This article deals with ‘Merger and Consolidation of Public Sector Banks.’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Bank Mergers

In 2016, it was decided in Gyan Sangam II that since Public Sector Banks aren’t performing well, there is a need to consolidate banks by merging small banks with the State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank etc. as Anchor Banks.

The crux of the matter is the government is working on a consolidation of public sector banks to create 3-4 global-sized banks and reduce the number of state-owned banks to about 10-12.

Mergers happened till now

2017: SBI’s 5 Associated Banks & Bhartiya Mahila Bank merged with SBI.

2019: Vijaya & Dena Bank merged with Bank of Baroda.

2019: Oriental Bank of Commerce and United Bank of India merged into Punjab National Bank.

2019: Syndicate Bank merged with Canara Bank.

2019: Andhra Bank and Corporation Bank merged with Union Bank of India.

2019: Allahabad Bank merged with Indian Bank.

Points in favour of Merger of Banks

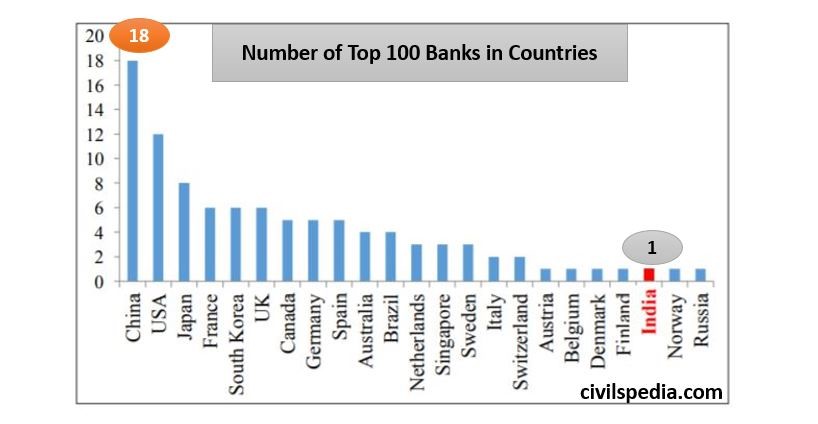

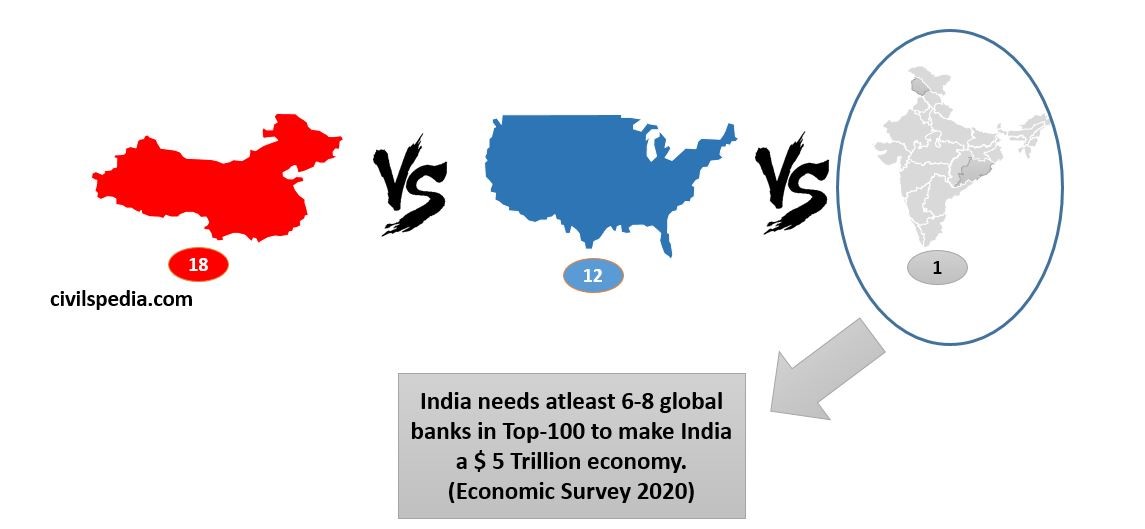

(Economic Survey 2020) It will help in placing more Indian Banks in the top 100 banks of the world. It is sine quo non to have at least 6-8 top-100 banks of the world in India if we want to make India a financial hub of Asia and channelize global savings towards India to make India a $ 5 trillion economy. Currently, India has just one bank in the top 100 banks (SBI = 55 Rank), while China has 18.

Earlier State Bank of Saurashtra (2008) & Indore (2010) merger into SBI was successful. Hence, previous experience is pleasant.

Larger banks provide financial stability and act as engines of growth in times of trouble. E.g. Chinese Banks in 2008.

It will lead to branch rationalization and reduce operating costs.

Larger Public Sector Banks can support the corporate sector better in overseas acquisitions as done by Chinese Banks.

To comply with BASEL III Norms, if big banks like Consolidated SBI issue shares, they can fetch a good response.

Enhanced geographical reach: For example, Vijaya Bank has strength in the South, while Bank of Baroda and Dena Bank had a stronger base in Western India. That would mean wider access for the proposed new entity and its customers.

Points against Merger of Banks

Mergers eat up a lot of top management time. At a time when Public Sector Banks need razor focus to deal with the NPA menace, mergers will be very distracting.

Large banks aren’t necessarily efficient banks: The quest to create an Indian banking giant is an old one when the world looked in awe at the Japanese banking giants. But their big size emboldened them to do excessive lending and ultimately they had to be bailed out by taxpayers’ money.

The merged State Bank of India is likely to be five times larger than its nearest competitor and can stifle the competition.

Setback to corporate governance: The merger sends out a poor signal of a dominant shareholder (the government) dictating decisions that impact the minority shareholders.

Banks will lose their regional identities.

Political Implications: Kerala Legislative Assembly has passed a resolution that the State Bank of Travancore’s merger with SBI will affect the state’s economic growth negatively.

Protests: Addressing the concerns of unions and shareholders will be challenging.

Harmonization of Technology: It is a big challenge as various banks are currently operating on different technology platforms.

Best way to Merge: Merge complementary banks. E.g., Bank of Baroda with Dena and Vijaya Bank so that layoffs aren’t large.

This article deals with the ‘History of Banking System.’ This is part of our series on ‘Economics’, which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

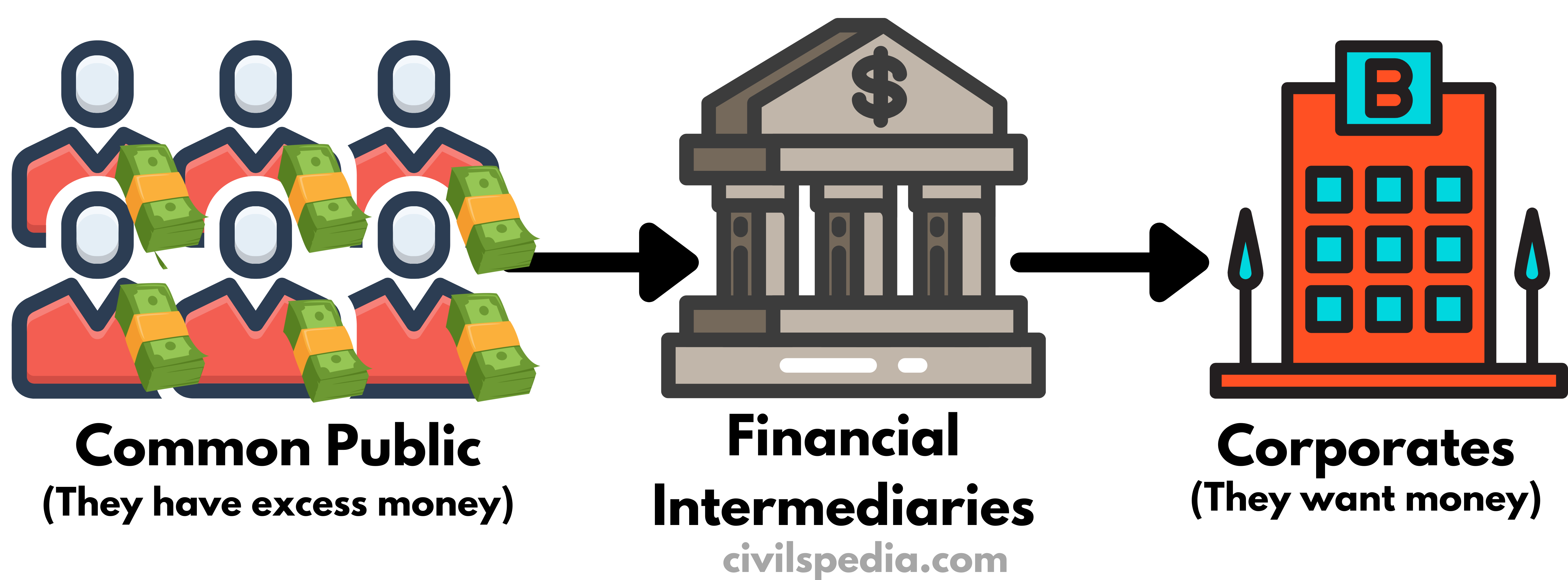

Financial Intermediaries

For the economy to function

properly, savings must be channelled into investments. But there is a conflict

here between savers and businesses/corporates.

Savers: Want instant access to their savings in case of unexpected expenditure.

Businesses/Corporates: Want promise that they will not be forced to repay loans prematurely.

Banks

can solve this problem by acting as an intermediary between savers and

businesses (Ben Bernanke et al. )

These include banks, insurance companies, pension funds, mutual funds etc.

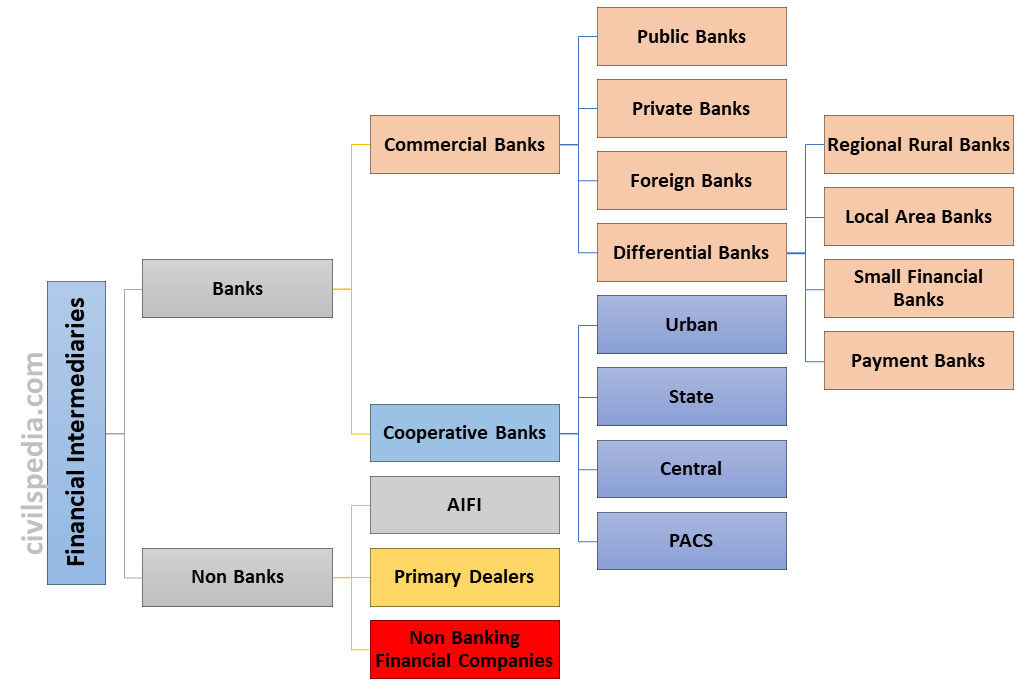

Banking System

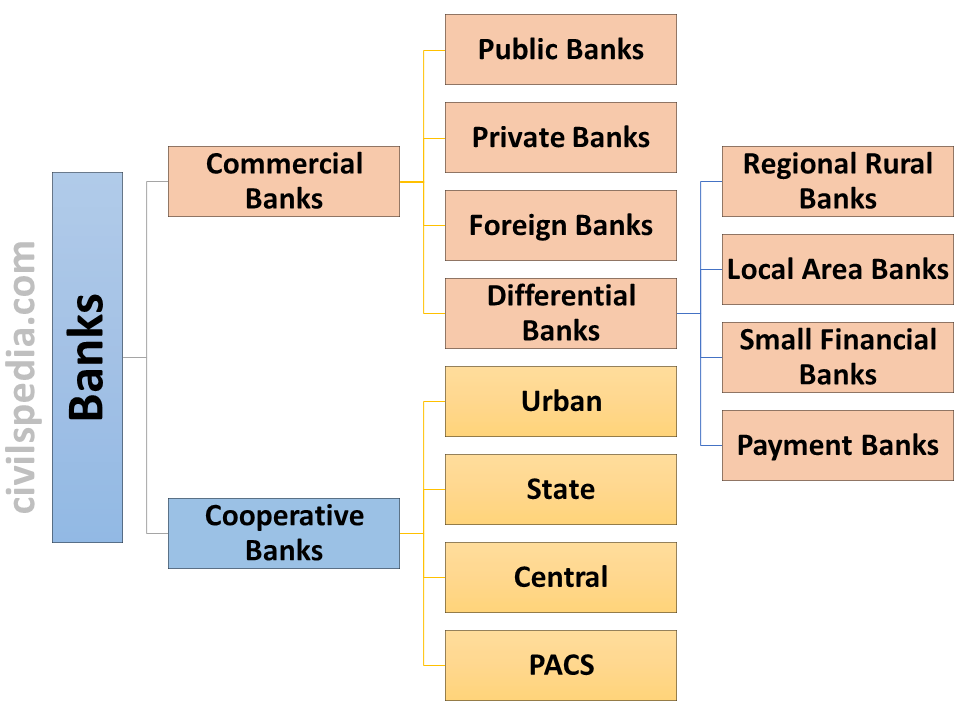

Type of Banks in India

Scheduled Commercial Banks

When RBI is satisfied that a bank has (Paid Up Capital + Reserves) of at least 5 Lakhs & it is not conducting business in a manner harmful to its depositors, such bank is listed in the 2nd Schedule of RBI Act, and it is known as a Scheduled Bank.

It is different from the Non-Scheduled Banks in the following way

Scheduled Banks

Non-Scheduled Banks

– Scheduled Banks are bound to maintain Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) as mandated by the RBI.

They are not required to maintain SLR and CRR.

– They are eligible to borrow funds via Liquidity Adjustment Facility (Repo and Bank Rates).

It depends on RBI’s discretion to borrow via this mechanism.

It can be subdivided into various parts 1. Scheduled Commercial Banks, e.g. SBI, Axis, PNB, ICICI Bank etc. 2. Schedule Cooperative Banks like Haryana Rajya Sahakari Bank etc. 3. Schedule Payment Banks like PayTM Payment Bank, Fino Payments Bank etc.

Hundreds of cooperative banks are non-Schedule Banks.

Topic: History of the Banking System in India

History of the Banking System in India before Independence

The present Banking System was introduced in the western world and was later introduced in India during the British Raj.

During British times, there were two types of Banks

1. British Banks

East India Company established Banks in 3 Presidencies.

Bengal

1806

Bombay

1840

Madras

1843

In 1921, these three merged to form the Imperial Bank of India. Later, it was nationalized and became SBI.

It provided services to British Army officers, Civil Servants & Judges.

2. Swadeshi Banks

These were set up by the Indians parallel to the British Banks.

First Indian Bank to be opened was Allahabad Bank(1856). Later, other banks such as Bank of Baroda (backed by Gaekwads of Baroda), Punjab National Bank (the role was played by Lala Lajpat Rai in its formation), Punjab & Sind Bank (by Bhai Vir Singh).

These banks targeted big merchants, particularly raw-material exporters.

But neither helped in financial inclusion.

Birth of RBI

By the early 1930s, many banks were operating in India. They were registered under the Company Law, and regulations on this sector were not present. But the problem arose during The Great Depression (1929), which started in the USA. Due to this, the demand for Indian exports in the foreign market decreased, and Indian merchants began to default.

Consequently, a large number of Indian banks collapsed.

To deal with such a situation and bring the banking sector under regulation, the British Indian government set up the Reserve Bank of India in 1934 under the recommendations of the Hilton Young Royal Commission.

History after Independence

The Government of

India took two important steps

Nationalisation of RBI

Banking Regulation Act,1949: It empowered RBI to control & regulate the Banking sector in India.

Nationalisation of Banks

Nationalisation of Banks: SBI Case (1st Round )

1955

Imperial Bank was nationalized & renamed SBI. (At the same time, the Nationalization of Insurance Companies was also done)

1960

8 Banks were nationalised & made subsidiaries of the State Bank of India.

1963

Two subsidiary Banks were merged (State Bank of Bikaner & State Bank of Jaipur), leading to the formation of the State Bank of Bikaner & Jaipur.

2008

State Bank of Saurashtra merged with Parent Bank.

2010

State Bank of Indore merged with Parent Bank.

Till recent times

There were 5 subsidiaries of SBI 1. State Bank of Bikaner & Jaipur 2. State Bank of Hyderabad 3. State Bank of Mysore 4. State Bank of Patiala 5. State Bank of Travancore

2017

All subsidiaries merged into Parent Bank

Nationalisation of Banks: Except SBI (2nd Round)

1969: 14 Banks having deposits of more than ₹ 50 Crore were nationalized.

1980: 6 more banks Nationalized, having deposits of more than ₹200 Crore.

Nationalised in 1969

Punjab National Bank, Canara Bank etc.

Nationalised in 1980

Punjab & Sind Bank, Vijaya Bank, Oriental Bank of Commerce etc.

Reasons of Nationalisation

To remove control & concentration of economic power in the hands of a few industrialists.

Due to misuse of funds by owners.

Due to the tendency of banks to ignore the needs of small-scale industrial sector & agriculture.

To remove the concentration of the banking sector mostly in Urban areas.

Objectives after Nationalisation

To open more banks in rural & semi-urban areas & to collect savings from these areas.

To provide credit facilities to areas defined as Priority Sector in the economy.

Has the nationalization of private banks benefitted India?

According to Economic Survey (2020), banking resources to rural areas, agriculture, and priority sectors have increased due to the nationalization of banks. For example, in the period between 1969-90

The number of rural bank branches increased ten-fold.

Credit to rural areas increased twenty-fold.

Agriculture credit expanded forty-fold.

The US Banking System shows the inefficiencies of the Private Banking System during the successive financial scams, including the Subprime crisis of 2008, lending to subprime borrowers, bias against people of colour etc. These things have not happened in India as the banks were nationalized in India.

But at the same time, Economic Survey (2020) doubts whether these benefits were entirely caused by nationalization as the period also saw various other events like green revolution, anti-poverty programmes (like the Integrated Rural Development Programme) and policies of RBI (such as RBI’s 4:1 formula).

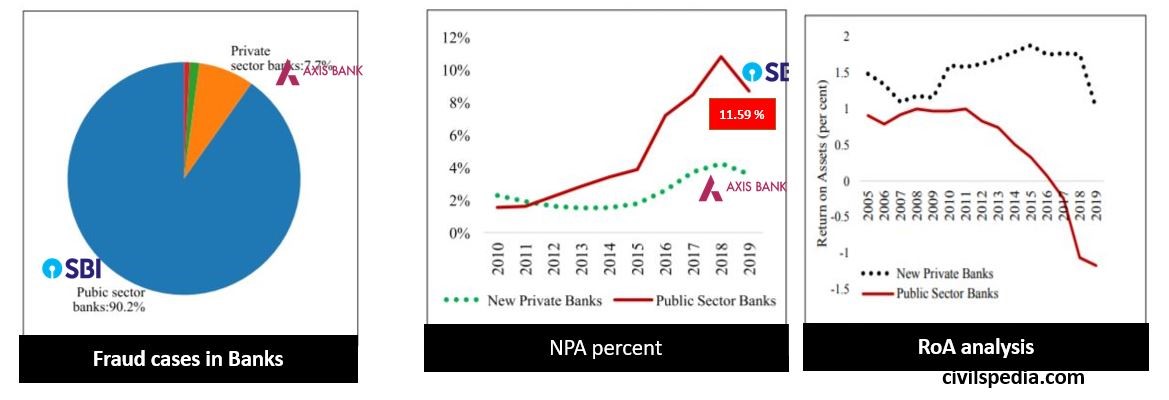

Issues faced by Public Sector Banks due to Bank Nationalisation

Since the government was the majority shareholder of the banks, it started to give loans at populistic ‘Government Administered Interest Rates’, which decreased the banks’ profitability.

Banks were forced to give loans to fund unviable projects based on political considerations, which increased the NPAs of Public Banks as the recovery of such loans was low.

Public Sector Banks account for 92.9% of bank fraud cases. A large majority (90%) were related to advances, suggesting the poor quality of screening and monitoring processes for corporate lending adopted by Public Sector Banks.

PSBs perform poorly on Return-on-Assets (RoA), Return-on-Equity (RoE) etc., when compared with Private Banks. Public Sector Banks are having negative RoA presently.

The politicization of Bank Boards happened with the government placing its favorites in the Board of Directors irrespective of their knowledge and talent. It reduced the professionalism in the banks.

Due to the above reasons, RBI feared that banks could collapse. Hence, it mandated a high Cash Reserve Ratio (CRR), reducing the funds at the disposal of banks for loan purposes.

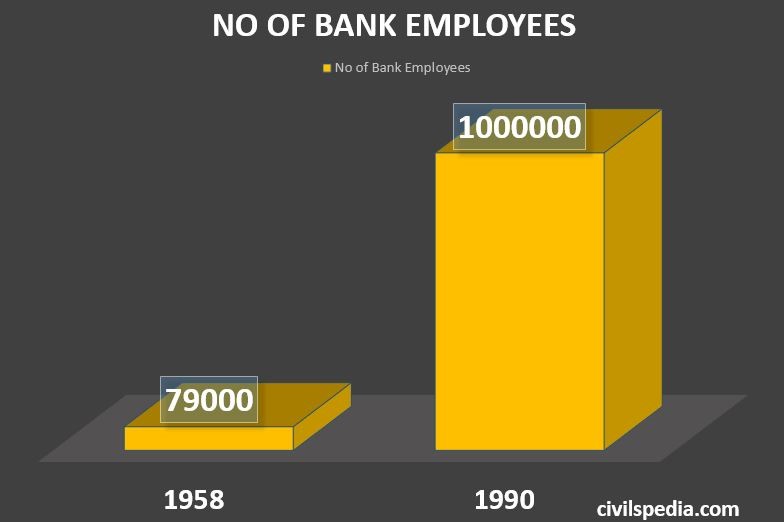

A large staff was hired in banks, even more than required, to create government jobs. It led to the unionization of staff and inefficient customer services. Frequent hartals of bank employees were observed in the period after nationalization.

PSB officers are subjected to extra scrutiny by the Central Vigilance Commission and CAG. Officers are wary of taking risks in lending or in renegotiating bad debt due to fears of harassment under the veil of vigilance investigations.

Side Topic: Number of Public Sector Banks Today

Public Sector Banks = 13 ( on January 2022, including India Post Payment Bank)

Old Private Banks

All the Big Private Banks were nationalized. But there were Small Private Banks whose deposits were less than limits and weren’t nationalized. These Banks are now called Old Private Banks.

There are 12 such banks in India.

These are Scheduled Banks and have to maintain Cash Reserve Ratio & Statutory Liquidity Ratio.

Examples: Catholic Syrian Bank, Dhanlaxmi Bank, Federal Bank, Jammu and Kashmir Bank etc.

Narsimham Committee and (Rise of ) New Private Sector Banks

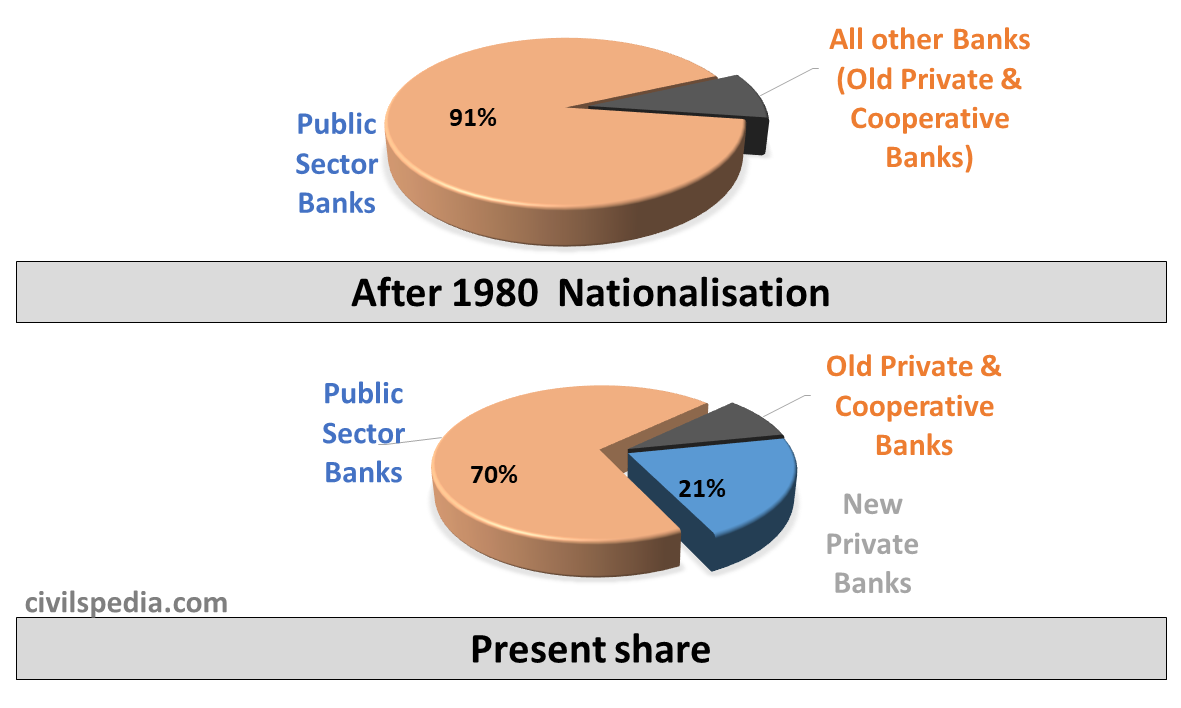

After the

1980 nationalization, Public Sector Banks had a 91% share in the national

banking market which has reduced to 70%. The reduced stake has been absorbed by

New Private Banks (NPBs), which came up in the early 1990s after

liberalization. It brings us to the topic of New Private Banks.

Private Sector Banks

The Balance of Payment crisis of 1991 finally forced the government

to set up a Committee for Banking Sector

Reforms under the former RBI

Governor M Narsimham. He recommended following

Government should decrease its shareholding in Public Sector Banks.

The banks’ resources came from the general public and were held by the banks in trust that they were to be deployed for the maximum benefit of the depositors. Even the government had no business to endanger the solvency, health and efficiency of the nationalized banks under the pretext of using banks, resources for economic planning, social banking, poverty alleviation, etc.

RBI should decrease Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR).

Priority Sector Lending (PSL) given to agriculture and Small Scale Industries (SSIs) should be phased out gradually as they had already grown to a mature stage.

Government should not dictate interest rates to Banks.

Liberalize the branch expansion policy.

Allow entry of New Private Banks and New Foreign Banks.

This led to 3 Rounds of Banking Licences.

1st Round (1993-95)

10 licenses were given to open the following banks. 1. ICICI 2. HDFC 3. Indus 4. DCB 5. UTI (later became Axis bank) 6. IDBI (presently owned by LIC) 7. Global Trust Bank (later merged with Oriental Bank) 8-9-10: Bank of Punjab, Centurion Bank, and Times Bank were merged into HDFC

2nd Round (2001-04)

2 licenses were given in the 2nd Round 1. Kotak Mahindra 2. Yes Bank

3rd Round (2013)

Bimal Jalan Committee made selections 1. Bandhan Bank (Originally, a Microfinance company based in West Bengal) 2. IDFC (Originally, an infra finance NBFC based in Maharashtra).

Side Topic: Number of Private Banks in India

22 presently (after IDBI is privatised).

On Tap System of Banking License

Earlier System: Start & Stop System

RBI issues notification and interested entities can apply at that time only..

Till now, 3 such rounds have happened

The new system proposed in 2016: On Tap System

In this system, there will be no deadline for application. Hence, there is no need to wait for notification.

When an entity thinks it is fit to become a bank, it can approach RBI with the application.

RBI has issued guidelines regarding this too.

In 2021, RBI gave Small Banking License to Unity Small Finance Bank through this route.

The following company can apply for Bank License via the ‘On-Tap’ System

The company must have a minimum of 500 crores paid-up capital.

The company must have 10 years of record in the banking/finance sector.

Initially, it must be controlled by Indians (100% shareholding should be with Indians).

Applicant must be willing to open a minimum of 25% branched in rural areas.

They have to maintain CRR, SLR, PSL etc.

But large industrial houses and NBFCs can’t open banks via this route.

Foreign Commercial Banks

In the Nehruvian Socialist Economy, there was disdain & apprehensions about Foreign Banks. Only a handful of them was allowed to open branches. But, Post-Narasimham-Reform, foreign banks approval policy was liberalized.

In 1991, M Narsimham Committee recommended allowing Foreign Banks on a reciprocal basis. The government accepted this proposal.

There are 44 Foreign Banks in India

AB Bank

Abu Dhabi Commercial Bank

American Express banking

ANZ Banking Group

Bank of America

Bank of Bahrain and Kuwait

Barclays Bank

BNP Paribas

Citibank

Commonwealth Bank of Australia

CCRB

Credit Agricole

Credit Suisse

DBS Bank

Deutsche Bank

Doha Bank

FirstRand Bank

Industrial and Commercial Bank of China

Industrial Bank of Korea

JP Morgan Chase Bank

JSC VTB Bank

KBC Bank

KEB Hana Bank

Krung Thai Bank

Mashreq Bank

Mizuho Bank

National Bank of Australia

National Bank of Abu Dhabi

PT Bank

Maybank Indonesia

Sberbank

SBM Bank

Shinhan Bank

Societe Generale

Sonali Bank

Standard Chartered Bank

Sumitomo Mitsui Banking Corporation

Bank of Nova Scotia

Bank of Tokyo

The Hongkong and Shanghai Bank

Royal Bank of Scotland

United Overseas Bank

Westpac Bank

Woori Bank

First, foreign banks have to open an Indian Subsidiary registered in India under the Companies Act.

Core Banking Solution

Core Banking Solution (CBS) is the networking of branches, enabling customers to operate their accounts and avail banking services from any branch of theBank on the CBS network, regardless of where he maintains his account. The customer is no more the customer of a Branch. He becomes the Bank’s Customer.

It has helped in converting Branch Banking to Branchless Banking.

Entry of Business Houses in the Banking Sector

Procedure to open a new bank

Register the company with the Ministry of Corporate Affairs.

The company has to issue IPO in the share market after taking SEBI’s permission to arrange the capital.

Then, the company has to take permission from RBI through the ‘On Tap’ System.

After doing this, the company will initially get a Non-Scheduled Bank License. After some years, when RBI is confident that the bank has good health, RBI will upgrade the license of the Bank to Scheduled Commercial Bank.

Analysis: Should private houses be allowed to open banks

Arguments in favour

More competition will lead to better services, higher interest rates and better customer services.

Existing banks have stressed balance sheets due to high NPAs. Hence, they have become over cautious while giving new loans. The entry of fresh banks will re-invigorate the lending process.

It will help the ‘shadow banks’ such as IL&FS and DHFL to become banks and come under the proper supervision of RBI.

Based on the above arguments, PK Mohanty Committee, to review the corporate structure for Indian Private Sector Banks (2020), recommended allowing private houses’ entry into the banking sector.

Arguments against

Connected Lending: In Connected lending, promoters of the bank lends loan at favourable terms to the companies owned by that group. The issue of connected lending was rampant in India from 1947 to 1958, which led to the failure of 361 banks in India during that phase.

Circular Banking: It has the potential to lead to circular banking under which a bank controlled by Corporation A lends a loan at favourable terms to Corporation B and a bank controlled by Corporation B lends a loan at favourable terms to Corporation A. In the process, the interests of the depositors are jeopardized.

The higher competition will lead to excessive loan disbursement and misspelling of the banking products to gain new customers and retain the old customers. These types of practices led to Subprime Crisis in 2007-08. After the subprime crisis, most countries have become cautious to such ideas.

History: Corporate houses were active in the banking sector till five decades ago, when the banks promoted by them were nationalized in the late sixties amid allegations of connected lending and misuse of depositors’ money.

RBI cannot effectively regulate the existing banks as shown by various scams like Yes Bank-Rana Kapoor Scam, ICICI-Vodafone Loan Scam, Punjab National Bank-Nirav Modi Scam etc. Hence, it is not guaranteed that RBI will be able to regulate the new banks effectively.

Large industrial houses face severe corporate governance issues, as epitomized by Ratan Tata- Cyrus Mistry and Narayan Murthy-Vishal Sikka controversy. In such a situation, allowing them to open banks is not advisable.

Banks controlled by big business houses can be misused for nefarious activities such as money laundering.

It can create very powerful oligarchs with large economic power.

Even regulators in developed countries don’t encourage the entry of business houses in the banking sector.

Considering the above discussion, the risks outweighs the

benefits. Government can take steps to strengthen the corporate structure and

health of the present banking sector.

This marks the end of the article on “History of Banking System.’

Last Updated: May 2023 (Convertibility of Current Account & Capital Account)

Convertibility of Current Account & Capital Account

This article deals with ‘Convertibility of Current Account & Capital Account .’ This is part of our series on ‘Economics’, which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Why restrictions on Convertibility?

Central Bank can’t manage a floating exchange rate regime all the time. Otherwise, Forex reserve will get empty. Hence, quantitative restrictions are placed on the conversion of ₹ to foreign currency.

There can be two types of restrictions, i.e. on the Current Account & Capital Account.

Current Account Convertibility

Current account convertibility means the freedom to convert currency for current transactions in terms of outflows and inflows.

In the case of India, Current Account is fully convertible (since 1994) & there are no quantitative restrictions. It means ₹ is fully convertible into another currency for current account transactions & vice versa is also true.

Capital Account Convertibility

Full capital account convertibility means :

A foreign investor can convert any amount of foreign currency to Indian Rupees and invest in any asset in India without any restriction. This investor can also sell the investment without any restriction, convert the resulting Indian Rupee amount to a foreign currency and take it out of the country.

A Domestic Investor can convert Indian Rupee to foreign currency and invest in any asset abroad without any restriction.

A Domestic Investor can raise any amount from External Market and convert it into Indian Rupees to invest that amount in India.

₹ is not fully convertible on the capital account. But after the S.S. Tarapore Committee (1997) recommendations on Capital Account Convertibility, India has been moving toward allowing full Capital Account Convertibility.

There are the following limitations on Capital Account Convertibility

Indian corporates are allowed full Convertibility of up to $ 500 million annually for oversea ventures.

Individuals are allowed to invest in foreign assets, shares, etc., up to $ 2,50,000 per annum.

Liberalised Remittance Scheme (LRS)

LRS was started by Government in 2004.

Under the scheme, an Indian resident (including a minor) is allowed to take out up to $2,50,000 from India either for a current Account or capital account transaction. (e.g. paying for college fees abroad, buying shares, bonds, properties, and bank accounts abroad.)

Issue: Panama papers allege various Bollywood celebrities used the LRS window to shift money from India to tax havens for tax avoidance.

Debate : Should there be Full Capital Account Convertibility?

There is an ongoing debate that there should be full capital account convertibility.

Arguments in favour of full Capital Account Convertibility

If the capital account is fully convertible, India can attract more FDI, FPI and ECB to India, creating new jobs & pushing economic growth.

It will increase the choices for investments– Investors get the opportunity to base their investment and consumption decisions on world interest rates and world prices for tradeable.

Various committees like SS Tarapore Committee have also accepted this.

Arguments against Capital Account Convertibility

IMF study says there is no correlation between full Capital Account convertibility & business growth.

It could lead to the export of domestic savings.

Companies that would get money in $ via ECB would be returned in $s only. But this is not favourable in times of Exchange rate volatility.

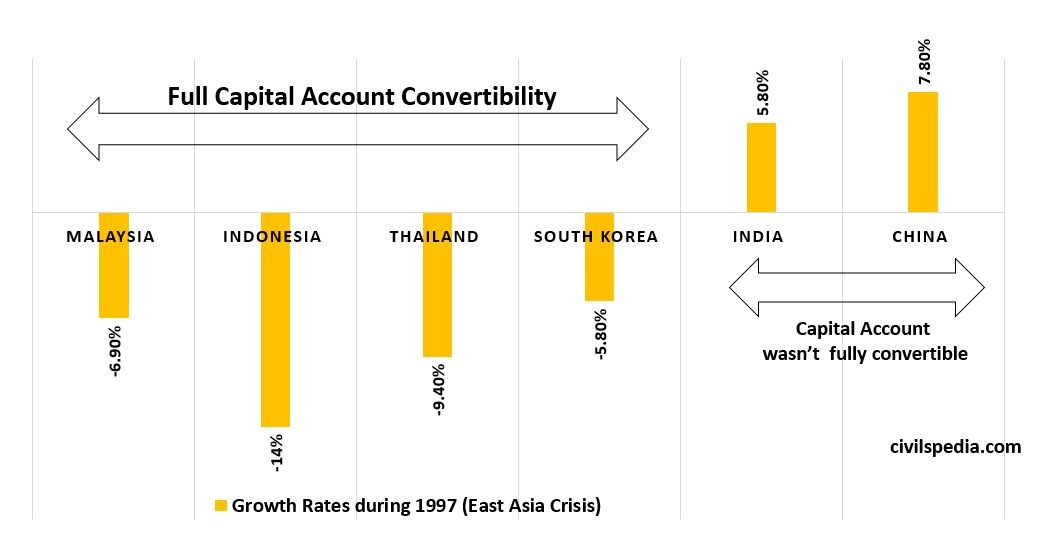

If our currency falls, the whole system can collapse, as happened in the East Asian Crisis of 1997. India & China survived the crisis because both didn’t have full capital account convertibility.

Various committees, like HR Khan Committee, have rejected full Capital Account Convertibility.

Side Topic: East Asian Financial Crisis

Before 1997, All East Asian Economies deliberately kept their currencies undervalued to boost export. (like China is doing now)

All these countries had full capital account convertibility. Foreign investment was quite high, and GDP growth was in double digits.

Thailand’s steel & automaker companies filed for bankruptcy. Foreign investors panicked and started to pull out $s from similar companies from all South East Asian Nations. As a result, their currencies & economies collapsed. E.g.: Indonesian Rupiah collapsed from 1$ = 2,000 to 1$ = 18,000 Indonesian Rupiah.

It led to high inflation culminating in rioting & political instability.

On the other hand, India and China survived this tumultuous period because their capital account wasn’t fully convertible. Hence, investors couldn’t pull off their investments overnight due to restrictions under Capital Account convertibility.

SS Tarapore Committee (1997)

The recommendations of the committee were as follows

He was in favour of Full Capital Account convertibility, but he also feared that a crisis like East Asian Crisis could happen in India too. For this, he advised that there should be some conditions before doing that

Conditions

Conditions

India’s situation

Forex

to sustain 6 months of imports

Yes, India has a forex of more than $550 billion (i.e. Can sustain

11 months of imports)

Fiscal

Deficit of 3.5% of GDP

Target for 2020 is 3.5% (but

will be breached due to Corona pandemic induced slowdown)

Inflation

should be between 3-5% (for 3 years)

Under

the new Monetary Policy Framework, it should be contained between 2-6%

This article deals with ‘Forex Reserves of India .’ This is part of our series on ‘Economics’, which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Current Status of Forex Reserves of India

Forex is the external assets that are readily available and controlled by the monetary authority for direct financing of external payment imbalances, for indirectly regulating the magnitude of such imbalances through exchange market intervention to affect the currency exchange rate and other purposes.

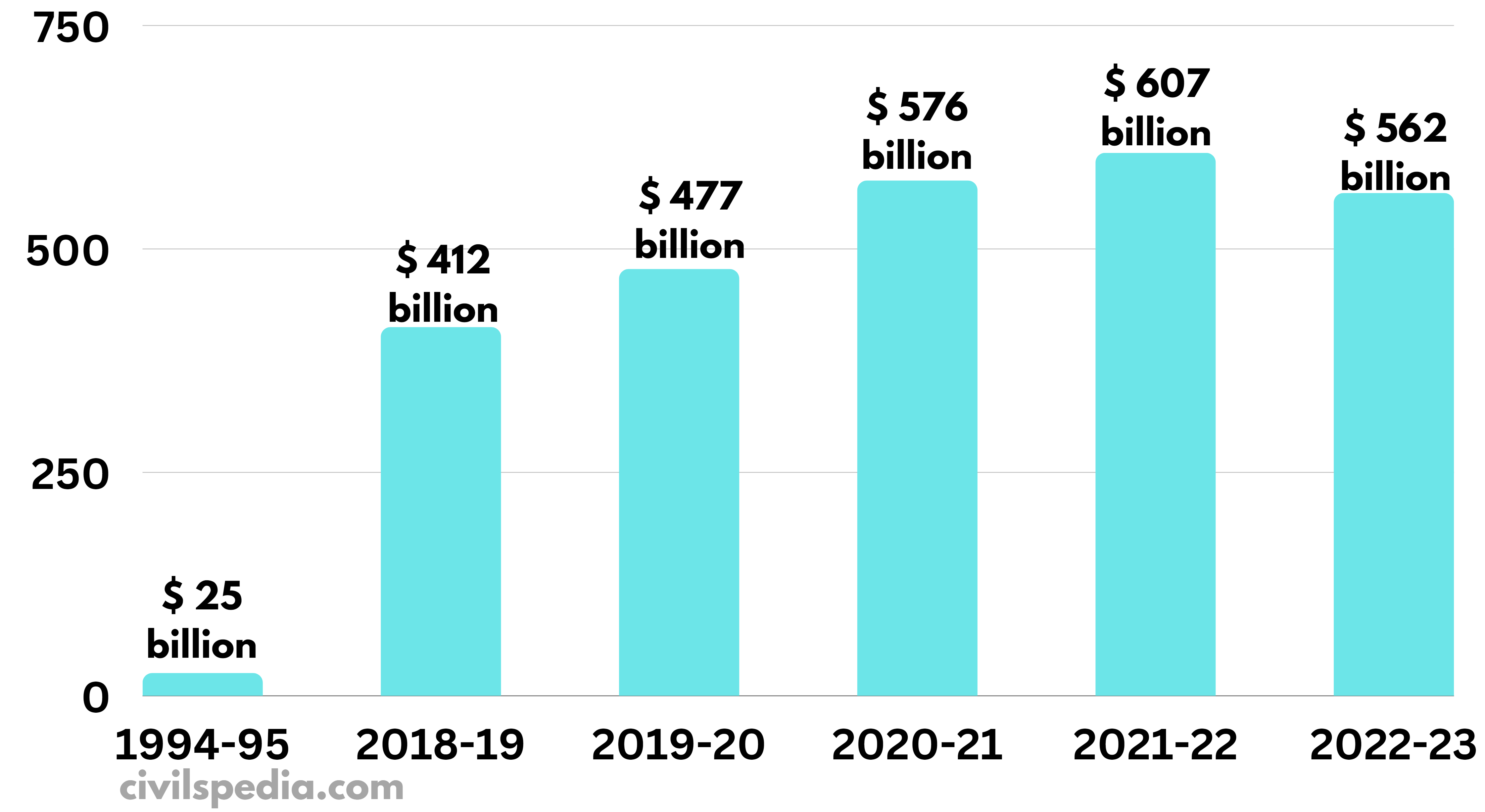

India’s forex reserves are about $562 billion (Dec 2022).

It is enough to finance about 9 months of imports. It has reduced from 13 months of imports in 2021. In March 1991, it was reduced to just 2.5 months of import coverage (which forced the country to seek International Monetary Fund assistance).

Ranking of Foreign Reserves with RBI

Foreign Currency and Foreign Currency Assets

Gold

IMF’s SDR

Reverse Tranche Position in the IMF

World Ranking of Forex Reserves ( India 6th and China topped with 3.2 Trillion Forex)

Rank

Country

Forex

1

China

$ 3.2

trillion

2

Japan

$1.2

trillion

3

Switzerland

$812

billion

—-

———

————-

6

India

$562.72 billion (Dec 2022)

(Covering

9.3 months of imports)

Forex Reserves of India are under pressure and decreased in recent times. The reason include

Adverse global economic conditions and the fear of global recession led to a decrease in Indian exports.

Sharp rise in the price of oil in the international market

Fed Tapering led to an outflow of forex currency from India.

Reason for maintaining High Forex Reserves

It reduces the risk of external vulnerabilities such as high oil prices or Fed Tapering.

Exchange Rate Management: High Forex allows occasional RBI intervention to curb excessive volatility in the foreign exchange market.

It increases the investor’s confidence in the economy of the country.

It will help India to become a regional leader by signing currency swap agreements with other neighbours such as Sri Lanka, Bangladesh etc.

Issues with maintaining more than required Forex

While reserves are imperative in both preventing crisis situations

and mitigating their impact, there are issues with maintaining more than

required Forex Reserves. The problems with maintaining more than required Forex

reserves include

Lost Opportunity Cost: Holding more than the required Forex Exchange reserve has opportunity cost because the stored money could be used for improving infrastructure and social services (like health and education)

Increase borrowing cost: Borrowing in foreign currency has high borrowing cost and is vulnerable to volatility in the exchange rate

Is India’s Forex Reserves enough?

As evident from the graph above, India’s Forex reserves have reduced. But it should not be a cause of worry as India has enough Forex Reserves based on the following yardsticks.

#1 IMF’s Guidotti–Greenspan Rule

According to Guidotti-Greenspan Rule, the country should have enough Forex Reserves to cover the short-term external debt.

Indian Forex Reserves comfortably meets this rule.

#2 RBI’s Tarapore Committee

According to Tarapore Committee, the country should have enough Forex Reserves to pay for 6 months’ imports.

Indian Forex Reserves comfortably meets this rule as well (Indian Forex Reserves can pay for more than 9 months’ imports).

Side Topic: How did China reach the top foreign exchange reserve position?

The term used for this phenomenon is ‘China’s Mercantile Policy’. Under this policy, China refrains from imports from other countries, and at the same time, exports are encouraged.

China restrains from imports in the following ways

IT

SOEs

(State Owned Enterprises) opaquely control the domestic market

Pharma

Inordinate delay in clearance

Food

SPS agreements used to ban imports

Manufacturing

Domestic products are too cheap

At the same time, Exports are promoted by

Keeping Yuan undervalued

SOE get cheap loans

Subsidies are provided on a large scale

Tech-piracy is neglected

Side Topic: Manipulators of Currency

US Treasury Department makes a list of countries which manipulate their currency.

3 Conditions to include any country in this list

A trade surplus of over $20 billion with the US.

The current account surplus is 3% of the GDP with the rest of the world.

Persistent foreign exchange purchases of 2% plus of the GDP over 12 months.

In 2018, India was included in this list. But India was removed in 2019.

This article deals with ‘Balance of Payment.’ This is part of our series on ‘Economics’ which is important pillar of GS-3 syllabus . For more articles , you can click here.

Introduction

Balance of

Payment is the summary/account sheet made by the country’s central bank

that shows the cash flow between residents of a country with the

rest of the world for a specified time period, typically a year.

A payment to a foreign country

is a debit transaction, whereas a payment received from a foreign

country is a credit transaction.

Outgoing

-ive

Incoming

+ive

The IMF decides the format, and all data is presented in dollars for the comparison’s sake.

If the Balance of Payment of all countries is added, the answer will be zero (because one nation’s credit becomes the other’s debit).

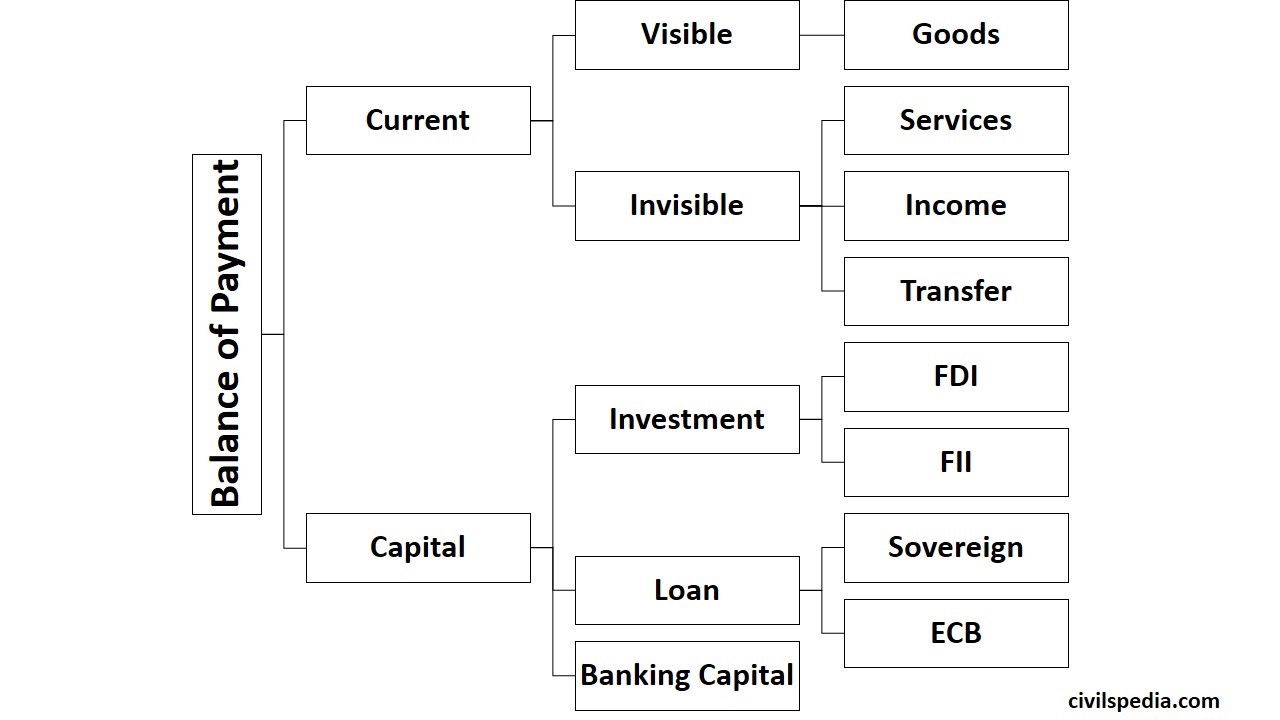

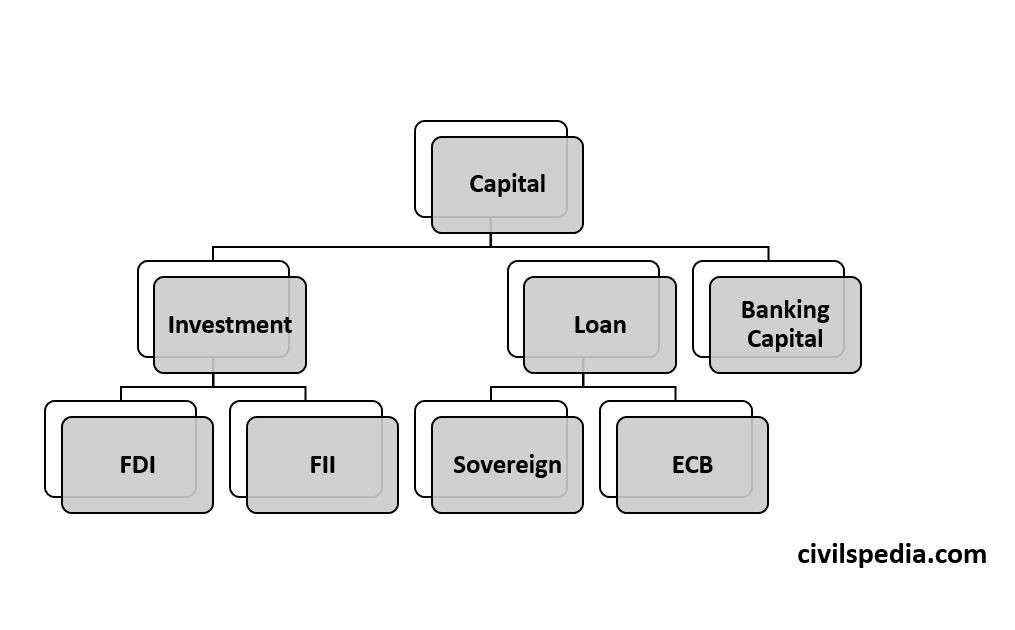

Components of Balance of Payment

Balance of

Payment comprises two parts: Current Account and Capital Account.

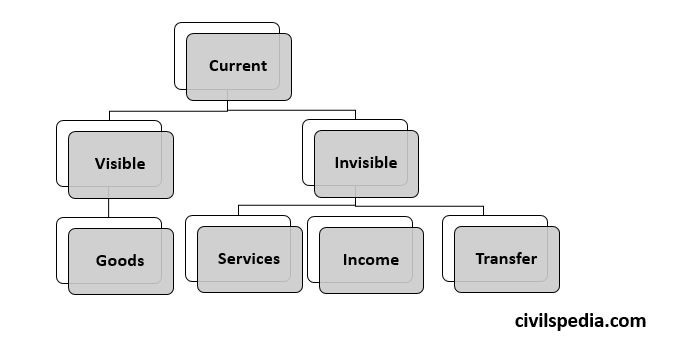

Current Account

The Current Account is the record of trade in goods and services, transfer of income (in the form of profit, interest and dividend) and transfer payments.

Capital Account

Capital Account records all international transactions of assets. An asset is any one of the forms in which wealth can be held, for example, money, stocks, bonds, Government debt, etc.

Part 1: Current Account

Note: In the Economic Survey, 2023 (which was published on 31/Jan/23), they have published only partial data from April to December-2022. Hence, instead of going into the exact data of each component, we will look into general trends. Even UPSC asks about general trends in the exam.

Visible Part and Balance of Trade (BoT)

The movement of goods (export and import) is also known as ‘visible trade’ because the movement of goods between countries can be verified physically by the customs authorities of a country.

Balance of Trade is the net difference between the export & import of goods.

India always has a trade deficit because Indian imports are always more than exports.

Imports & Exports of Goods

Major Exports

1. Petroleum Products (14% of all exports) 2. Gems and other precious metal Jewellery 3. Organic and Inorganic Chemicals 4. Drug and Biologicals 5. Iron and steel

Major Imports

1. Petroleum: Crude (22% of all imports) 2. Electronic goods 3. Coal and coke 4. Gold 5. Chemicals

But there is a danger of a slowdown in Indian exports due to the fear of a global recession.

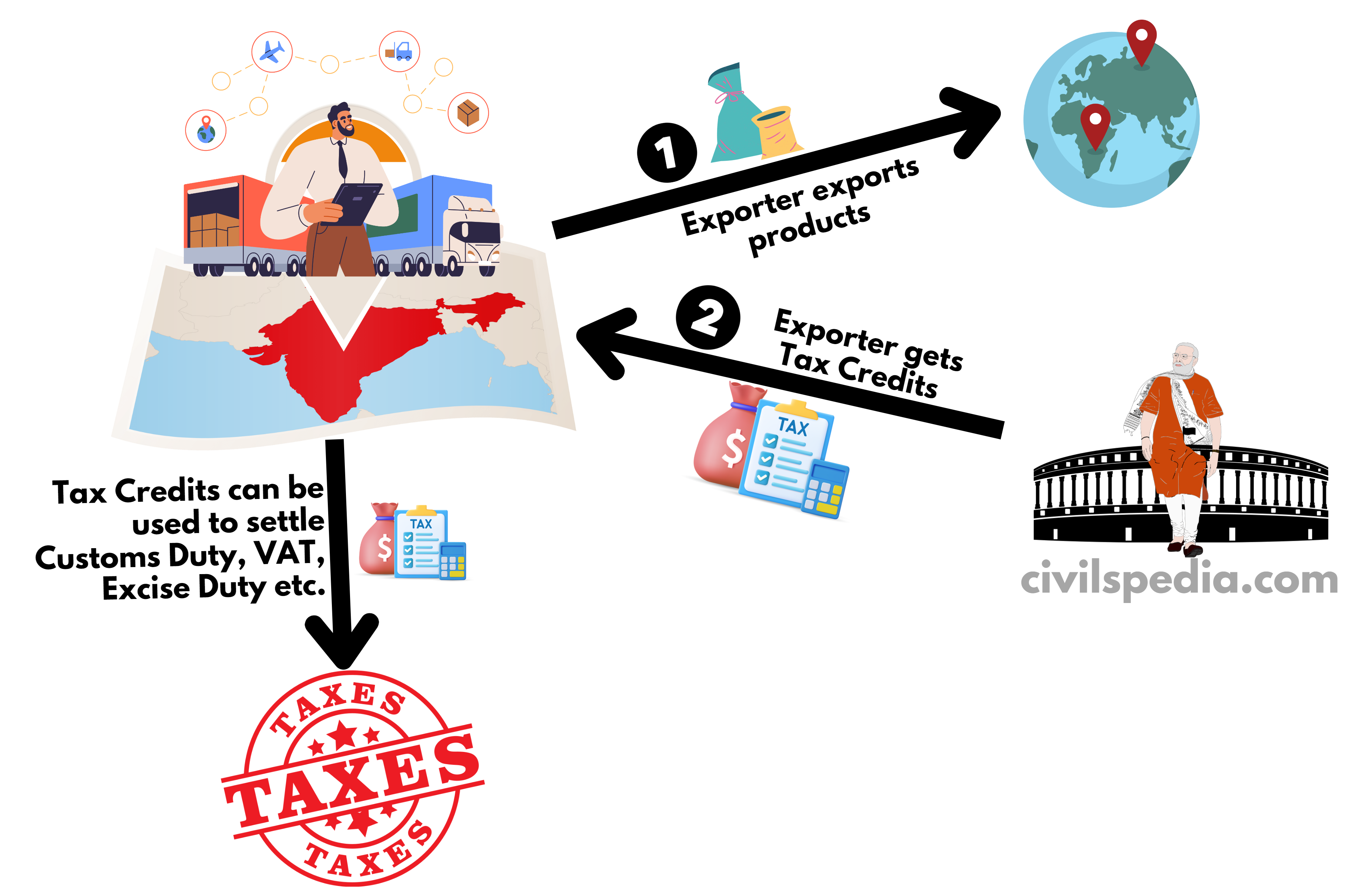

RoDTEP Scheme

Under RoDTEP, tax credit earned by the merchant can be used to settle (1) Customs Duty, (2) excise duty and VAT on the export of fuel, (3) electricity duty on the export of electricity and APMC Mandi fees on the export of agricultural raw material.

Remission of Duties & Taxes on Exported Products (RoDTEP) has replaced MEIS (Merchandise Exports from India Scheme) as MEIS was declared against WTO obligations and also due to the shortcoming that MEIS tax credits can be used to settle Customs Duty only.

Steps to Improve Export Competitiveness of India

Some suggestions from Economic Surveys of recent years are as follows

1. Change in mindset

Indian policymakers and businesses will have to change their mindset. They shouldn’t only produce what they can make with ease. Instead, they should focus on what the world needs from India.

2. Product Basket and Destination Diversification

India should focus on Product basket and destination diversification. It can be achieved by signing more FTAs to enhance trade opportunities.

3. Logistics

Government should focus on improving the logistics to make Indian exports more competitive.

4. Sign FTAs

India should sign Free Trade Agreements with as many nations as possible.

5. Currency Rate

India should make sure that the Indian Rupee is not overvalued.

Most of the time, it has been observed that REER is greater than 100. As a result of the overvaluation of the Indian Rupee, Indian exports are expensive compared to our competitors like Vietnam and Bangladesh.

6. Promote Make in India

India should make a solid industrial base and encourage export-oriented manufacturing (as China did in the past).

7. Combine Assemble in India with Make In India

‘Assemble in India for the world’ should be integrated with the ‘Make in India’. By doing so, India can raise its export market share to about 3.5 per cent by 2025 and 6 per cent by 2030.

8. Use GI Tags

India should export products like Darjeeling Tea, Basmati rice etc.

9. Other suggestions

India should reduce the import of petroleum by promoting ethanol blending of ethanol.

India needs to utilize SEZ potential properly due to numerous policy issues.

The Government has introduced Export Preparedness Index to evaluate State’s capacity and potential to export goods. It will guide the stakeholders to strengthen the export ecosystem accordingly in a particular area.

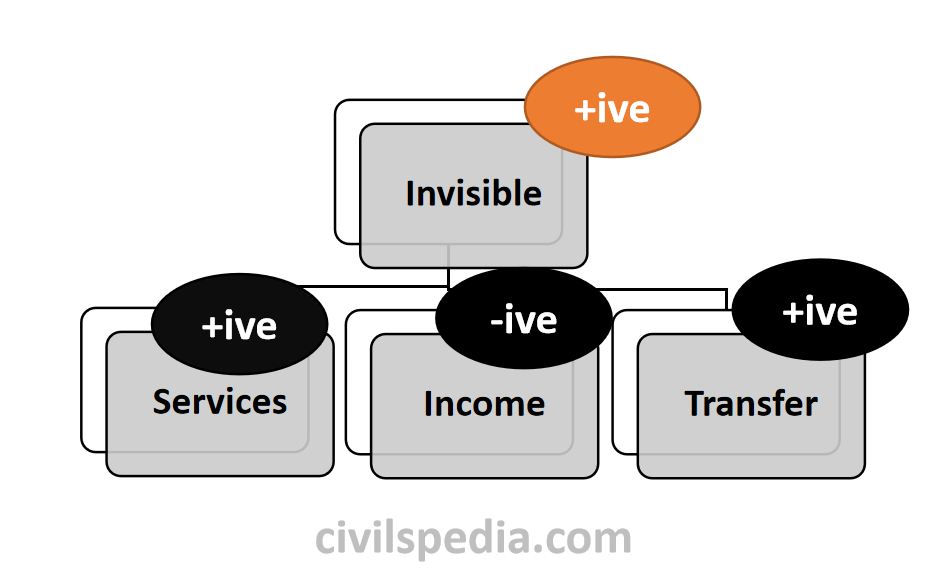

Invisible Part & Balance of Invisibles

Balance of Invisibles is the difference between the export & import of Invisibles, i.e. Services, Income and Transfers.

Generally, the Balance of Invisibles is positive for India.

1. Service

India has always been a surplus in Services due to the well-developed IT and BPO sectors.

Hence, the general trend is that India is a surplus in Services.

Note – The general trend is that Trade in Goods and Services (combined) is negative because Trade Deficit is much larger than the Surplus in Services.

Major exports and imports of India in services are

Exported Services

1. Software, IT and BPO services (40% of all service exports) 2. Transportation 3. Travel tourism 4. Financial

Imported

Services

1. Business Services (like digital advertisements) 2. Foreign Travel 3. Fees for using the intellectual property of foreign entities

Service Export from India Scheme (SEIS)

The government introduced this scheme to increase the export of Services from India.

Under this, for the export of Services worth every $100, Commerce Ministry transfers $ 5 to the Scrip Wallet of that firm, which can be used for paying tax liabilities.

2. Income

Income consists of profit earned by FDIs, interest on loans & dividends earned by investors.

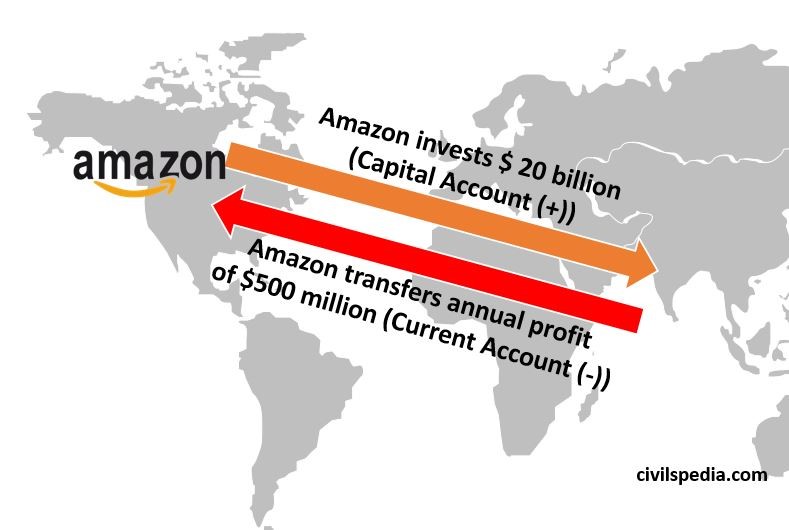

It has to be noted that whenever a foreign investor invests in any country, he will get back a dividend (in case of equity) or interest (in case of debt) or profit (in case a company like Amazon is doing FDI in India). These incomes are counted in the Current Account.

The general trend is that India is a deficit in Income.

3. Transfer

It includes three things.

Remittances (sent to India by Indians living abroad and by foreigners residing in India to their native countries (e.g. Nepal))

Gifts

Donations

According to World Bank’s Remittance Report, India receives the largest amount of remittance (about $100bn), followed by (2) Mexico, (3) China, (4) the Philippines and (5) Egypt.

The general trend is that India is a surplus in Transfers.

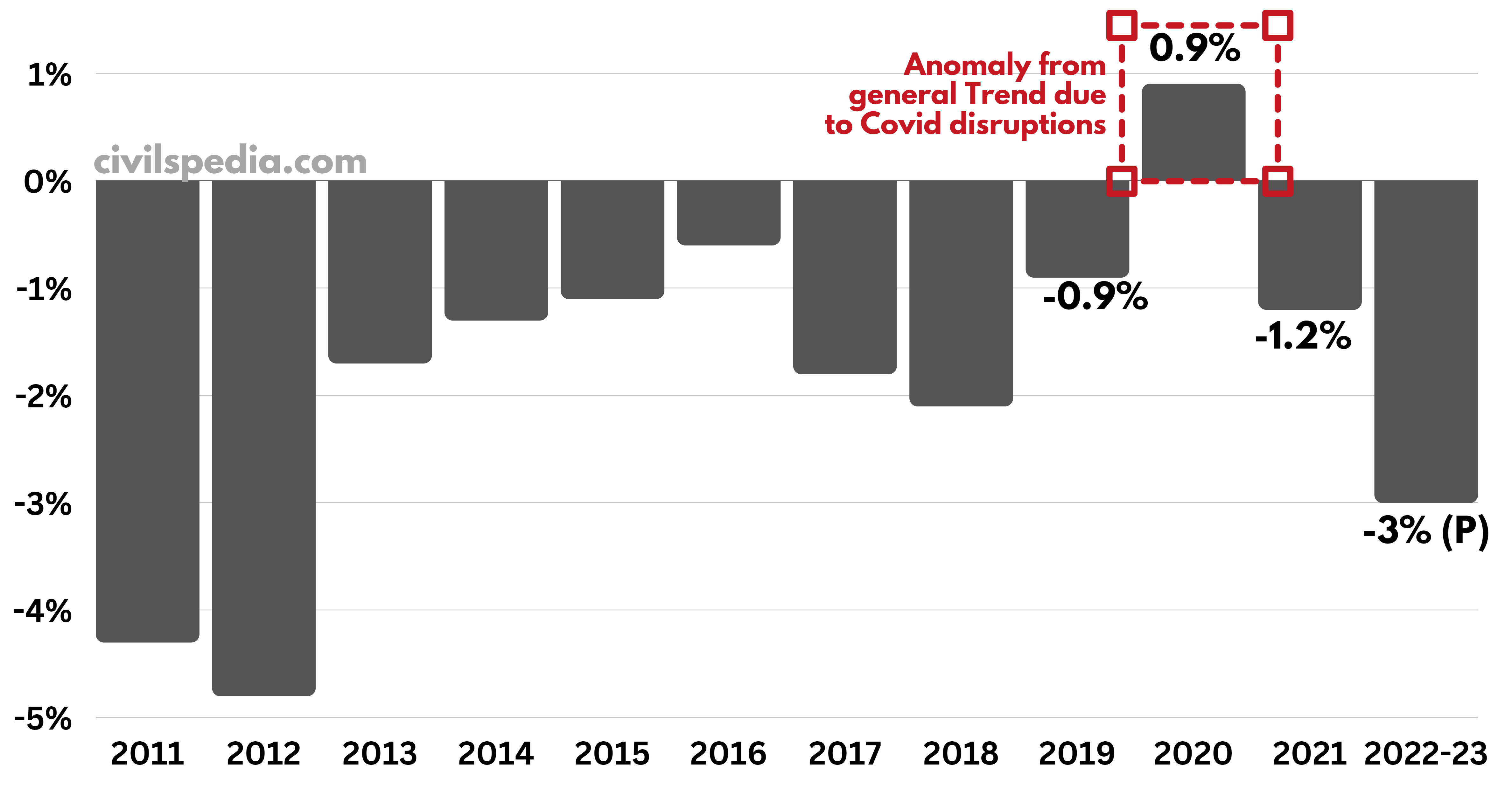

Current Account of India (Final Stats)

The Current Account is in balance when receipts on the Current Account are equal to the payments on the Current Account. A surplus Current Account means that the country is a net lender to other countries, and a deficit Current Account implies that the country is a net borrower from other countries.

India

generally has a DEFICIT CURRENT ACCOUNT.

Based on a historical perspective, India can sustain a CAD of 2.5-3.0% of GDP without getting into an external sector crisis.

Note:

From 2001 to 04, India had a Current Account Surplus because Indian exports to

Western economies were booming, especially in the wake of the BPO revolution in

India.

Current Account Deficit is not considered good

If CAD increases, the currency of the country weakens.

For a country like India, which has high imports, it increases the cost of imports impacting the economy negatively.

CAD for 2023-24 can be a challenge as

The prices of commodities that India imports (like petroleum, gold etc.) have reached record-high levels. Additionally, there is strong pent-up domestic demand for foreign goods in India.

Due to the slowdown in the advanced economies, the global demand for Indian goods is low.

The rupee has been weakening against the US dollar, further increasing the cost of imports.

Side Topic : Major Importers and Exporters of India

Importers of Indian Products

1. USA (16% of India’s exports are sent to the USA) 2. United Arab Emirates 3. Netherlands 4. China

Exporters to India

1. China (14% of all Indian imports are from China) 2. USA 3. United Arab Emirates 4. Saudi Arab 5. Iraq

It has to be noted that

India has a large Trade Deficit with China, Saudi Arabia, Iraq, Germany, South Korea, Switzerland and Indonesia.

India has been diversifying its export destinations. E.g., South Africa, Brazil, Saudi Arabia etc.

Part 2: Capital Account

The Capital Account is the second account, recording all international purchases and sales of assets such as money, stocks, bonds, etc., for a specified time, usually a year.

Investment – FDI & FPI

What constitutes Foreign Direct Investment (FDI) ?

According to Arvind Mayaram Panel, more than 10% of equity investment made by a foreign entity into an Indian company with the motive of getting involved in the management of that Indian company is known as FDI.

E. g. : Walmart of USA has 77% stakes in Flipkart.

What constitutes Foreign Portfolio Investors (FPI) ?

FPIs are foreign entities registered with SEBI and have up to 10% equity in an Indian Company.

FPIs are not involved in the management of a company. Their primary motive is to earn profit by buying and selling shares.

Note: Till 2019, the summation of all the FPIs in a company could be at most 24%. But in the 2019 Budget, the government removed the 24% cap.

Sector-wise Foreign Investment (FDI + FPI) Limit

Note: The list is not exhaustive and keeps changing frequently. For the latest limits, please cross-check government sources as well

100% FDI allowed

1. Single Brand Retail 2. E-commerce (marketplace model) 3. Defence Industry 4. Railway Infrastructure (Construction, operation and maintenance) 5. Industrial Parks 6. Telecom services 7. Pharma Companies 8. Contract manufacturing 9. Asset Reconstruction Company (ARC) 10. Floriculture, Horticulture, and Cultivation of Vegetables 11. Animal Husbandry, Pisciculture, Aquaculture, Apiculture 12. Plantation : Only in plantations of Tea, Coffee , Rubber , Cardamom , Palm oil and Olive oil tree plantations 13. Airports (both Greenfield and Brownfield projects) 14. Air Transport Services 15. Maintenance and Repair in air transport 16. Mining and Exploration of metal and non-metal ores 17. Coal and lignite 18. Exploration activities of oil and natural gas fields 19. DTH and Cable Networks 20. Non-news channels

74%

1. Private Banks 2. Private Security Agencies

51%

1. Multi Brand Retail Trading

49%

1. Insurance Company 2. Pension Sector Companies 3. Power Exchanges 4. FM and News channels

26%

1. Digital Media 2. Newspapers and periodicals

20%

1. Public Sector Banks

Prohibited

1. E-commerce ( inventory based model ) 2. Atomic energy 3. Railway operations (except Metro) 4. Tobacco Products like cigars , cigarillos and cigarettes 5. Real Estate Business and Farm Houses 6. Chit Funds and Nidhi Companies 7. Betting , Gambling, Casino & Lottery.

Foreign Investment Promotion Board (FIPB)

Foreign Investment is permitted either through:

Automatic Route: i.e. Foreign entities don’t require Indian Government’s approval.

Government Route: i.e. Approval of the Government is required prior to investment.

Earlier, this approval was given by FIPB. But, Budget 2017 removed this Board to promote Ease of Doing Business by removing Red-Tapism in bureaucratic decision-making and reducing the time for mergers and acquisitions.

Now, Government approval is given by the Commerce Ministry after consultation with the subject ministry.

FDI in India

1. Sector Wise

Sectors receiving maximum FDI in India are

Computer Hardware

& Software (44%)

Construction (13%)

Services (8%)

2. Country-wise

Countries with maximum FDI in India are

Singapore

Mauritius

UAE

USA

3. States with Maximum FDI

Indian states having maximum FDI are

Gujarat (27%)

Maharashtra (27%)

Karnataka (13%)

4. State Wise Analysis

A state-wise analysis of FDI

inflows to different Indian states shows a clear regional disparity in FDI

inflows. Delhi, Haryana, Maharashtra, Karnataka, Tamil Nadu, Gujarat and

Andhra Pradesh have together attracted more than 70 % of total FDI inflows

to India during the last 15 years.

However, states with vast

natural resources, like Jharkhand, Bihar, Madhya Pradesh,

Chhattisgarh and Odisha, have not been able to attract foreign funds

directly for

investment in different sectors.

What government has done to attract FDI ?

The Government has abolished Foreign Investment Promotion Board (FIPB)

A number of sectors have been opened for FDI, including defence, construction, broadcasting, civil aviation etc.

Investor Facilitation Cell has been created under Invest India Program to guide, assist & handhold investors.

For some countries like Japan, a special program like Japan Plus has been started.

The Insolvency and Bankruptcy Code has been passed to make an exit from non-viable businesses easier.

“Foreign Investment Facilitation Portal (FIF Portal)” has been launched as the online single-point interface of the Government of India for investors to facilitate Foreign Direct Investment.

FDI & FPI Trends in India (2018-19)

FDI

FDI is positive for India as India attracts significant investments in FDI.

FPI

– There is no general trend for FPI, and it can be positive or negative depending on the situation. – In FY 2023, there was a net outflow of the FPI (mainly due to Fed Tapering).

Fed Tapering and FDI

The US

and other advanced economies are witnessing very high rates of inflation due to

the following reasons

Loans

were provided at an ultra-low interest rate during the Covid pandemic to

boost the economy.

Supply chain disruptions due

to the Russia-Ukraine war.

To combat inflation, the Federal Bank of America (the equivalent of RBI of India) has started to increase their Repo Rate, thus making the loans expensive in the USA. This process is known as Fed Tapering.

Fed Tapering has an impact on India and other developing economies as well. When the Feds were following Easy Money Policy, US investors were investing their excess funds in India and other developing economies as the rate of return on the US bonds was extremely low. But when Feds started to increase Repo Rate, the Bond Yield on US bonds increased, and investors started to take their money out of India. E.g., the bond yield on a 10-year US bond was 0.54% in July 2020 and raised to 3.30% in Feb 2023.

Overall,

Fed Tapering has the following impacts on the Indian economy

Flight of FPI and FDI from India (as explained above)

The flight of investment leads to a fall in Rupee vis-à-vis US Dollars

The inflation from the US economy is exported the world over.

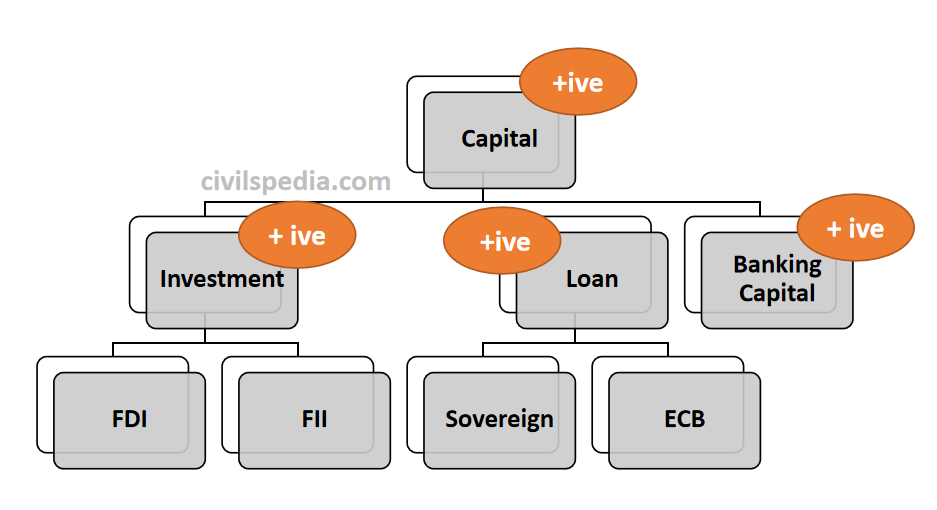

Loans

In loans, the Indian account is +ive.

Internally, Private External Commercial Borrowing is more than Sovereign foreign debt.

Such loans are beneficial during good times as borrowers could enjoy the benefits like lower interest rates, longer maturity, and capital gains. But sharp depreciation in local currency would mean a corresponding increase in debt service liability, as a more domestic currency would be required to buy the same amount of foreign exchange.

Composition of Indian Debt

Tenure Wise

Long Term (78%) more than Short Term (22%)

Sector Wise

Private Sector (80%) more than Public Sector (20%)

NRIs can deposit their $ (or other foreign currency) in Indian Banks via FCNR Accounts.

Interest to be paid on FCNR deposits is tied up with LIBOR (London Interbank Offered Rate).

Capital Surplus

India’s Capital Account is in Surplus.

Balance of Payment condition of India

The outcome of the total transactions of an economy with the outside world in one year is known as the Balance of Payment (BoP) of the economy. It is the net outcome of an economy’s current and capital accounts.

The Balance of Payment can be positive or negative. However, negative doesn’t mean it is unfavorable for the economy until it has the means to fill the gap with the help of its forex reserves.

Various conditions

Positive BoP

If the Balance of Payment is positive at the end of the year, the money is automatically transferred to the foreign exchange reserves of the economy.

Negative BoP

If the Balance of Payment is negative at the end of the year, the foreign exchange is drawn from the country’s forex reserves.

If the forex reserves cannot fulfil the negativity created by the BoP, it is known as a BoP crisis. India faced such a situation in 1991 when India was forced to take forex help from the IMF.

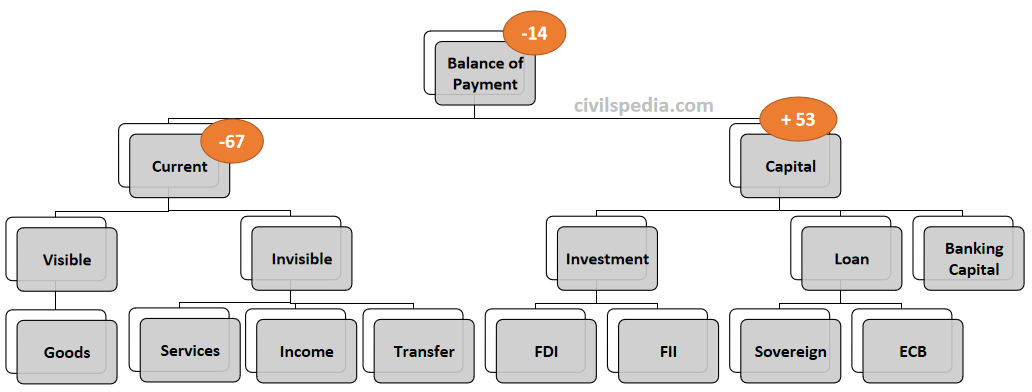

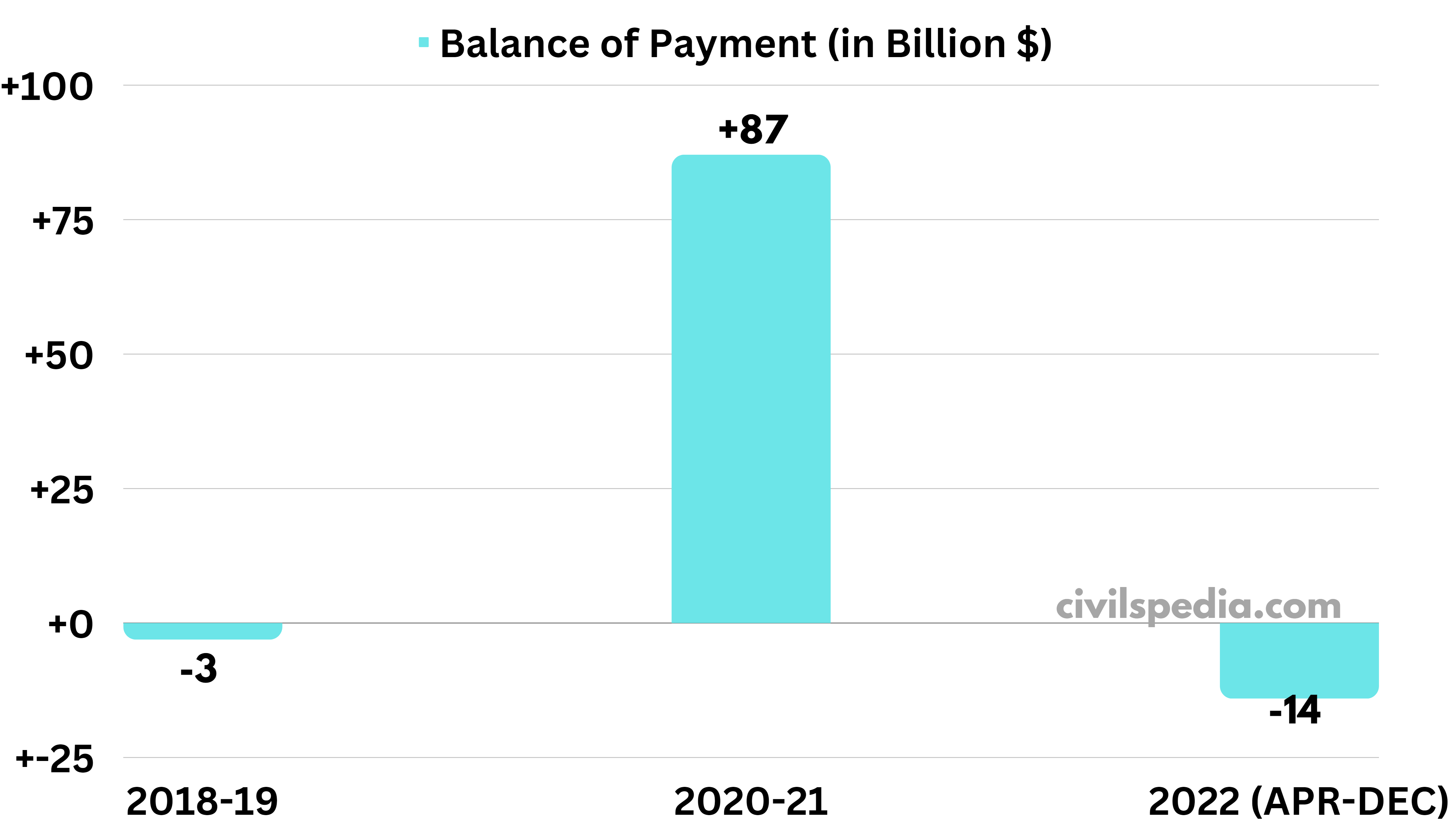

India’s BoP position (for 2022-23)

Only preliminary data was

presented in the Economic Survey (2023). For period Apr-Dec 2022, India

Balance of Payment -14 billion.

But India has forex reserves of more than $ 560 billion. Hence, India faced no problem in bridging the gap.

This article deals with ‘Theories on International Trade .’ This is part of our series on ‘Economics’ which is important pillar of GS-3 syllabus . For more articles , you can click here .

Introduction

International Economics is

that branch of economics which is concerned with the exchange of goods and

services between two or more countries .

The subject matter of

International Economics includes large number of segments :-

Pure Theory of Trade : It includes issues like causes for foreign

trade, composition, direction and volume of trade, exchange rate, balance of trade and balance of

payments .

Policy Issues : It includes

policy issues such as free trade vs. protection, use of taxation,

subsidies and dumping, currency convertibility, foreign aid, external

borrowings and foreign direct investment.

International Cartels and

Trade Blocs .

International Financial and

Trade Regulatory Institutions : Most important of which are IMF, WTO and World Bank.

Theories of International Trade

1 . Mercantilist Theory

It takes an us-versus – them view of trade.

According to Mercantilist

Theory, World Trade remains same. Hence, one country gains by damaging the

other. Increase in trade of one country means loss of some other country.

Hence, nation’s wealth and power are best served by increasing exports and

receiving payments in gold, silver and precious metals.

From the 16th to 18th century,

economists believed in mercantilism. One of the leading proponent of

Theory of Mercantilism was Thomas Munn (Director of English East India

Company) .

2 . Adam Smith’s Theory of Absolute Cost Advantage

Adam Smith was in favour of free trade.

According to Adam Smith, the basis of international trade was absolute cost advantage. Trade between two countries would be mutually beneficial when one country produces a commodity at an absolute cost advantage over the other country which in turn produces another commodity at an absolute cost advantage over the first country.

Example / Illustration

Take

example of India and China in production of Wheat and Cloth . Suppose, one

labourer in India can produce 20 units of wheat and 6 units of cloth while that

in China can produce 8 units of wheat and 14 units of cloth.

Country

Wheat production by one labourer

Cloth production by one labourer

India

20 units

6 units

China

8 units

14 units

Hence, India has an

absolute advantage in the production of wheat over China and China has an

absolute advantage in the production of cloth over India. Therefore, India

should specialize in the production of wheat and import cloth from China. China

should specialize in the production of

cloth and import wheat from India. This kind of trade would be mutually

beneficial to both India and China.

3 . Ricardo’s Theory of Comparative Cost Advantage

According to David

Ricardo’s Theory of Comparative Cost Advantage , a country can gain from

trade when it produces at relatively lower costs. It means, even when a

country enjoys absolute advantage in both goods, the country would

specialize in the production and export of those goods which are

relatively more advantageous. Similarly, even when a country has absolute

disadvantage in production of both goods, the country would specialize in

production and export of the commodity in which it is relatively less

disadvantageous .

Example / Illustration

Units of labour required to produce one unit

Cloth

Wheat

Domestic Exchange Ratios

USA

100

120

1 wheat =1.2 cloth

India

90

80

1 wheat=0.88 cloth

In the

illustration, India has an absolute

advantage in production of both cloth and wheat. However, India should concentrate on the

production of wheat in which she enjoys a comparative cost advantage. For

America the comparative cost disadvantage is lesser in cloth production. Hence

America will specialize in the production of cloth and export it to India in

exchange for wheat.

4 . Heckscher and Ohlin’s Factor – Proportions Theory

Capital-abundant country will

export the capital –intensive goods. E.g. USA exporting Aeroplanes

Labour-Abundant Country will

export labour-intensive goods. E.g. India exporting cotton .

Last Updated: May 2023 (Industrial Policies of India)

Industrial Policies of India

This article deals with ‘Industrial Policies of India.’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Introduction

‘Industrialize or perish!’ – M. Visvesvaraya

Statistics about the Manufacturing Sector

With the

development of the economy, the percentage of people engaged in industry is

increasing, and its contribution to the net GDP of India is increasing as well.

a . Percentage of Indians employed in Manufacturing Sector

In 2018, 24% of Indians were employed in the Industrial sector.

b . Contribution of Manufacturing in India’s GDP

Its contribution to India’s total GDP is 29% (in 2018).

c . Indian companies in Fortune-500

There are 7 Indian companies on the Fortune-500 list. These are

Reliance Industries

155

State Bank of India

205

Indian Oil

212

ONGC

243

Rajesh Exports

348

Tata Motors

357

Bharat Petroleum

394

d . Growth Rate

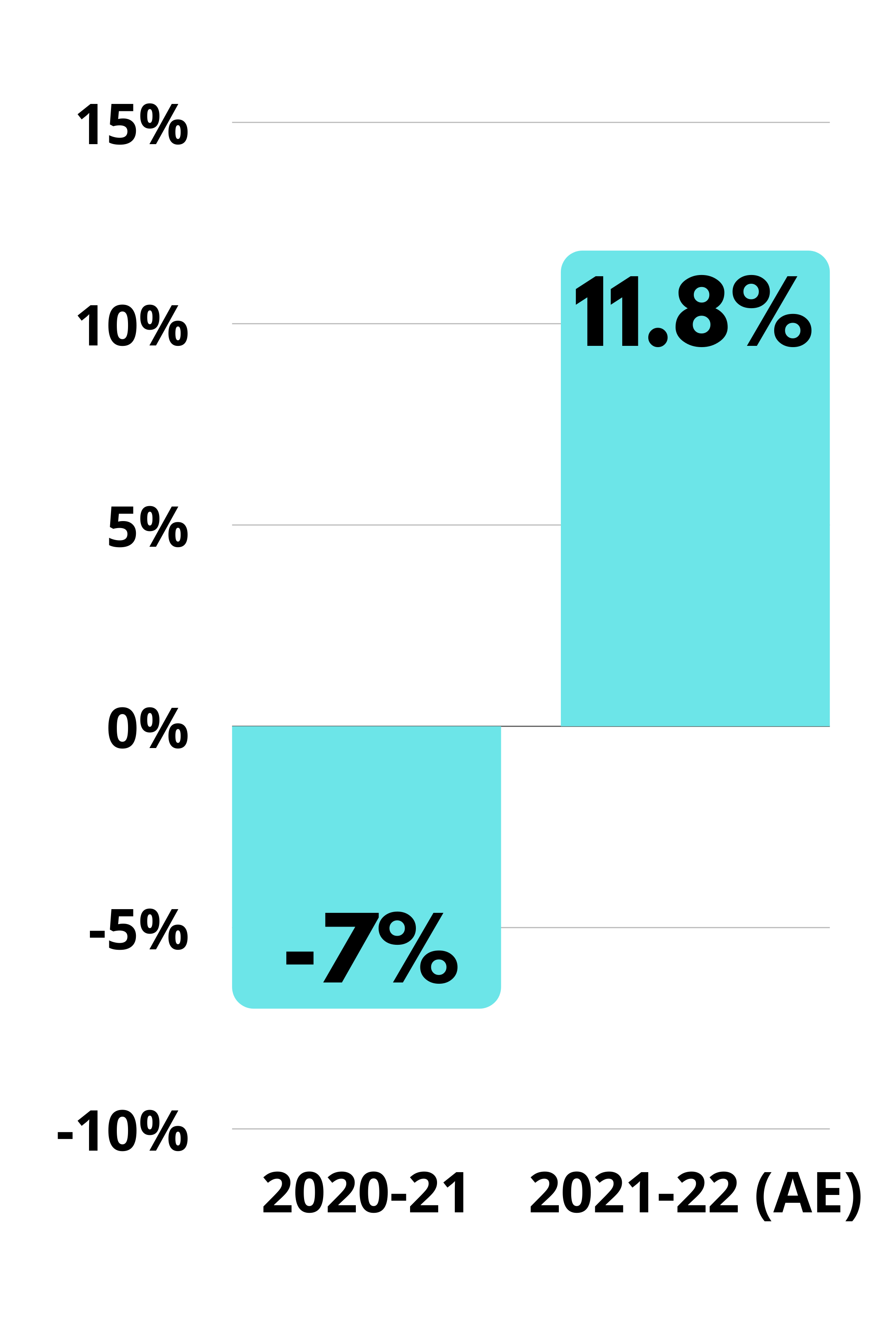

The covid pandemic badly hit the growth rate of the industrial sector. But it has revived again and witnessed the growth of 11.8% in 2021-22.

Indian Industrial Policies – History

Industrialization is sine quo none for the economic development of any country. At Independence, India inherited a weak and shallow industrial base. Therefore, during the post–Independence period, the Government of India emphasized the development of a solid industrial base.

The Government of India has declared its Industrial policies at various times, which has changed the trajectory of the Indian economy.

Industrial Policy Resolution, 1948

It was announced in 1948.

It was decided that model of the economy would be ‘Mixed Economy’. It divided the economy into the following three lists

Central List

Important industries were here like coal, power, railways, civil aviation, ammunition, defence etc.

State List

Industries of medium importance were put here – medicine, textile, cycles, 2 wheelers.

Rest industries

All rest industries were left open for all private sector investment, with many having compulsory licensing provisions.

The policy was to be reviewed after 10 years.

Industrial Policy Resolution,1956

The government was

encouraged by previous success & announced it after 8 years only. This

policy structured the nature of the economy till 1991.

Main provisions of Policy

1. Reservation of Industries

A

clear-cut classification was made into three schedules

Schedule A

– It contains 17 areas in which the centre enjoyed a monopoly. – Industries set up under this provision were called Public Sector Undertakings (PSUs). – PSU included those industries as well, which were taken over between 1960 and 1980 under the nationalization drive.

Schedule B

– Schedule B consists of 12 areas where the state was supposed to take up the initiative with more expansive follow-up by the private sector. – It also included the provisions of Compulsory licensing. – Neither state nor private sector had a monopoly in these industries.

Schedule C

– Schedule C consists of all the areas not covered in Schedule A & B. – The private sector has provisions to set up industries. – Many of them had provision of licensing.

2. Provision of Licensing

All Schedule B & several Schedule C industries came under this.

This provision is also called LICENSE- QUOTA -PERMIT RAJ.

3. Expansion of Public Sector

The policy announced to expand the public sector for accelerated industrialization & growth of the economy.

Emphasis was on heavy industry.

4. Regional Disparity

Upcoming PSUs were set up more in backward areas (although it was entirely against the ‘Theory of Industrial Location’).

5. Emphasis on Small Industry

The policy was committed to promoting small-scale industries and the Khadi & Village industry.

6. Agriculture Sector

The agriculture sector was pledged as a priority.

Industrial Policy of 1969

It was aimed at solving the shortcomings of the Industrial Policy of 1956.

Experts & industrialists believed that licensing was serving the opposite purpose than it was mooted. The main aim behind the ‘Licensing policy’ was socialist & nationalist feeling so that

The exploitation of resources could be done for the development of all.

Price-control of goods purchased from licensed industries.

Checking concentration of economic power.

Channelizing investment into the desired direction.

But licensing policy wasn’t serving this purpose as

Influential industrial houses were able to procure new licenses at the expense of budding entrepreneurs.

Older & well-established business houses were capable of creating hurdles for new ones with the help of different kinds of trade practices & forcing the latter to agree to sell out & takeovers.

Industrial Policy of 1969 introduced the Monopolistic & Restrictive Trade Practices(MRTP) Act. The main features of the MRTP act were

It was aimed at checking & regulating trade & commercial practices of the firms and checking the monopoly & concentration of economic power.

Firms with assets worth ₹ 25 crores (which was later increased to ₹50 crores in 1980 and ₹100 crores in 1985) or more were obligated to take permission from the Indian government before expansion, greenfield venture & takeover of other firms.

For redressal of prohibited & restricted practices of trade, the government set up the MRTP Commission.

Industrial Policy Statement, 1973

1. Core Industries

The policy introduced a new classification of ‘Core Industries’.

It included six industries that were of fundamental importance for developing other industries – Iron & Steel, Cement, Coal, Crude Oil, Oil Refining & electricity.

Note: At that time, there was 6 Core Industries. Now there are 8

Coal

Crude Oil

Cement

Fertilizer

Electricity

Refinery Products

Natural Gas

Steel

2. Private Companies

Private Companies may apply for licenses under Core industries if they aren’t covered under Schedule A.

They were eligible only if their total assets were above ₹20 crores.

3. Reserved List

Some industries were put under a reserved list in which only MSME could set up industry.

4. Joint Sector

It allowed partnership between centre, states & private sector for setting up some industries.

The government had discretionary power to exit such ventures in future.

The intention was to promote the private sector with government support.

5. FERA

Foreign Exchange Regulation Act was introduced to regulate foreign exchange in India.

According to experts, it was draconian law that hampered the country’s growth.

6. Foreign Investment

Limited permission of foreign investment was given, with MNCs being allowed to set up subsidiaries in India.

Industrial Policy Statement, 1977

Political set up at the centre changed so did economic policy.

There was more inclination towards Gandhi -Socialistic view & anti-Indira stance.

Main Features

Foreign investment in unnecessary areas prohibited ( in practice, it was complete no). During this period, Coca-Cola, IBM and Chrysler were made to exit India.

Emphasis was placed on village industry with a redefinition of small & cottage industry.

Decentralized industrialization was given attention to link masses to the process of industrialization.

Khadi & Village industry was to be reconstructed.

Serious attention was given to the level of production & prices of essential of everyday use.

Industrial Policy Resolution, 1980

The

Congress party returned to power. As a result, Industrial Policy was revised in

1980. The main provisions of this policy were

Foreign investment via technology transfer route was allowed.

MRTP limit was increased to ₹50 crores to promote the setting up of bigger industries.

Industrial licensing was justified.

Overall

liberal attitude followed towards the expansion of private industries.

Industrial Policy Resolution of 1985 & 86

Industrial Policy Resolutions of 1985 & 86 were very similar in nature & latter tried to promote initiatives of the former. The main provisions of this policy were

Foreign investment was further simplified & more areas were opened for foreign investment. The dominant method of foreign investment was still technology transfer, but foreign MNC can hold up to 49% in their subsidiary.

MRTP limit was increased to ₹100 crores.

Provision of industrial licensing was further simplified & remained for 64 industries only.

A higher level of attention was given to sunrise industries such as telecommunication, computerization & electronics.

The modernization & profitability aspects of PSU was emphasized.

FERA regime was relaxed.

Many technology missions were launched in the Agricultural sector.

It has to be noted that these policies were formulated when the developed world was going towards forming the World Trade Organization.

These provisions were attempted at liberalizing the economy without any slogan of economic reform. The government wanted to go for the kind of economic reforms India pursued after 1991 but lacked political support.

By the end of the 1980s, India was in the grip of a severe Balance of Payment crisis with higher inflation (over 17%) & a high fiscal deficit (8%). It was magnified by the Gulf war & the high prices of oil, ultimately leading to the Balance of Payment crisis, IMF bailout & 1991 LPG reforms.

India was in a severe Balance of Payment crisis in 1991. Reasons for this were several interconnected factors that were growing unfavourable for the Indian economy

Gulf war of 1990-91: Oil prices increased, leading to fast depletion of Indian Foreign currency reserves.

There was a sharp decline in private remittances from overseas Indian workers in the Middle East in the wake of the gulf war.

Inflation peaked at 17% & the central government’s fiscal deficit reached 8.4%.

By June 1991, Indian Forex declined to just 2 weeks of import coverage.

The financial support that India got from the IMF to fight out the Balance of Payment crisis of 1990-91 had a tag of structural readjustment as a condition to be fulfilled by the Government of India.

With this policy, the government kickstarted the very process of reform in the economy. That is why the policy is taken more as a process than a policy.

New Industrial Policy of 1991

Triple pillars of New

Economic Policy were Liberalization, Privatization and Globalization (LPG)

1. Liberalisation

1.1 De Licensing of Industries

The

number of industries put under the compulsory licensing provision (Schedule B

& C) was cut down to 18 in 1991. Now

only 5 industries require a license, and these are

Industries that were

reserved for the Central government in the Industrial Policy of 1956 were cut down to 8 from 17 at

that time. Presently only

three sectors are reserved for central government.

Nuclear Energy

The present government is seriously considering allowing the private sector to enter the management of nuclear power plants.

Nuclear research

Consist of mining, use, management, fuel fabrication, export-import, waste management of radioactive material & no country allows private industry in this.

Railways

Many of the functions related to railways have been allowed private entry, but still, the private sector can’t enter as a full-fledged railway service provider.

1.3 Location of industries

Industries were

categorized into polluting & non-polluting & highly simple provision

deciding their location was announced

Non-Polluting

Such industries can be set up anywhere.

Polluting

Such industries can be set up at least 25 km away from million cities.

1.4 Abolition of phased production

The compulsion of phased production was abolished.

Now private firms can go for production of as many goods & models simultaneously as they want.

1.5 Abolition of MRTP

The MRTP limit of ₹ 100 cr was abolished.

MRTP Act was replaced by Competition Act & MRTP commission was replaced by Competition Commission of India (CCI).

2 . Privatisation

2.1 Privatizing PSUs

It was decided to convert the public sector companies to private sector companies by reducing Government shareholding to below 50%. E.g., Hindustan Zinc Limited.

2.2 Stopped Nationalization

The policy stopped the practice of nationalization. It means that the way Tata Airlines was nationalized to Indian Airlines or Banks were nationalized will not be used by the government in the future.

2.3 More sectors opened

Private sector companies were allowed to operate in banking, insurance, aviation, telecom and other sectors.

3 . Globalization

3.1 Joined WTO

India joined the WTO regime & gradually relaxed the tariff and non-tariff barriers on the imported goods and services.

3.2 Promotion of Foreign Investment

Promotion of foreign investment was encouraged through both routes, i.e. Foreign Direct Investment & Foreign Portfolio Investment.

3.3 FERA by FEMA

Draconian FERA was replaced with the Foreign Exchange Management Act (FEMA), which came into effect in 2000-01 with a sunset clause of two years.

Need of New Industrial Policy

Why we need a new Industrial Policy?

Technological changes like the 4th Industrial Revolution, Artificial Intelligence & Automation have changed the nature of industries.

Systemic issues in the economy: Indian economy faces a large number of systemic issues such as outdated labour laws, infrastructural bottlenecks, logistic weakness etc.

Changes in Demographic conditions: With an increasing number of old age people, the government needs to focus on Longevity Dividend and the Demographic Dividend.

Global Changes: The world has changed, and China is losing Demographic Dividends. India needs to take drastic steps to fill the vacuum.

The Indian economy has changed drastically since 1991. The service sector is contributing the highest share to Indian GDP.

The rise of Multilateral Trade Agreements poses a threat to the Indian economy.

India needs to formulate a new Industrial Policy to deal with the problem of Climate Change and comply with Paris deal obligations.

What should New Industrial Policy focus on?

Technology & Innovation: Government should provide incentives for artificial intelligence, the internet of things, and robotics.

The Ease of Doing Business should be emphasized to attract MNCs in India.

Infrastructure should be made world-class to end the logistic problems of the Indian economy.

More focus on the skills & employability of new workers.

The focus should be on labour-intensive sectors such as textiles, leather and footwear industries etc.

Sustainable and responsible industrialization to reduce carbon emissions should be emphasized.

Provide easy access to capital to the MSMEs.

Create global brands out of India.

Promote Innovation and R&D via Academia- industry linkages, transparent IPR regime and encouragement to Startups.

Side Topic: National Manufacturing Policy, 2011 & NMIZ

Aim

Increasing the manufacturing sector’s share in Indian GDP to 25% by 2022.

Target is to create 100 million jobs.

Create National Manufacturing & Investment Zone (NMIZ)(NMIZ is an essential component of NMP, 2011).

NMIZ/National Manufacturing & Investment Zone

NMIZ is an ‘industrial township’ containing Special Economic Zones, Industrial Parks etc.

NMIZ are given additional support by the government in the form of

Tax incentives

Relaxed norms for FDI approval

Providing Rail, Road, energy etc.

Relaxations in the labour laws, e.g. easier hiring-firing norms.

NIMZ is treated as a self-governing body under Article 243(Q-c) of the Constitution.

India has 15 NMIZ like Manesar-Bawal Investment Region in Haryana etc.

This article deals with ‘Assemble in India.’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Introduction

Economic Survey (2020) points towards the fact that in just the five years 2001-2006, labour-intensive exports enabled China to create 70 million jobs for workers with just primary education.

But now, firms are looking for alternatives because

US-China trade war: The US has placed significant tariffs on products manufactured in China.

Increase in wages in China.

Companies have recognized the strategic vulnerability due to all supply chains concentrated in China.

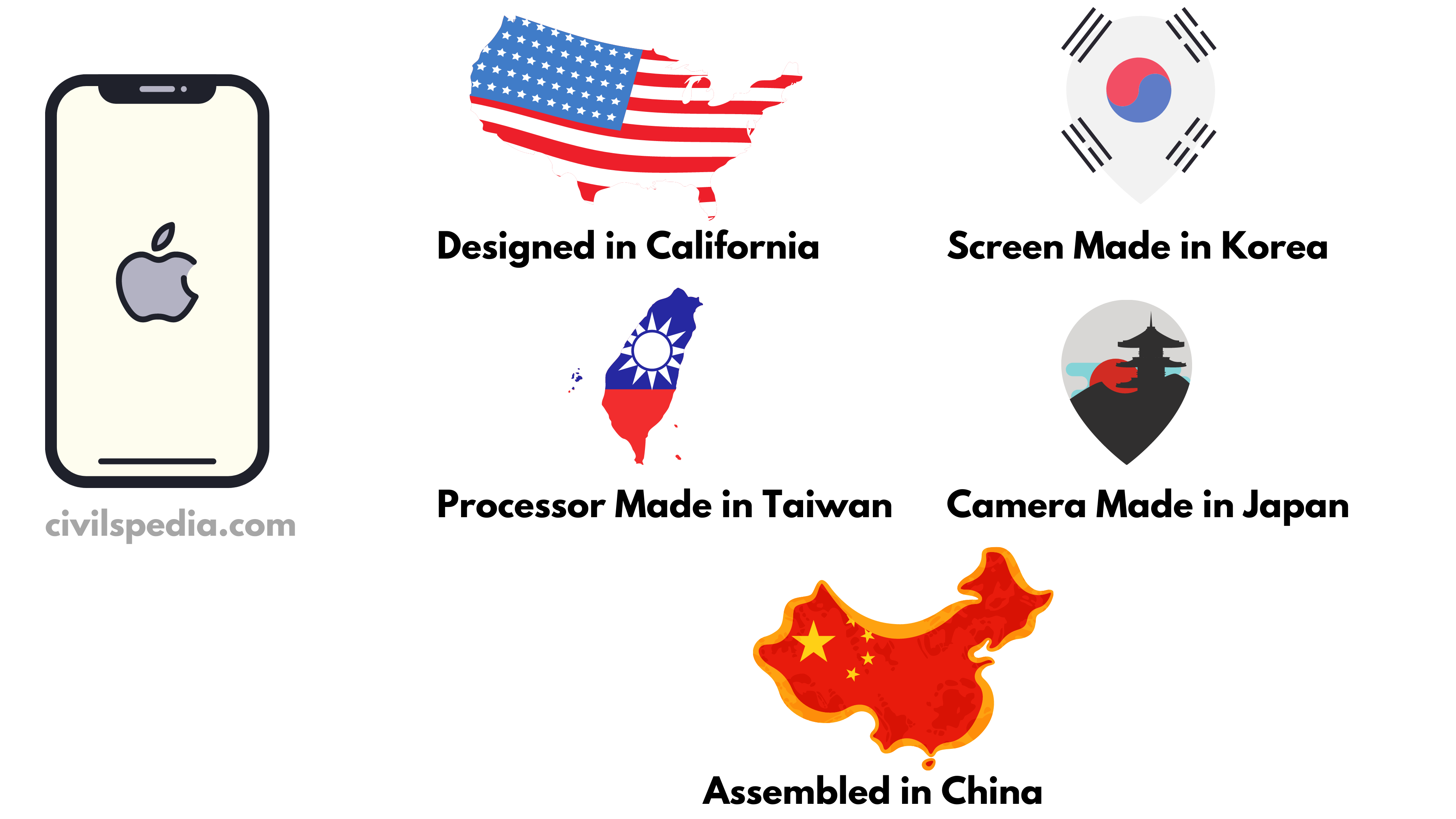

Side Note: Network Product

In modern production lines, the entire production is not done at a single place. Instead, different components are made at different locations and then integrated in some third place to make the final product. Such a final product is known as Network Product.

Take the example of the iPhone.

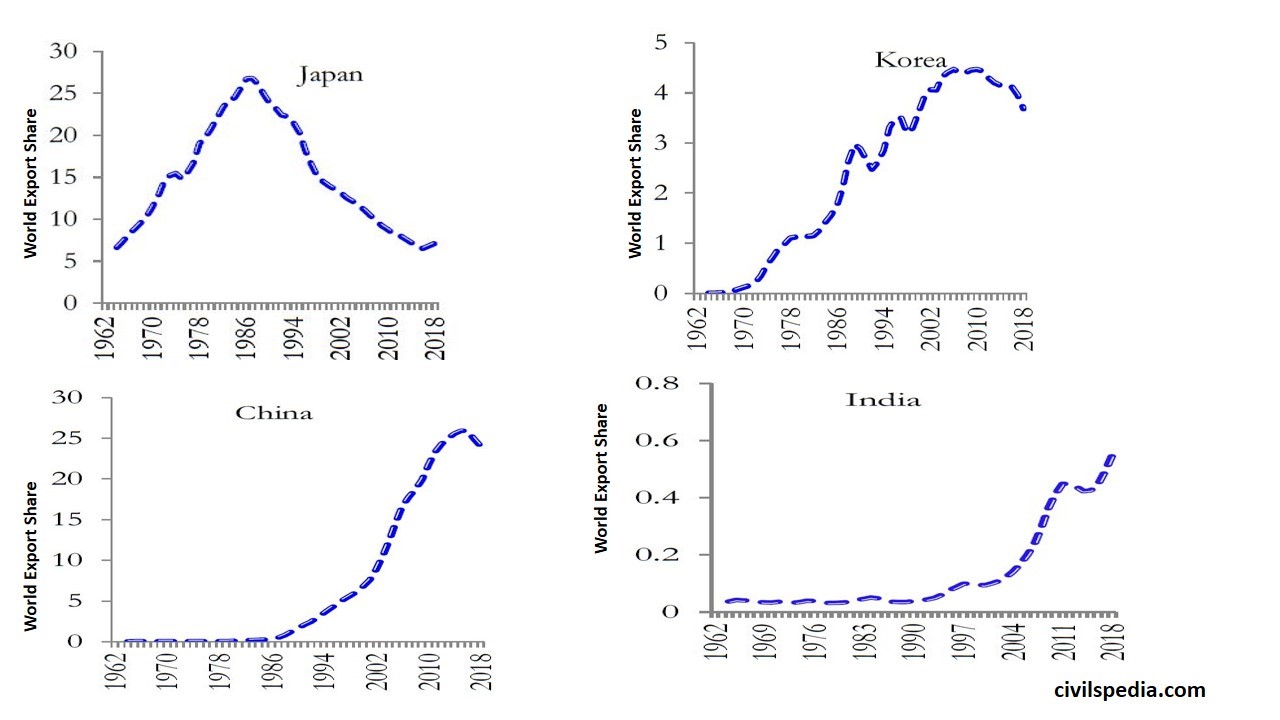

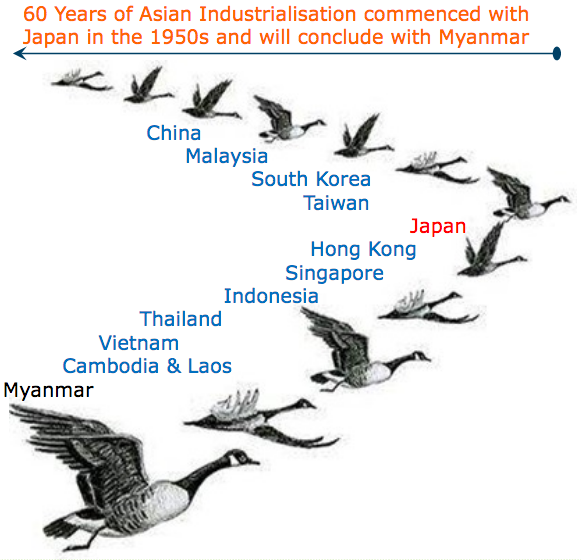

Wild Geese Flying Model

The pattern of entry, rise, survival, and the relative decline of countries in the export market for Network Products follows the “wild-geese flying model”.

This process started with Japan which later moved to South Korea, Taiwan and China and so on.

Japanese Companies (like Sony) first started to assemble Cameras, TVs, Walkman etc. When labour costs rose, they shifted their manufacturing to South Korea.

Then South Korean Companies like Samsung and LG grew in the export of Network Products. After some time, due to cost issues, they outsourced their manufacturing to China and Taiwan.

Hence, Network Goods assembly will continue to move from more advanced countries to less advanced countries. (CLICK HERE)

Economic Survey believes that while Japan is in a declining stage, most countries, including China, have reached the inflexion point. India is at the right stage to take the place of China in the assembly of Network Products, thus providing us sufficient opportunity to grab.

Why India should focus on Network Products and Assemble in India?

MNCs are moving away from China due to the trade war between China and US, along with rising wages in China. Hence, India should grab the opportunity to shift a large chunk of Assembly Lines from China to India.

Network Products accounted for nearly 30 per cent of world exports in 2018. Although India has much potential, India lags in exporting Network Products. In 2018, Network Products exports accounted for 10% of India’s export basket, while these products accounted for about 50% of China, Japan, and Korea’s total national exports.

Economic Survey (2020) suggests that by integrating “Assemble in India for the world” into Make in India, India can raise its export market share to about 3.5% by 2025 and 6% by 2030. In the process, India would create nearly 4 crore well-paid jobs by 2025 and about 8 crores by 2030.

Reforms required

To attract MNCs to Assemble in India, India needs to

Reform Taxation laws

Reform Labour Laws

Skill training of workers and mid-level supervisors.

Invest heavily in infrastructure and create world-class roads, railways and ports.

Sign a large number of Free Trade Agreements so that India becomes part of Global Value Chains

While the short to medium-term objective is the large scale expansion of assembly activities by making use of imported parts & components, the long term objective should be giving a boost to domestic production of parts & components (and create global giants like Samsung developed in Korea and Xiaomi, Huawei etc. developed in China).

This article deals with ‘Make In India (MII).’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

What is Make in India (MII)?

MII is a program started by the Government of India to make India a global hub of manufacturing, design, and innovation.

Why do we want to Make in India?

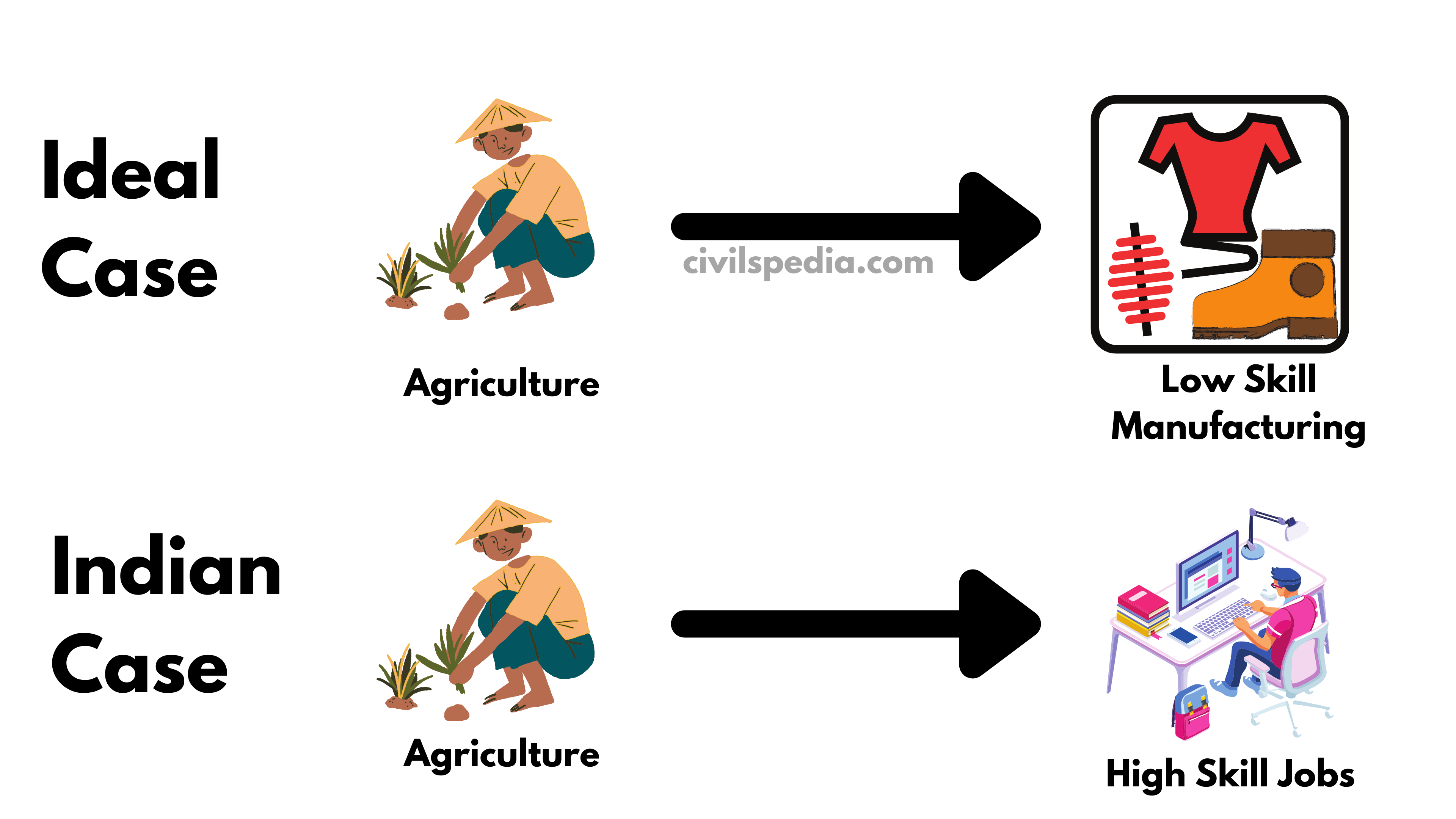

Remove excess of population in Agriculture to be employed in Manufacturing Sector.

To reap Demographic Dividend by providing jobs to the youth in the manufacturing sector.

Use Cheap Labour available in the country to fill the lacunae left by China, where labour wages have risen.

We have substantial domestic demand in India & still importing from abroad. Why not make it in India & save our foreign exchange?

To address issues created by the fact that India directly jumped from Agricultural to Service sector economy without first passing through low skill manufacturing economy.

The need for a dedicated government policy to support domestic industrialization amidst foreign competition can be better appreciated from the industrialization experiences of East Asian economies such as South Korea & Taiwan in 1960-1990. These countries supported their domestic industries during their high growth phase while also ensuring healthy competition required for the industries to grow

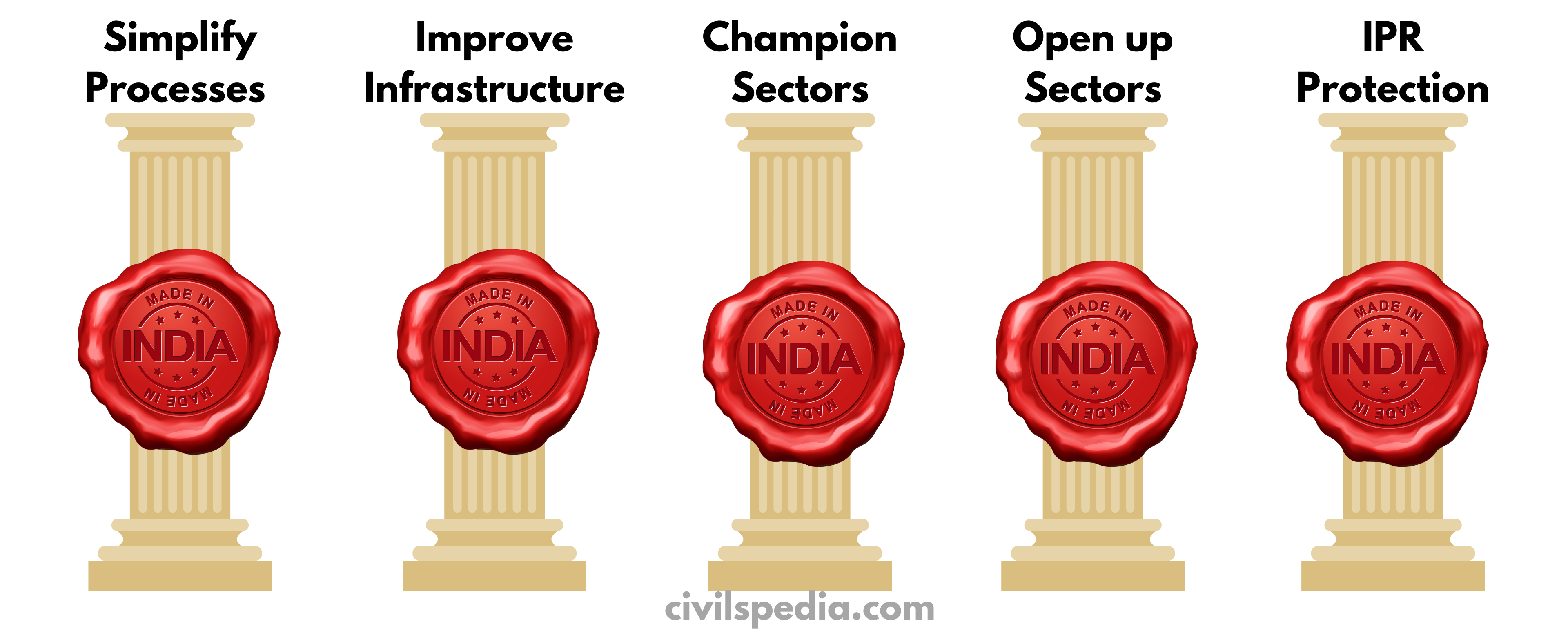

Make In India: 5 Pillars

1. Simplify Processes

Ease the regulatory framework and cut red-tapism to invest easily, and entrepreneurs can set up industries.

2. Improve Infrastructure

End infra bottlenecks by investing in new Industrial corridors, smart cities, roads, railways and world-class ports.

3. Focus on Sectors

The government has recognized 27 sectors under Make in India 2.0 (as of 2023), where

India has the potential to become the global champion.

Which can drive double-digit growth in manufacturing.

Generate significant employment opportunities.

These include

Manufacturing Sectors: Capital goods, Auto, Defence & Aerospace, Biotechnology, Pharmaceuticals, Food Processing, Gems & Jewellery, New & Renewable Energy, Construction, Shipping and Railways.

Service Sectors: IT, Tourism & Hospitality, Medical Tourism, Logistics, Legal Services, Educational Services etc.

4. Open up Sectors

India will open new sectors for investment.

5. IPR protection

Protection & Promotion of Intellectual Property Rights like Patents, GI, Copyrights, Trademarks and Industrial Designs.

Initiatives in various sectors to promote Make in India

1. Production-linked incentive (PLI) scheme

Production Linked Incentive refers to a rebate given to producers. This rebate is calculated as a certain percentage of incremental sales by the producer.

The scheme is applicable on Automobiles, Advanced Chemistry Cell (ACC) Battery, Pharma, Telecom, Food Products, Textile, Specialty Steel, White Goods (home appliances), Electronic goods and Solar Modules.

E.g., As a part of the PLI scheme for mobile and electronic equipment manufacturing, an incentive of 4-6% on incremental sales is given to electronic companies manufacturing mobile phones, transistors etc.

This scheme is in line with India’s Atmanirbhar Campaign.

Total of Rs. 1.45 trillion will be given in 5 years.

The design of the earlier PLI scheme is such is compatible with WTO as the support is not linked to exports or value-addition.

2. Defence and Aviation Sector

Defence Procurement Procedure (DPP): The government will prioritise the indigenously designed, developed and manufactured (IDDM) equipment.

Defence Offset Norms: When the government buys defence equipment from a foreign company, foreign companies have to procure a certain percentage of components from India.

3. Food Processing

The government is encouraging the opening up of new Mega Food Parks.

The government has started SAMPADA Scheme to promote Food Processing Industry.

4. Automobiles