Last Updated: May 2023 (Investment Funds)

Table of Contents

Investment Funds

This article deals with ‘Investment Funds.’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here .

Introduction

- It is quite difficult for ordinary people to understand economic concepts and invest in bonds and equity after analyzing the market. There is an easy option for such people to invest in Investment Funds that gather money from ordinary people to invest in such securities and other projects and are managed by Fund Managers with expertise in financial matters.

- Fund Managers take money from investors and give them units made with the backing of investments.

- Later, Manager gets a return from the investments in the form of interest, dividend, charges etc. and distribute this return among Investors based on the share they have in Fund after cutting his fee.

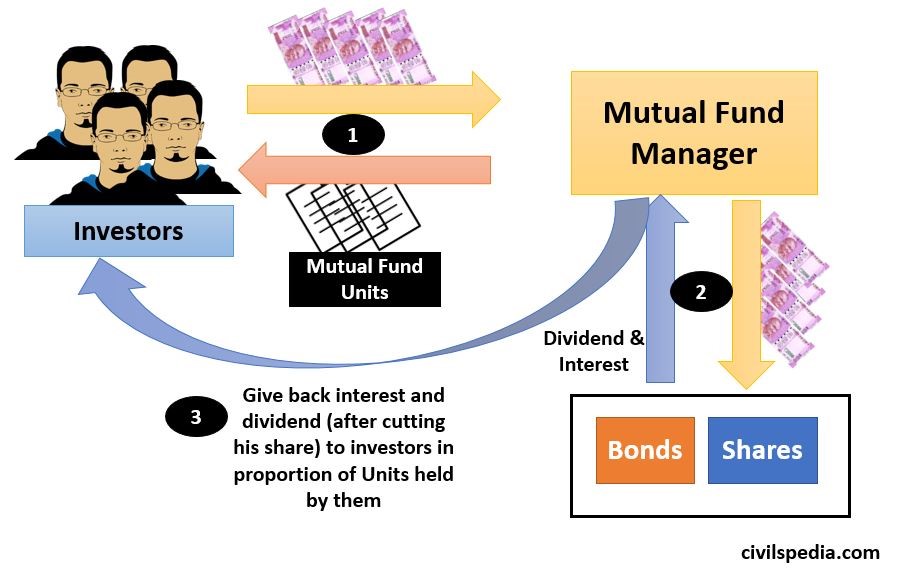

1. Mutual Funds

- Mutual Fund Manager is a financial intermediary.

- Mutual Fund Manager mops up money from a group of investors to invest in different asset classes like shares, bonds etc., to generate returns for investors. In return, the Manager gives Units backed by the assets to the Investors.

- When a Mutual Fund manager gets returns in the form of dividends and interest from the assets in which investors’ money was invested, it is distributed among investors in the proportion of Units held by them.

- Each unit has a fixed maturity period. After that time, the investor returns the unit & get back his initial investment /money.

- Latest regarding Mutual Funds: A large number of Mutual Fund managers had invested money in bonds issued by IL&FS, which suffered a loss after the crisis. In fear, people stopped investing money in all Mutual Funds, hitting this sector very hard.

Types of Mutual Funds

It can be classified in many ways

1 . Portfolio Nature

| Equity Mutual Funds | Invest only in Equity |

| Debt Mutual Funds | Invest only in Debt instruments |

| Gilt Edged Mutual Funds | Invest only in Gilt Edged Bonds only ( and thus have very less return ) |

2. Income & Risk

| Growth Fund | Eg : Equity (80%) & Debt (20%) |

| Balanced Fund | Eg : Equity : Debt = 50:50 |

| Income Fund | Eg : Equity : Debt = 20:80 |

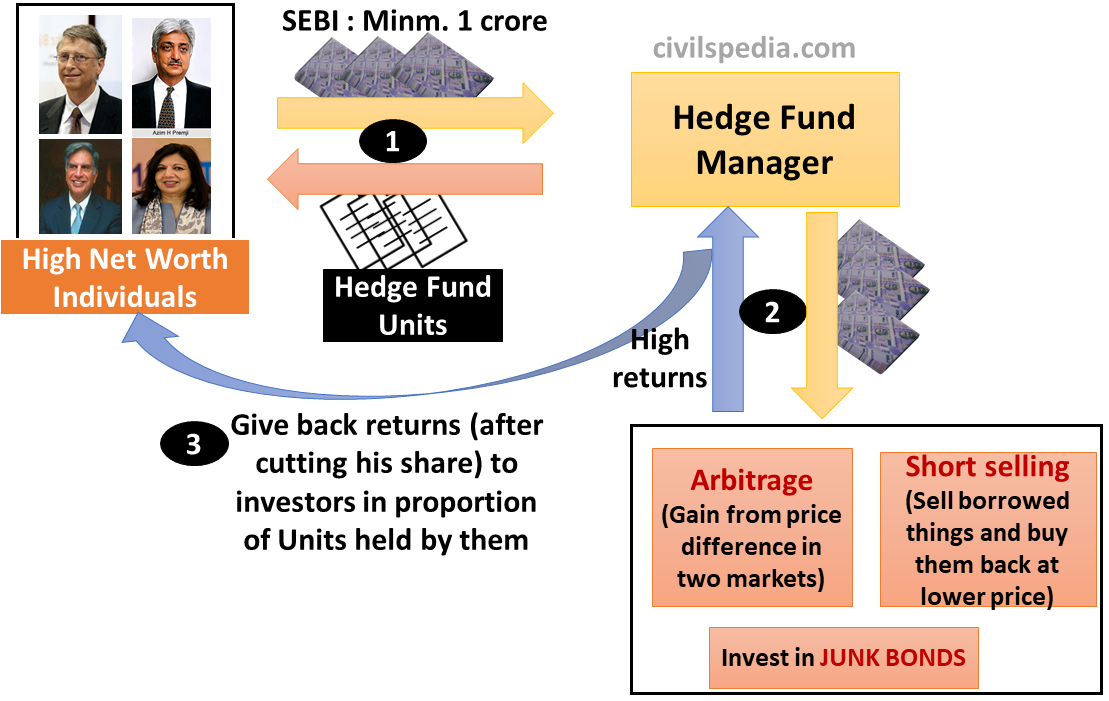

2. Hedge funds

- The hedge fund is open to a limited range of very high net worth individuals (HNI). In simple words, it is a private Mutual Fund for High Net-worth Individuals

- Their only aim is to get maximum return in the quickest time.

- Under this, HNI individuals give money to the Hedge Fund Manager in return for units with the promise of high returns. Hedge Fund Manager then play in the market to make money in different ways like investing in junk bonds, Arbitrage, Leverage, Short Selling etc.

- SEBI Regulations on hedge Funds

- Each member must be paying at least ₹1 crore.

- SEBI has placed strict norms on Hedge Funds.

- Examples of Hedge Funds Managers in India: Karvy Capital, Motilal Ostwald etc.

- Technically they are Alternate Investment Funds (AIF) Cat III.

Side Topic: Alternative Investment Funds

It is a technical classification under SEBI norms:

1. AIF Category I

- They generate positive spillover effects on the economy.

- E.g., Venture Capital Funds, Angel investors funds, SME Funds, social venture funds, infrastructure funds.

- SEBI norms are easy on them.

2. AIF Category II

- Neither in Cat-1 nor Cat-3. E.g. Private Equity or debt fund.

3. AIF Category III

- The AIF Category III funds indulge in excessively risky investments to generate high returns in a short time.

- E.g. Hedge Funds.

- SEBI norms are stricter; otherwise, they may destabilize the capital market.

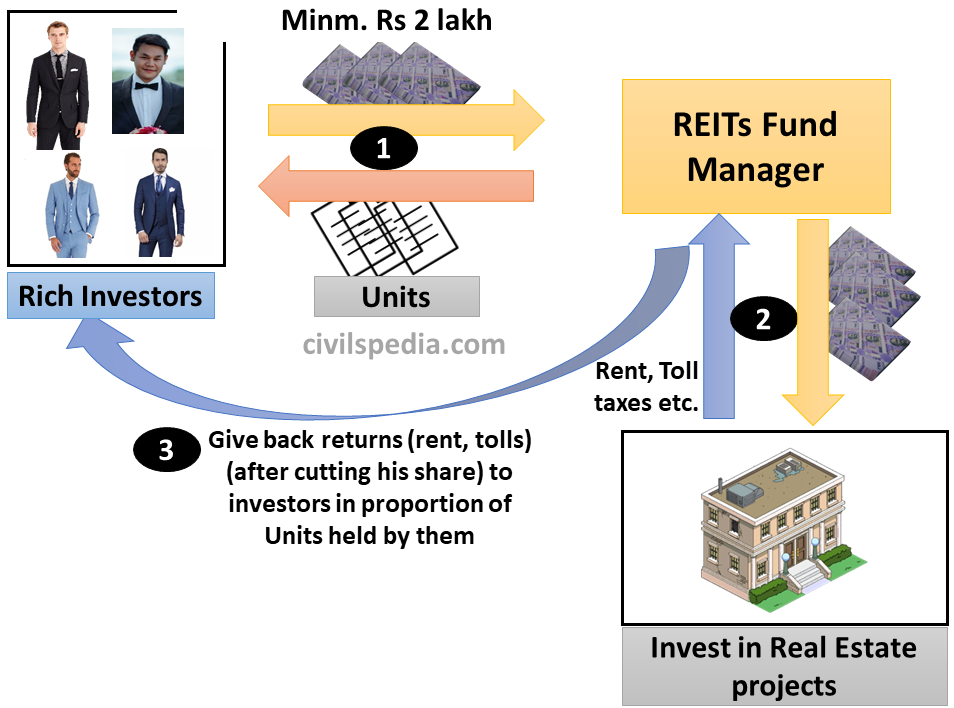

3. REITs: Real Estate Investment Trusts

- REITs are for High Net-worth Individual (HNI), and the Minimum Investment in REITs can be ₹ 2 lakh.

- SEBI regulates REIT Fund Managers.

- REIT Fund Managers give Units to investors and invest money in Real Estate Projects on the verge of completion but finding it difficult to raise loans from Banks or other NBFCs.

- When a real estate project completes and starts generating rent, they get their share of the rent from that which is paid to investors based on the proportion of units held by them.

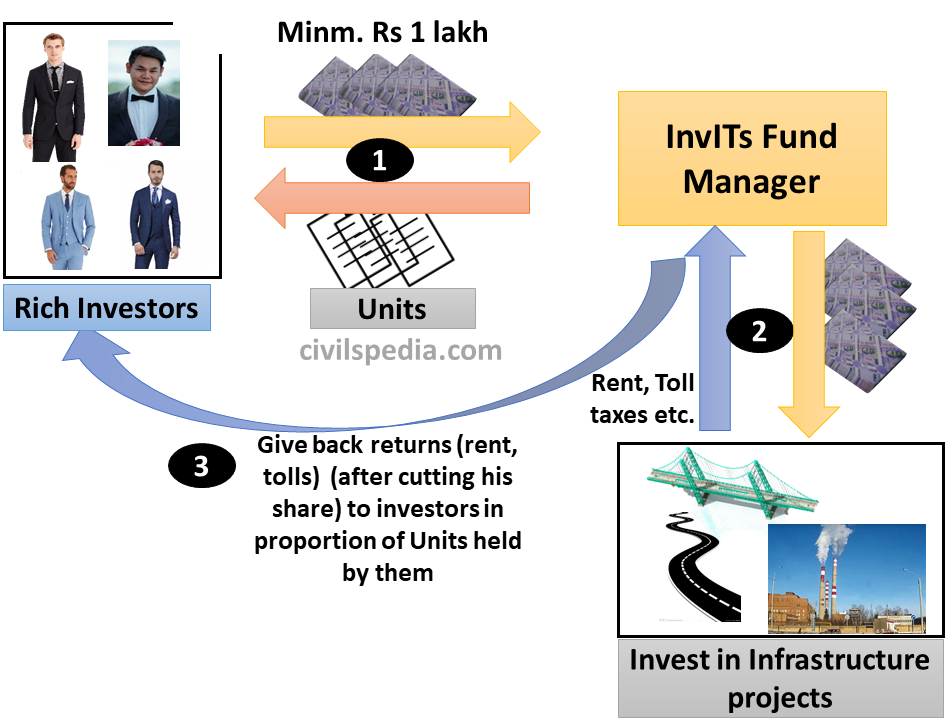

4. InvITs

- InvITs are Infrastructure Investment Trust.

- InvITs are the same as REITs, with the only difference being that they invest in Infrastructure Projects like airports, highways, ports, gas grids etc.

- RBI has allowed Banks to invest 10% of net owned funds in REITs & InvITs. Further, IRDAI has allowed insurers to invest in InvITs and REITs subject to the condition that they can’t invest more than 10% of their outstanding investment in single InvITs and REITs.

National Highways Authority of India (NHAI) launched its InvIT in FY22 to facilitate the monetization of roads and attract foreign and domestic institutional investors to invest in the roads sector.

Benefits of REITs & InvITs

- These instruments are successfully tried & tested in the US, UK, Australia, Japan etc.

- Stressed developers can get new finance and help complete projects facing financial crunch.

- It has the potential to help in saving banks from NPAs.

- REITs and InvITs provide new investment opportunities to people.

- They will help to channel household savings towards nation-building.

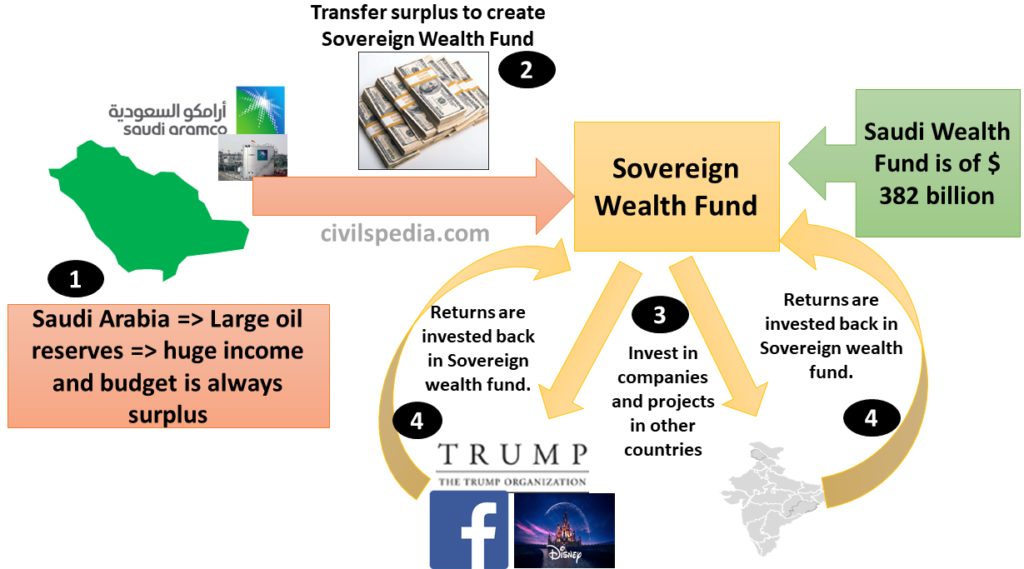

5. Sovereign Wealth Fund

- These funds are sovereign, i.e. under the direct control of the nation-state.

- Sovereign Wealth Funds are state-owned investment funds, wherein the country parks its surplus budget. This money is later used in making investments and earning more money in return.

- Examples: Abu Dhabi Investment Authority (ADIA) ‘s funds, Qatar Investment Authority (QIA), Saudi Arabia’s Public Investment Fund etc.

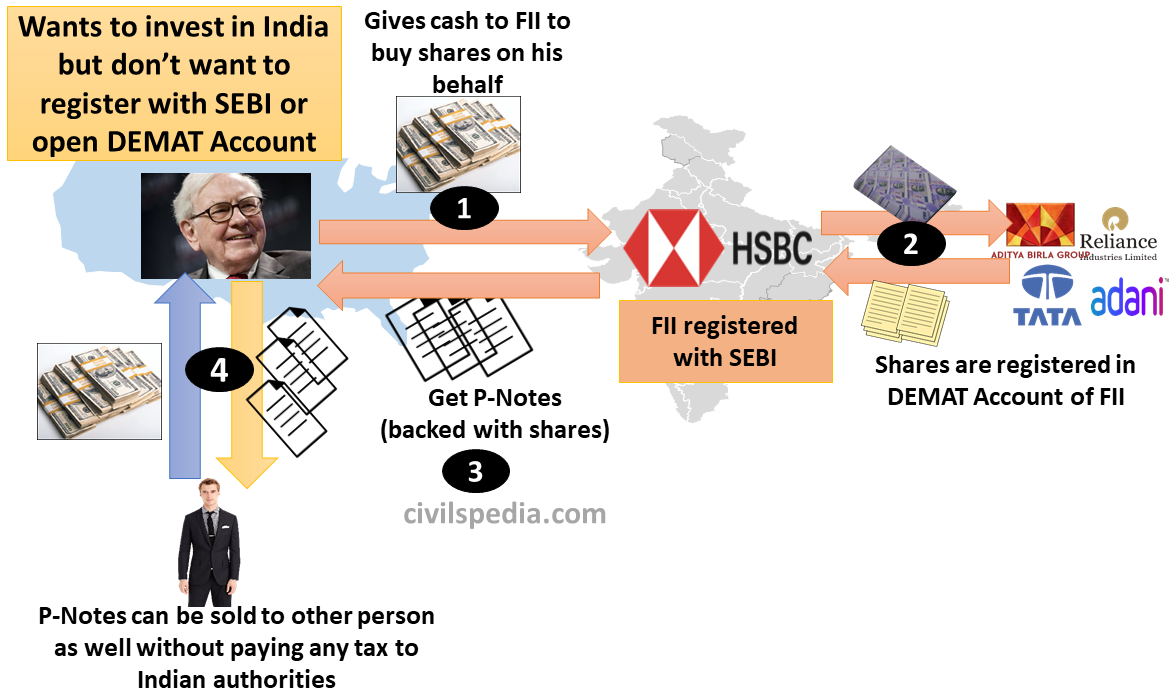

6. P-Notes / Participatory Notes

- Suppose a foreigner wishes to invest in India but does not want to go through the hassles of registering with SEBI, getting a PAN card number, opening a DEMAT account etc. So, he will approach SEBI registered foreign institutional investors (FII) such as Morgan Stanley, Citigroup or Goldman Sachs. He will pay them & instruct them to purchase particular shares and bonds on his behalf and store them in their Demat account. FII will give him P-Notes in return, and he will receive interest and dividends accordingly. He may also sell those P-notes to a third party. The P-Note holder also does not enjoy any voting rights in relation to security referenced by the P-Note.

- In simple terms, P-Notes are Offshore derivative Instruments that derive the value from the underlying Indian shares and bonds.

P-Notes are considered harmful to Indian economy because:

- P-note investors are not directly registered with SEBI; the identity of the actual investor and source of funds remain disguised. Hence, it may allow India’s ‘black money’ stashed away from India through ‘hawala’ to get invested back in the market. Again, ‘terrorist organizations’ might have been using this route, too.

- If the P-Note owner sells his P-Notes to another foreign investor, the Government of India will be deprived of taxes. (Compared to a scenario where an Indian shareowner sells his shares to another Indian investor, the government gets securities transaction tax and capital gains tax on his profit).

=> Therefore, SEBI is tightening the control over P-Notes.