This article deals with ‘Article 13 of the Indian Constitution – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Article 13

Article 13 declares that all the laws inconsistent with any Fundamental Rights shall be void.

And the LAW, according to Article 13, is

Permanent laws enacted by Parliament and State Legislatures

Temporary laws like ordinances

Statutory instruments like orders, rules, regulations and notifications

Non-legislative sources of law like customs or usage having the force of law

Although Constitutional Amendments aren’t law and can’t be challenged in the Supreme Court, the Keshavananda Bharti case pronounced that if the constitutional amendment violates the basic structure of the constitution, which includes Fundamental Rights, it can be challenged.

It has to be noted that ‘Judicial Review’ is conferred by Article 13.

Note: The pre-constitution laws are not declared invalid ab initio (from the start). They are invalid only when they are inconsistent with any of the fundamental rights.

Judicial Review

What is Judicial Review?

The term’ Judicial Review’ means the Power of a Court to review and potentially strike down an act of Legislature, Executive or Administration as unconstitutional if they are not in line with the provisions of the constitution.

The doctrine of Judicial Review has its origin in the USA in the Marbury v/s Madison case of 1803.

Judicial Review of Legislative Action in India

The Indian constitution provides for Judicial Review through Articles 13, 32, 131-136, 143, 226, and 246.

Judicial Review of Legislative Action is done using basic constitutional doctrines as listed below.

Doctrine of Basic Structure,

Doctrine of Pith and Substance: ‘Pith’ means ‘true nature’, and ‘Substance’ means ‘a most important part of something’. Hence, the Doctrine of Pith and Substance says that where the question arises of determining whether a particular law relates to a specific subject (mentioned in one List or another), the Court looks to the true nature and substance of the matter.

Doctrine of Colourable Legislation: It means that whatever legislature can’t do directly, it can’t do indirectly.

Doctrine of Severability: It means that when a part of the statute is declared unconstitutional, then the unconstitutional part is to be removed, and the remaining valid portion will continue to be valid

Doctrine of Liberal Interpretation: The provisions of the Constitution should be interpreted liberally and broadly instead of in a narrow sense.

Doctrine of Limitation of Stare Decisis: The Policy of the courts to stand by the precedent

Doctrine of Eclipse: If the act violates the Fundamental Rights of citizens, the Fundamental Rights overshadow the act, making the act unenforceable.

Doctrine of Prospective Over-Ruling: The Supreme Court can overrule its earlier judgment, but the impact will apply from the prospective effect and not retrospectively.

Doctrine of Harmonious Construction: Provisions of the Constitution shouldn’t be interpreted in isolation. Instead, it should be read together to ensure consistency and harmony, keeping in mind the intent of the Constitution makers.

Important Cases / Judicial History of Judicial Review of the Legislative Action

AK Gopalan v. State of Madras: TheConstitution is supreme, and every statute has to conform to the constitutional requirements.

Minerva Mills Case: The Judicial Review is the Basic Feature of the Indian Constitution.

Indira Gandhi v. Raj Narain (1975): Ordinary Laws aren’t subject to the Doctrine of Basic Structure, which is applied only to determine the validity of the Constitutional Amendment.

IR Coelho v. State of Tamil Nadu (2007): All Constitutional Amendments made on or after 24th April 1973 by which the Ninth Schedule is amended by inclusion of various laws therein shall have to be tested on the touchstone of Basic Features of the constitution enshrined in Article 14, 19 and 21.

Judicial Review of Administrative Action

In this case, the Court scrutinizes the entire Administrative Action and sees how it was reached. If the Court finds an Administrative Action arbitrary or irrational, it sets aside the entire action.

Delhi Development Authority v. UEE Electrical Engineering Private Limited (2004): The court held that irrationality and procedural impropriety are grounds for judicial review of administrative action.

Doctrine of Proportionality: If the Administrative Authority awards disproportionate punishment to the allegations, it remains open for judicial review.

This article deals with ‘Union Public Service Commission (UPSC)– Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Introduction

The Union Public Service Commission (UPSC) serves as the central recruiting agency in India and is responsible for conducting examinations and selecting candidates for various government posts.

The Constitution of India directly created this body, highlighting its significance and constitutional mandate.

The provisions related to the UPSC are outlined in Articles 315 to 323, which fall under Part XIV of the Indian Constitution.

Article 315 establishes the UPSC and outlines its composition, functions, and powers.

Articles 316 to 319 detail the appointment, removal, suspension, prohibition to hold office after ceasing to be member and term of office of members of the UPSC, ensuring their independence and impartiality.

Article 320 empowers the UPSC to conduct examinations for appointments to civil services and other positions, ensuring a merit-based selection process.

Article 321 provides for the power to extend the functions of Public Service Commission.

Articles 322 and 323 deal with the expenses and annual reports of the UPSC

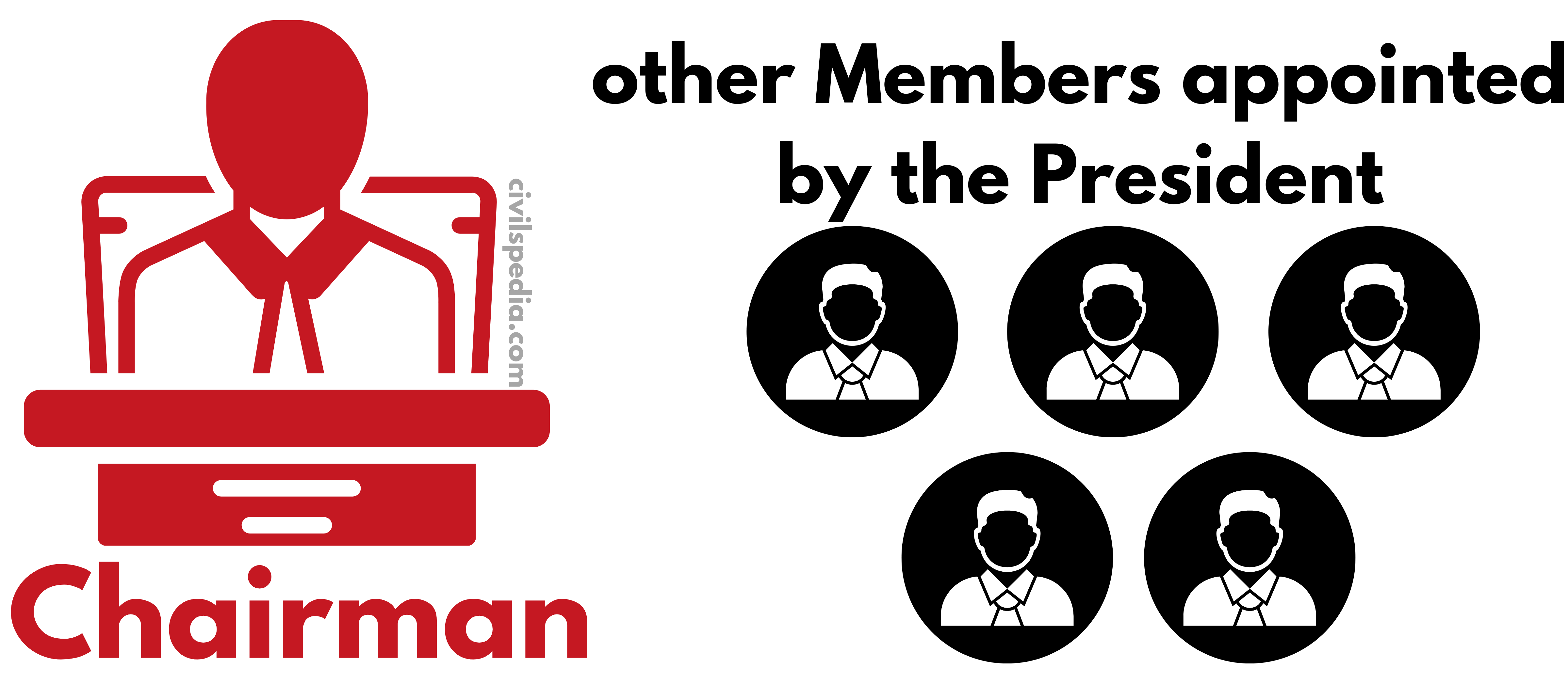

Composition

UPSC consists of a Chairman and other Members appointed by the President of India.

The Constitution hasn’t specified the strength of the Commission & left the matter to the discretion of the President.

No qualifications are prescribed except that one-half of the members of the Commission should be persons who have held office for at least ten years, either under the Government of India or the Government of a state.

The Constitution also authorizes the President to determine the conditions of service of the Chairman and other members.

Term of Chairman and Members

The

Chairman and members of the Commission hold office for

Term of 6 years or

Until they attain the age of 65 years

Whichever is earlier.

However, members of

the UPSC have the option to relinquish their positions at any time by

submitting their resignation to the President of India.

Removal of Chairman and Members

The President can remove the Chairman or Members of UPSC.

If he is adjudged insolvent (that is, has gone bankrupt)

If he engages in any paid employment outside of his office

Infirmity of mind or body

The President can also remove them due to misbehaviour. However, in this case, the President has to refer the matter to the Supreme Court for an enquiry and act according to the advice.

Independence

The manner of

removal of

members of the UPSC ensures their independence, as they can only be

removed on the grounds mentioned above, safeguarding their security of

tenure.

Conditions of service for UPSC members cannot be

altered to their disadvantage after their appointment, ensuring stability and

protection against arbitrary changes.

The

entire expenses of the UPSC are charged on the Consolidated Fund

of India,

ensuring financial autonomy.

The Chairman of UPSC (on ceasing to

hold office) is not eligible for further employment in the Government of

India or a state.

Member of

UPSC (on ceasing to hold office) is eligible for appointment as the

Chairman of UPSC or a State Public Service Commission (SPSC), but not for

any other employment in the Government of India or a state.

Neither the

Chairman nor a member of the UPSC is eligible for reappointment to that

office.

Functions

The

UPSC conducts examinations for appointments to the All-India

Services, Central Services, and Public Services of centrally administered

territories, ensuring merit-based selection.

It assists

the States in Joint Recruitment for any services for which candidates

possessing special qualifications are required.

It serves

the needs of a state at the request of the State Governor and with

the approval of the President of India.

It is consulted on

matters related to personnel management (like suitability of candidates,

promotions, transfers, extension of service etc. of civil servants).

The

jurisdiction of UPSC can be extended by an act made by the Parliament.

The UPSC annually presents a report on its

performance to the President. The President places this report before both

Houses of Parliament, along with a memorandum explaining the cases where the

advice of the Commission was not accepted and the reasons for such

non-acceptance.

Limitations

The following matters are kept outside the functional jurisdiction

of UPSC. In other words, the UPSC is not

consulted

While making reservations of appointments or posts in favour of any backward class of citizens.

While taking into consideration the claims of SCs & STs in making appointments

Posts of the highest diplomatic nature and a bulk of group C and D services.

With regard to the selection for temporary post (less than a year.)

The President holds

the authority to exempt certain posts, services, and issues from the

jurisdiction of the UPSC. However, any regulations established by the President

for this purpose must be presented before both Houses of Parliament for a

minimum of 14 days. Parliament retains the power to modify or revoke these

regulations as deemed necessary.

Role of UPSC

The Constitution visualises the UPSC to be the ‘watchdog of the merit system‘ in India, ensuring that recruitment to various civil services is based on merit and fairness.

UPSC’s responsibilities are specifically focused on the selection process. It does not involve itself in matters such as service conditions, cadre management, training, and other administrative aspects. These areas fall under the jurisdiction of the Department of Personnel and Training (DoPT).

The recommendations made by UPSC are advisory in nature and are not binding on the government. However, the government is answerable to Parliament if it chooses to deviate from UPSC’s recommendations.

The emergence of the Central Vigilance Commission (CVC) in 1964 affected the role of UPSC in disciplinary matters. This is because both are consulted by the government while taking disciplinary action against a civil servant. However, the UPSC, being an independent constitutional body, has an edge over the CVC, which is a statutory body.

This article deals with ‘Comptroller and Auditor General (CAG) – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Introduction

The Constitution of India (Article 149) provides for an independent office of CAG

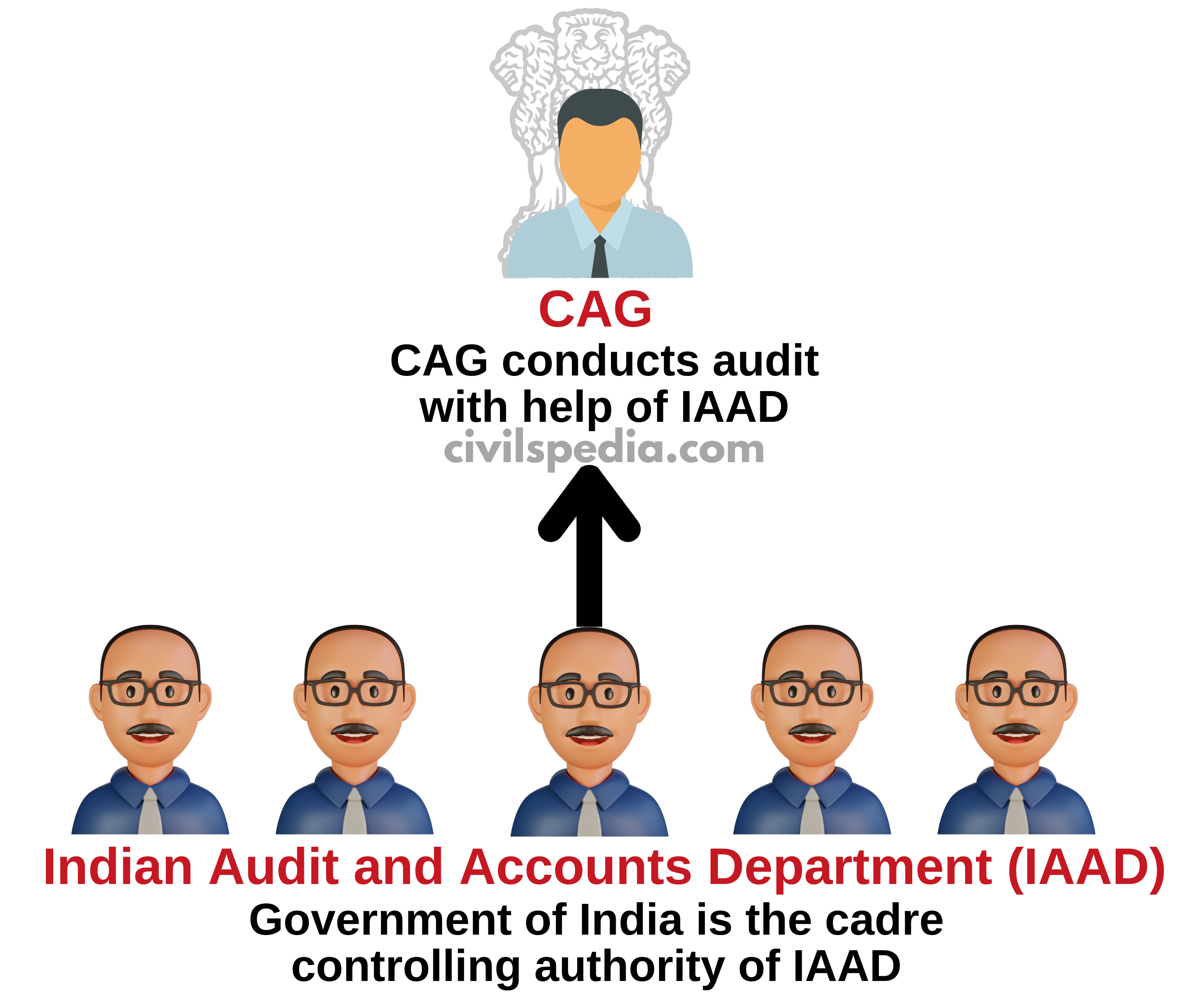

CAG is the head of the Indian Audit and Accounts Department

CAG is the guardian of the public purse at both levels—Centre and State.

Appointment and Term

CAG is appointed by the President of India by a warrant under his hand and seal.

CAG holds office for a period of six years or up to the age of 65 years, whichever is earlier.

He can also be removed by the President on the same grounds and in the same manner as a judge of the Supreme Court.

To ensure the Independence of Office

CAG is provided with the security of tenure. He can be removed by the President only in the same manner as the Judge of the Supreme Court. Thus, the CAG doesn’t hold his office till the pleasure of the President, although the President appoints CAG.

CAG is not eligible for further office under the Government of India or any state after he ceases to hold his office (controversy erupted when former CAG Vinod Rai was appointed as Head of Bank Board Bureau )

Neither his salary nor his rights regarding leave of absence, pension, or age of retirement can be altered to his disadvantage after his appointment.

Administrative expenses of the office of the CAG are charged upon the Consolidated Fund of India.

System of Auditing in India

Articles 148 to 151 of the Indian Constitution institutionalized the Auditing Mechanism and office of CAG. But this system is a continuance of British rule. The same Auditing System is continuing in India.

The Comptroller and Auditor General (CAG) of India is a constitutional authority responsible for auditing. CAG operates independently of the Government and reports directly to the Parliament or State Legislatures, thereby ensuring impartiality and objectivity in its auditing processes.

The Indian Audit and Accounts Department (IA&AD) is the primary body through which CAG conducts audits.

Issue with the System

CAG (IAAD) conducts Audit on behalf of Parliament. Principally, it should be entirely out of the influence of the Executive. However, the Government of India is the Cadre controlling Authority of the Indian Audit and Accounts Department (IAAD), which is headed by CAG and with whose help CAG conducts audits. This is a continuance of the British Era Model (1937 rules) in which the Executive indirectly controlled CAG.

Duties and Powers of the CAG

Article 149

Constitution (Article 149)

authorises the Parliament to prescribe the duties and powers of the

CAG. Accordingly, Parliament enacted CAG’s

(Duties, Powers and Conditions of Service) Act, 1971. The Act was

amended in 1976 to separate accounts from audits in the Central government.

The duties and functions of the CAG

CAG audits the accounts related to all expenditures from

Consolidated Fund of the Union of India and each state

Contingency Fund of the Union of India and each state

Public Account of the Union of India and each state

CAG audits the balance sheets of the departments of the Central Government and state governments.

CAG can audit the accounts of any other authority when requested by the President or Governor. For example, audit of local bodies

Earlier,

CAG used to compile and maintain accounts of the Central Government as

well. In 1976, he was

relieved of his responsibility to compile and maintain accounts of the Central

Government due to the separation of accounts from Audit.

Article 150

CAG advises the President with regard to the prescription of the form in which the accounts of the Centre and states shall be kept.

Article 151

CAG submits the audit reports related to the accounts of the Centre to the President, who shall, in turn, place them before both Houses of Parliament

He acts as a guide, friend and philosopher of the Public Accounts Committee of the Parliament.

Role of CAG

The role of the CAG is to

uphold the Constitution of India and the laws of Parliament in the field

of financial administration. The audit reports of the CAG secure

accountability in the sphere of financial administration of the

executive.

CAG is an agent of the

Parliament and conducts an Audit of expenditure on behalf of the

Parliament. In

addition to legal and regulatory Audit, CAG can also conduct the propriety

audit; that is,

he can look into the ‘wisdom, faithfulness and economy’ of expenditure and

comment on the wastefulness and extravagance of such expenditure. However,

legal and regulatory Audits are obligatory, but propriety audit is

discretionary (but CAG can’t audit Secret service expenditure).

The Constitution of India

visualises the CAG as the Comptroller as well as the Auditor General.

However, in practice, the CAG is fulfilling the role of an

Auditor-General only and not that of a Comptroller, as the CAG has no control

over the issue of money from the Consolidated Fund and is concerned only

at the audit stage when the expenditure has already taken place (unlike

Britain)

Problems with CAG

Paralysing Unwillingness to Act: The Comptroller and Auditor General’s (CAG) presence in India is often cited as a primary cause of bureaucratic inertia. Officials fear making decisions due to the scrutiny they may face from the CAG, leading to indecision and stagnation in governance processes.

Post-Mortem Examination: CAG audits often serve as post-mortem examinations of government expenditures. CAG is concerned only at the audit stage when the expenditure has already taken place

Appointment of Generalists: The practice of appointing generalist bureaucrats, such as those from the Indian Administrative Service (IAS), as the CAG is criticized. Many argue that specialists from services like the Indian Audit and Account Service, Indian Economic Service, Indian Statistical Service, or Indian Revenue Service would be better suited for the role due to their expertise in auditing and financial matters.

CAG & Defence: CAG reports have sometimes been accused of jeopardizing national security, as seen in instances where revelations about defence preparedness were made public. For example, a CAG report in 2017 warned that the Indian Army’s ammunition stock would be depleted within 10 days of the war, potentially compromising the country’s defence capabilities.

Issue of Notional Loss: The CAG’s estimation of notional losses, such as in the 2G spectrum case, has been a subject of controversy. These estimates, which are based on assumptions and methodologies that may not always align with legal standards, can lead to inflated figures and subsequent legal challenges.

CAG Activism: Some critics perceive the CAG’s involvement in high-profile cases like the 2G spectrum and Coalgate as examples of activism beyond its mandate. While the CAG’s role is primarily to audit government expenditures and ensure accountability, its involvement in such cases has been seen as overstepping boundaries and encroaching into policy and regulatory domains.

Much of the government expenditure is kept out of CAG Audit by Governments.

CAG’s Authority doesn’t extend to Government Corporations created with special laws. Parliament or State Legislature can make provisions regarding Audit within the Act itself. Additionally, new organizational structures in the form of public-private partnerships are also out of the scope of CAG’s Audit. E.g., GMR Airport

NGOs and Private Agencies take up many Government works at delivery points. These private agencies and NGOs are also out of the ambit of CAG.

Issue of Redactment: CAG, in the Audit Report of Acquisition of Rafale, redacted, i.e. removed sensitive information from the document citing security concerns expressed by the Government.

Politicization of CAG’s office: The politicization of the Comptroller and Auditor General (CAG) post in India has become a subject of concern in recent years. The Constitution of India explicitly states that the CAG should not be given a post-retirement posting, emphasizing the need for the CAG to maintain impartiality and independence from political influence. However, there have been instances where former CAGs have been appointed to positions that raise questions about their independence and neutrality. For example

Former CAG Vinod Rai (who unearthed the Coal Scam) was appointed as Chairman of the Bank Board Bureau.

TN Chaturvedi (CAG from 1984 to 89) joined the BJP after retirement and contested the election using BJP’s ticket. He was later made Governor of Kerala too.

Appleby’s Criticism

Paul H. Appleby was highly critical of the role of the Comptroller and Auditor General (CAG) in India, going as far as recommending its abolition.

He argued that the institution of the CAG was inherited from colonial rule, implying it may not be suitable for modern governance needs.

Appleby criticized the CAG for fostering a paralysing unwillingness to act within government circles, suggesting that its oversight role may stifle decision-making and action.

He questioned the competence of auditors to understand the nuances of good administration, asserting that their expertise lies in auditing rather than administration.

Side Topic: Presumptive Loss / 2G Spectrum Case

The theory of presumptive and notional loss involves calculations by the CAG to estimate the potential revenue lost by the Government due to irregularities or lack of adherence to proper procedures in resource allocations, such as natural resources like spectrum and coal.

Using the Theory of Presumptive and Notional Loss

In the case of the 2G Spectrum

Allocation, the CAG calculated a notional loss of Rs 1.76 lakh crore due

to the use of a “first come, first served” policy instead of an

auction, which could have potentially generated higher revenue.

In the Coal Scam, the CAG

initially estimated a notional loss of ₹10 lakh crore, later revised to Rs

1.86 lakh crore, highlighting discrepancies in the allocation process.

However, in December 2017, a Special CBI Court acquitted A Raja and Kanimozhi and rejected the presumptive loss theory proposed by the CAG.

It’s also important to recognize that the Government’s objectives extend beyond profit maximization; considerations such as socio-economic factors and job creation also play a significant role in decision-making.

Hence,

CAG has failed to accommodate the changing

dynamics of doing business in the LPG Era

This article deals with ‘Inter-State River Water Disputes – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus. For more articles , you can click here

Constitutional Provisions

Status of Water in the Constitution

State List

Entry 17: Water, that is to

say, water supplies,

irrigation & canals, etc., subject to provisions of Entry 56

of List 1

Union List

Entry 56:Regulation and Development of

Inter-State Rivers & River Valleys

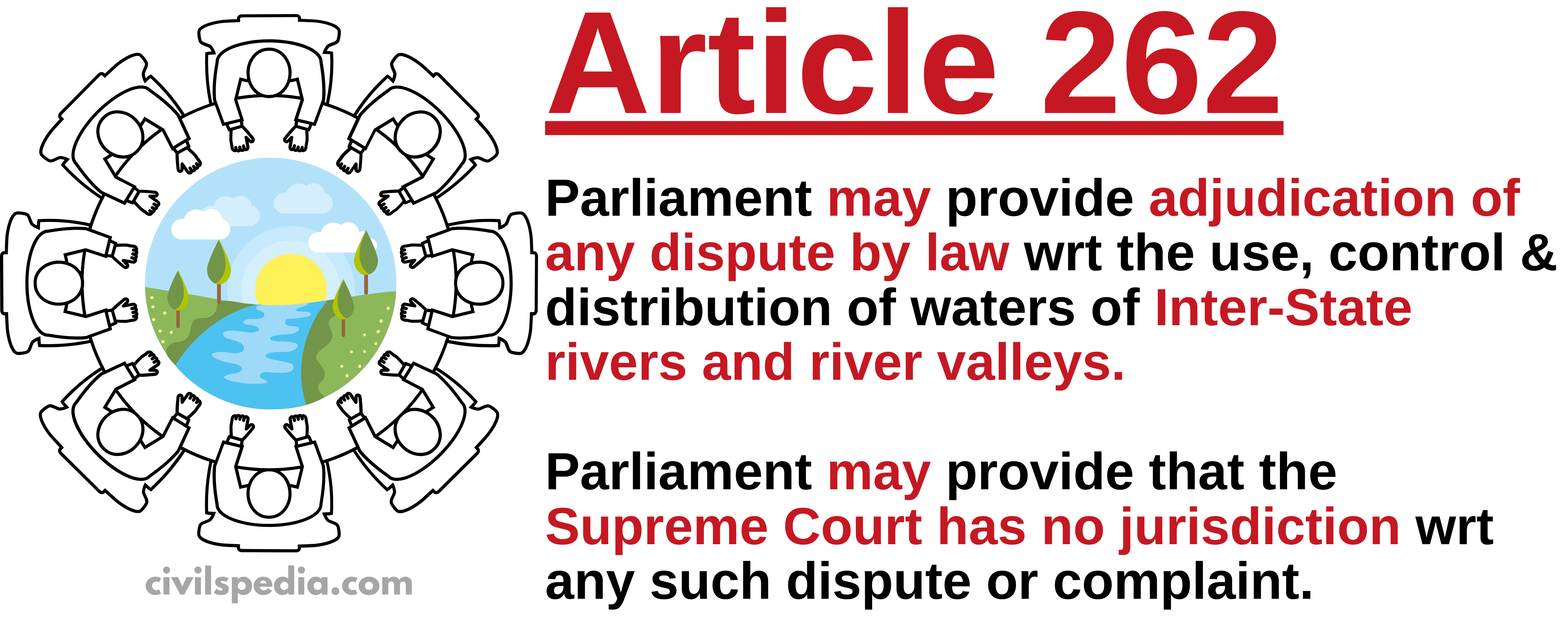

When a water dispute arises between two states, Article 262 is invoked & in pursuance of Article 262, two Acts were passed by the Parliament.

River Boards Act,1956

The Act

is designed to regulate and facilitate the development of inter-state rivers to

ensure effective water resource management. The key features of the River

Boards Act 1956 are

Establishment of River Boards: These boards are instrumental in coordinating efforts to regulate and develop rivers that flow through multiple states.

Board Establishment on State Government Request: River Boards are not unilaterally imposed but are established based on requests from State Governments.

Inter-State River Water Disputes Act,1956

The

Inter-State River Water Disputes Act of 1956 provides a mechanism for resolving

disputes related to the sharing of river waters between different states in

India.

Initiation of Tribunal: If a Riparian State believes that its interests are adversely affected by the actions or plans of another state, it can request the government of India to establish a Tribunal to address the dispute.

Timeline for Tribunal Setup: The government of India is mandated to set up the Tribunal within one year of receiving such a request.

Composition of Tribunal: The Tribunal comprises three members, each of whom must be a Judge of either the Supreme Court or a High Court.

Final and Binding Decision: The decision rendered by the Tribunal holds ultimate authority and is deemed final and binding. The Supreme Court or any other court don’t have any jurisdiction in this regard.

A total

(9) such tribunals have been established

till date. Important ones are

Ravi & Beas: Involving Punjab and Haryana, formed in 1986 and still pending the award.

Kaveri: Involving Karnataka, Tamil Nadu, Kerala & Pondicherry, with time period 1990-2007

Mahanadi: The most recent tribunal, formed in 2018, involving the states of Odisha and Chhattisgarh.

Causes of these Disputes

Agriculture

and Water Scarcity: Riparian

states depend on river water for agriculture. Such issues intensify during

low rainfall seasons. Examples include disputes over the Kaveri, Krishna,

Ravi, and Beas rivers, primarily revolving around sharing water for

agricultural purposes.

Multipurpose

Projects and Dams: Conflicts often arise between upstream and downstream

states regarding multipurpose projects and dams. The Mahanadi issue serves

as an illustration of such disputes.

River

Joining: It

is usually done to divert river water from sufficient to deficient river

basins, but many issues arise, such as environmental assessment,

submergence of surrounding lands, etc. Mahadayi/ Mandovi (Goa vs

Karnataka) is an example of such a dispute.

Unborn States

Share: Disputes

arise when a tribunal’s judgment on a contested river involves states that

later undergo division or creation. The Krishna water tribunal is an

example where the parties were Andhra Pradesh, Maharashtra, and

Karnataka. But as the new state Telangana has come into being, it

approached the Supreme Court for its right to get a proper share.

Why Tribunals for Inter-State Water Disputes?

Article 262 of the Constitution lays down that the Parliament may by law provide for the adjudication of any dispute with respect to any Inter-State River (ISR). Accordingly, the Parliament enacted the Inter-State River Water Dispute Act 1956, which provides for the reference of such a dispute to a Water Tribunal. The said Act bars the Supreme Court or any other Court from exercising jurisdiction in respect of any water dispute.

The main reasons for keeping River Disputes out of the

purview of the court’s jurisdiction were that (the whole of the

Constituent Assembly agreed that there is a need for Tribunals to settle

Inter-State River Disputes (but there wasn’t unanimity on Permanent Tribunal or

Temporary Tribunals)) :

Speedy Disposal: The Act

ensures the swift resolution of Inter-State River water disputes by making

the tribunal’s decision final and binding, thereby avoiding prolonged

legal processes.

Technical and Scientific Expertise: Since the

resolution of Inter-State River disputes hinges upon heaps of technical

and scientific data, the resolution of such disputes by specialized

tribunals would allow for a better appreciation of such data.

Flexible and Informal Proceedings: Unlike

courts bound by strict legal procedures, tribunal proceedings are

relatively informal. This flexibility allows for deliberative

decision-making and discretionary measures, fostering the potential for

mutually negotiated settlements.

In this

context, it can be argued that the rationale behind excluding the jurisdiction

of courts was fairly well-intentioned.

Main Problems with Present System and Remedies

The

problem lies elsewhere and has been well documented by many commissions,

including the Sarkaria Commission. These include:

Long delays & uncertain time frame: The existing system is plagued by prolonged delays, leading to uncertainty. For example, in the Ravi Beas case, referred to the Tribunal in 1986, the matter is still pending.

Issue of finality: The Tribunal acts as the arbiter for water disputes between states. Although courts are barred from interfering, matters are still taken to courts through Special Leave Petitions. E.g., the Cauvery Case, where the matter was brought to courts through Special Leave Petitions.

Enforcement Issues: Inadequate provisions for enforcing Tribunal awards lead to challenges in implementation. There is political resistance and reluctance from states to comply with Tribunal awards due to political considerations.

Politicization of Water Issues: Even after the award is announced, in times of coalition politics, sometimes the centre doesn’t publish it in the gazette.

Suggestions to improve this

Institutional Changes: Utilize the

Inter-State Council as a platform for resolving water conflicts

effectively.

Permanent Tribunal: Advocate the establishment of

a Permanent Tribunal, a concept supported by Ambedkar during

Constitutional Assembly Debates.

Mediation Approach: Reform the current adversarial

judicial process to mediation for a mutually acceptable resolution.

Mediation has solved a large number of River Disputes, even at the

international level. For example,

World Bank played the role of

mediator between India and Pakistan in the Indus Treaty.

The Vatican became a mediator

in solving the Zambezi River dispute involving eleven countries.

Declaring Rivers National Property: The

establishment of separate corporations on the pattern of the Damodar

Valley Corporation may be immensely useful in this direction.

Bringing Water to Concurrent List: As

suggested bythe Ashok Chawla Committee, water resources

should be included in the concurrent list for better coordination and

management.

Proposed Changes in Inter State River Water Disputes Act

The following changes have been proposed in the Inter-State River Water Disputes Act of 1956 to resolve the deficiencies the present mechanism faces.

Single Permanent Tribunal

Establish a single, Permanent

Tribunal for adjudicating all inter-state river water disputes.

Awards will be notified

automatically.

Composition

of the Tribunal: Chairperson, Vice-Chairperson, and not more than six other Members

Members from both judicial (3)

and technical backgrounds (3).

Even in Constituent Assembly

debates, the setting of the Permanent Tribunal to resolve Inter-State

River Water Disputes was greatly favoured, and BR Ambedkar

was in favour of the Permanent Commission. The act favouring the Temporary Commission

was favoured on the basis of experience that such issues would not come

up. This is not the case now, and such disputes are rising very

frequently.

Dispute Resolution Committee (DRC)

DRC will handle

disputes prior to the tribunal, with a resolution timeline of one year.

Most disputes will get

resolved at the DRC’s level itself. But if the state is not satisfied, it

can approach the tribunal.

Data Agency

Establish an agency to collect

and maintain updated water data in each river basin in the country.

The collected data will aid in

the timely resolution of water disputes

Timeline

The Tribunal must give a

decision within two years, with a possible extension of one more year.

The decision of the Tribunal

shall be final and binding.

Case Study: Cauvery Issue

1924

The agreement was signed

between Madras Presidency and Mysore to build a dam in Mysore. The

agreement was valid for 50 years, and it led to the

construction of the Krishnaraja Sagar Dam.

Note: The agreement was

heavily in favour of the Madras Presidency. Mysore was allowed to

construct just one dam.

1960s

Karnataka wanted to

make more dams on Cauvery, but Tamil Nadu didn’t allow it on the basis of the

1924 Agreement.

1974

The Water Sharing

Agreement lapsed after 50 years. Karnataka decided to go ahead with making

dams. 4 dams were made by Karnataka in quick succession.

1986

Tamil Nadu

approached the Centre for setting up a Tribunal

2 June

1990

The Cauvery Water

Dispute Tribunal (CWDT), headed by Justice Chittosh Mookerjee, was set after

the Supreme Court’s direction.

2007

CWDT issued its

final order, allocating water shares (in tmcft):

– Tamil Nadu: 419

– Karnataka: 270 (Karnataka claimed 312,

but CWDT considered earlier agreements)

– Kerala: 30

– Puducherry: 7

Karnataka and Tamil

Nadu contested the order in the Supreme Court via Special Leave Petitions

(SLPs).

It also recommended

the establishment of a Cauvery Management Board. But

it was just a recommendation.

2013

2013

was a drought year. Tamil Nadu moves Supreme Court seeking directions to

Water Ministry for Constitution of Cauvery

Management Board as Karnataka wasn’t following orders of CWDT.

2016

The year 2016 was a

drought year, with Karnataka not releasing adequate water. Tamil Nadu went to

the Supreme Court again. SC ordered the formation of the Cauvery Water

Management Board.

Point to Note – The

main issue in this case (& other River Disputes, too) is a shortage of

water. Whenever there are drought-like conditions, states start to fight over

the division of Rivers.

This article deals with ‘Financial Relations between Centre and States – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus. For more articles , you can click here

Introduction

Articles 268 to 293 in Part XII of the Indian constitution deal with financial relations.

Allocation of Taxing Powers

The

division of taxing powers is as follows

Parliament

Parliament can levy taxes on subjects in the Union List (13 items).

State Legislature

State Legislatures can levy taxes on subjects enumerated in the State List (18 items)

Both

– Both Parliament and State Legislatures can levy taxes on subjects enumerated in the Concurrent List. – Initially, the Concurrent List had no tax entries, but the 101st Amendment Act of 2016 introduced a special provision for GST. Parliament and State Legislatures now have concurrent power to make laws related to GST.

Residuary

The residual power of taxation is vested in the Parliament.

There is a difference between the power to levy taxes, collect taxes & appropriate the proceeds of taxes. For example, the income tax is levied and collected by the Centre, but its proceeds are distributed between the Centre and the states.

The Indian Constitution has placed various restrictions on the state’s taxing powers. These are as follows:-

Tax on Professions, Trades, Callings, and Employments: State legislatures can levy taxes on professions, trades, callings, and employments, but there’s a cap of ₹2,500 per year on the total amount imposed on any individual.

Prohibition on Taxing Goods and Services: State legislatures cannot impose tax on goods or services in two instances: (1) when the transaction happens outside the state and (2) when it occurs in the course of import or export.

Tax on Consumption or Sale of Electricity: States have the authority to levy taxes on the consumption or sale of electricity.

No tax can be imposed on electricity consumed or sold to the Centre

No tax can be imposed on electricity utilised in the construction, maintenance, or operation of railways

Tax on Water or Electricity by Interstate Authorities: State legislatures can levy taxes on water or electricity generated, consumed, sold or distributed by authorities established by Parliament for regulating or developing interstate rivers or river valleys.

Distribution of Tax Revenues

Major changes in the scheme to distribute tax revenue between the

Centre and the States were introduced by the 80th and 101st Constitutional

Amendments.

80th Constitutional Amendment, 2000 (Alternative Scheme of Devolution)

The 80th Amendment was passed to implement the 10th Finance Commission’s suggestion of allocating 29% of specific central taxes and duties to the states.

It was retroactively applied from April 1, 1996, and brought various central taxes, including corporation taxes and customs duties, in line with income tax regarding their constitutional sharing with the states.

101st Constitutional Amendment

The 101st Amendment enables the implementation of a new tax system, Goods and Services Tax (GST), in the country. It grants both the Parliament and State Legislatures the authority to enact laws for imposing GST on transactions involving the supply of goods or services.

The proceeds of GST are divided between the Center and the state on the recommendation of the GST Council.

The present situation regarding tax distribution between the Centre and states is as follows

Article 268 (Taxes levied by the Centre but collected and appropriated by States): It includes stamp duties on cheques, bills of exchange, promissory notes, insurance policies, transfer of shares, and similar transactions.

Article 269 (Taxes levied and collected by Centre but assigned to States): There are two categories of taxes under this category

Taxes on interstate sale or purchase of goods (excluding newspapers)

Taxes on the consignment of goods in interstate trade.

Article 269-A (Levying and Collecting of GST in the Course of Inter-State Trade): The responsibility for levying and collecting this tax rests with the Centre. However, the distribution of this tax between the Centre and the States is determined by Parliament based on the recommendations of the GST Council.

Article 270 (Taxes Levied and Collected by the Centre but Distributed between the Centre and the States): This category includes all taxes and duties listed in the Union List, excluding those mentioned in Articles 268, 269, and 269-A, surcharge on taxes in Article 271, and specific-purpose cess. Based on the Finance Commission’s recommendation, the President determines the distribution of the net proceeds of these taxes and duties.

Article 271 (Surcharges for the purpose of the Centre): The Parliament has the authority to impose surcharges on certain taxes and duties mentioned in Articles 269 and 270. The funds generated from these surcharges are allocated exclusively to the Centre. However, the Goods and Services Tax (GST) is exempted from such surcharges.

Taxes Levied, Collected, & Retained by the States: These include taxes enumerated in the state list (18 in number).

Distribution of Non-tax Revenues

a. The Centre

The

primary contributors to the non-tax revenues of the Centre are the following.

b. The States

The

primary contributors to the non-tax revenues of the States are the following.

Grants-in-Aid to the States

The

Centre can give money to States via Grants in Aid. These are of two types

1 . Statutory Grants

General Provision: Under Article 275, Parliament can give money to states which need financial assistance on the recommendation of the Finance Commission. They are charged on the Consolidated Fund of India.

Specific Provision: The Constitution has provisions for specific grants aimed at enhancing the well-being of scheduled tribes within a state or improving the administrative standards of scheduled areas in a state, including the State of Assam.

2. Discretionary Grants

Under Article 282, the states & centre can make grants even if it is not in their Legislative competence. For example, the Central Funds given on the advice of the Planning Commission.

They are discretionary because the centre is under no obligation.

These grants serve a dual purpose: firstly, to assist the state in meeting its financial obligations for achieving plan targets, and secondly, to provide the Centre with a means to influence and coordinate state activities in line with the national plan.

3. Other Grants

These grants, stipulated by the Constitution, were temporary in nature.

For the initial 10 years following the commencement of the Indian Constitution, a provision of grant was made in lieu of export duties on Jute products to states of Assam, Bihar & Orissa & were charged on Consolidated Fund.

GST Council

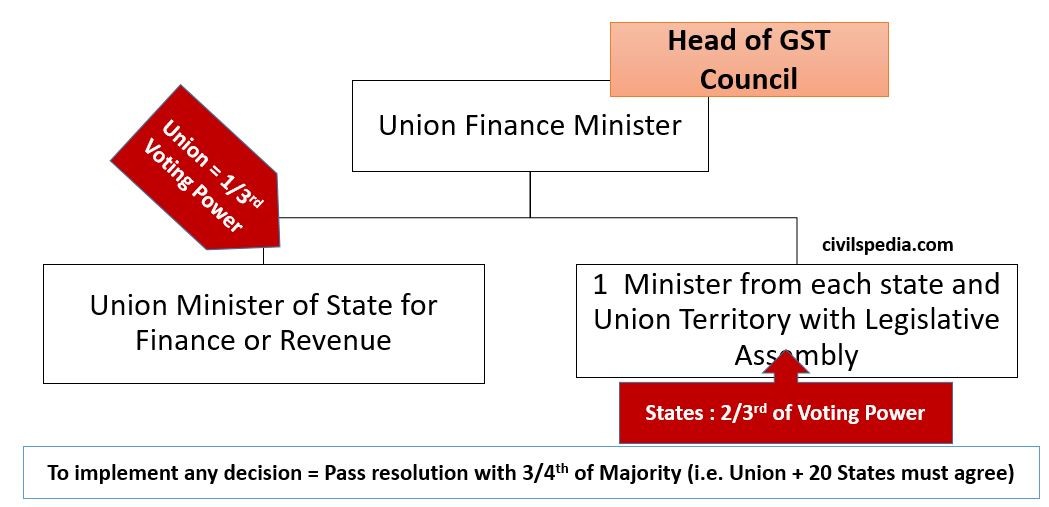

GST Council is a Constitutional Body made under the provisions of Article 279-A.

Membership of GST Council

Its membership is as follows

Headed by Union Finance Minister

Union Minister of State of Finance / Revenue

1 Minister from each State and Union Territory with the Legislative Assembly

Weighted Voting Powers: 1/3rd of Voting Power is with the Union and 2/3rd with States.

In order to implement any decision, at least a three-fourths majority is necessary, which translates into votes of the Union and a minimum concurrence of 20 states.

Functions of GST Council

Determine the inclusion of Union and State Taxes, Cess, and Surcharge under the GST regime.

Establish standard rates for CGST, SGST, and UTGST within the GST framework.

Set the effective date for including Crude Oil, Petrol, Diesel, Aviation Turbine Fuel, and LPG under the GST regime, until which the Union and individual States will unilaterally determine Excise and State VAT on these hydrocarbons.

Define the categories of ‘Exempted Goods and Services’ under GST.

Determine ‘Special Rates’ applicable during calamities, exemplified by the GST Council allowing Kerala in January 2019 to impose a 1% Calamity Cess on Intra-State trade for the subsequent two years for the rehabilitation of flood victims from 2018.

Address dispute settlements within this system involving conflicts between states or between a state and the Union.

Finance Commission

Article 280 establishes the Finance Commission as a quasi-judicial entity.

The President forms the Finance Commission every five years, or sooner if necessary.

The Finance Commission is required to make recommendations to

the President of India on the following matters:

Distribution of the divisible pool of taxes between the Centre and states (Vertical Distribution) and among states (Horizontal Distribution).

It provides recommendations on the principles guiding grants-in-aid from the Centre to the states.

The Finance Commission suggests measures to enhance a state’s consolidated fund for supporting Panchayats and municipalities.

It can address any other finance-related matter referred to it by the President.

The Constitution permits the Finance Commission to make broader

recommendations in the interest of sound finance.

Protection of State’s Interests

To

protect the interest of States, certain bills can be introduced in Parliament only on the recommendation of the

President

Bill which imposes or varies any Tax in which states are interested

Bill, which varies the meaning of the expression Agriculture income

Bill, which affects the principle on which money is distributed to state

Bill which imposes any surcharge on any specified tax or duty for the purpose of the centre.

Borrowing and Loans by Centre & States

Borrowing

Centre can borrow either within India or outside upon security of the Consolidated Fund of India within the limit fixed by Parliament (no limit fixed yet)

State Government can borrow within India (& NOT ABROAD) upon security of the Consolidated Fund of State

Loans

The central government can make loans to any state or give guarantees regarding loans.

The state can’t raise a loan without the consent of the centre if any part of a loan made by the centre to the State or in which the centre has guaranteed is still outstanding.

Effects of Emergencies on Financial Relations

National Emergency

During a National Emergency, the President can modify the Constitutional distribution of revenues between the Centre & and the State.

Modification continues until the end of the financial year when emergencies cease to operate.

Financial Emergency

During

Financial Emergency, the centre can give direction to states

Observe specified canons of financial propriety

Reduce the salaries & allowances of all classes of persons in states

Reserve money bills & financial bills for consideration by the President.

Inter-Government Tax Immunities

There

are certain rules of IMMUNITY FROM MUTUAL

TAXATION

Property of the centre is exempted from all taxes imposed by the state or any authority within the state like Panchayat, Municipal Corporation, etc.

Property & income of the state is exempted from central taxation.

Property & income of local bodies like panchayat are not exempted from central taxation.

Analysis: Centre-State Financial Issues

Vertical Imbalance in Resource Sharing: The States feel that the resource transfers to them haven’t been commensurate with their growing responsibilities.

Growing Central Expenditure on Functions in the State List: The 12th Finance Commission estimated that a fifth of the expenditure incurred by the Centre was on subjects that were in the domain of the States.

Compliance and Enforcement Cost of Central Legislation: There are several Central legislations, the compliance and enforcement costs of which are entirely borne by the States. At present, States are not compensated for the cost of compliance and the revenue loss on account of compliance.

Impact of Pay Revision by the Central Government on State Finances: The periodic pay revision by the Central Government gives rise to demand on the part of State government employees for a similar pay hike. States have demanded that the Central government should bear at least 50 % of the increase.

Sharing of Offshore Royalty and Sale Proceeds of Spectrum: Under the present Constitutional arrangements, offshore royalty accrues entirely to the Centre.

Profession Tax: it can not exceed Rs. 2,500 per annum. As income and salary levels are increasing, a limit on the professional tax constraints revenue mobilization

FRBM Legislation: The deficit reduction targets are uniform across all States. This ‘one-size-fits-all’ approach has constrained fiscally strong States to raise more resources.

Article 12 – ‘State’ for the purpose of Constitution

This article deals with ‘Article 12 – ‘State’ for the purpose of Constitution – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Article 12

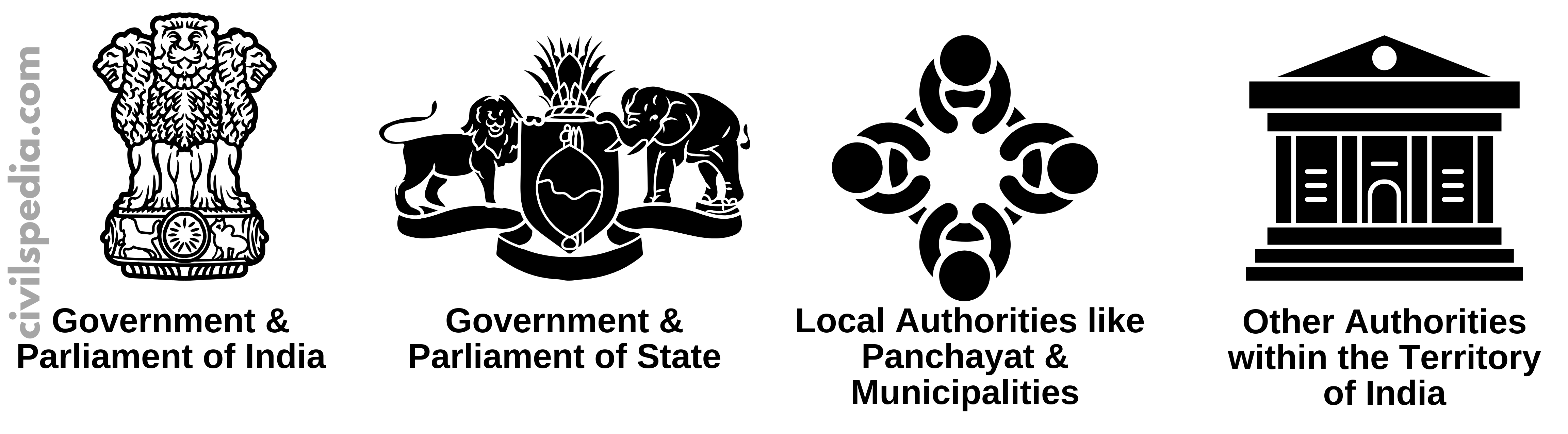

Article 12 defines ‘State’ for the purpose of Part III of constitution- Actions of which can be challenged in courts as a violation of Fundamental Rights.

‘State’ includes

Government & Parliament of India

Government & Legislature of States

All Local Authorities like Panchayat and Municipalities

Other Authorities within the Territory of India or under control of the territory of India

Various Supreme Court judgments have pronounced the following to

be within the ambit of the State as well

Statutory and Non-statutory Authorities like LIC, ONGC, SAIL etc.

Private body working as an instrument of State.

The

most problematic expression in Article 12 is Other Authorities because it is not defined in

the constitution or any other statute of India. Consequently, it falls upon the

judiciary to construe this term, and it becomes evident that the broader the

interpretation of this term, the wider the scope of Fundamental Rights will be.

Judicial History

If we look at the judicial history, the Courts have widened the ambit of the STATE with subsequent Judgements.

Important Cases

The University of Madras vs Shanta Bai (1954): The Supreme Court of India pronounced the Principle of ‘Ejsudem Generis,’ i.e. only those authorities which perform governmental or sovereign functions can be included in Article 12.

In Rajasthan Electricity Board v. Mohan Lal: In the case of Rajasthan Electricity Board v. Mohan Lal, the Supreme Court ruled that the term ‘other authorities’ encompasses any entities established by either the constitution or statutes. This statutory body is not required to be involved in carrying out governmental or sovereign functions.

(Landmark Judgement) RD Shetty vs International Airport Authority (1979): The Supreme Court laid down the following tests for authority to be recognized as a STATE

The State owns the entire share capital.

Enjoys monopoly status

Department of Government is transferred to the Corporation.

Functional character is governmental in nature.

The body is under deep and pervasive state control.

Other Concern in the era of Privatisation and Liberalisation

In the era of LPG, the State is outsourcing its functions to the private authorities.

Hence, where a private entity performs any Public Utility Function, it should come within the purview of Article 12. National Commission to Review the Working of Constitution,2002 has recommended the same.

This article deals with ‘Legislative Relations between Centre and States – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus. For more articles , you can click here

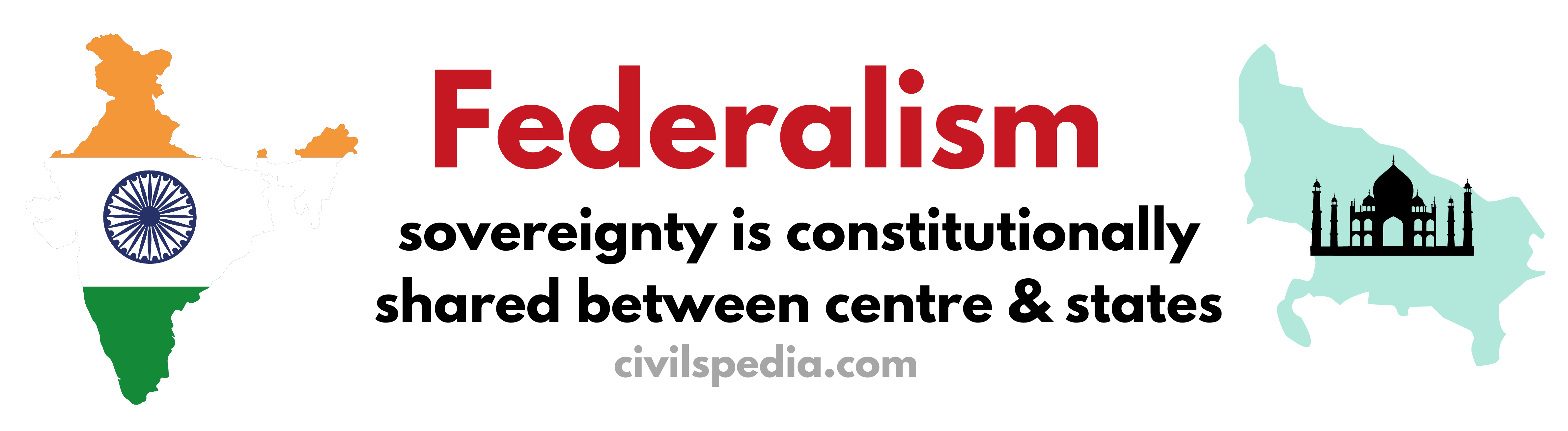

Distribution of Legislative Subjects

India has a federal polity. Federal

Polity is a system of governance in which sovereignty is constitutionally shared between the centre &

states.

As per the Indian

Constitution, legislative or law-making powers are not vested in a single

tier of government; rather, they have been distributed between the Centre

and the States with respect to territory and subject matter.

Territorial Jurisdiction

The Constitution defines the territorial limits of legislative powers. Parliament possesses the authority to enact laws that apply to the entire country or specific regions within its territory. It has extra-territorial legislative powers as well, allowing its laws to apply beyond the borders of India, affecting Indian citizens and their assets worldwide.

A State can legislate only for their State, and its laws are not applicable outside the State.

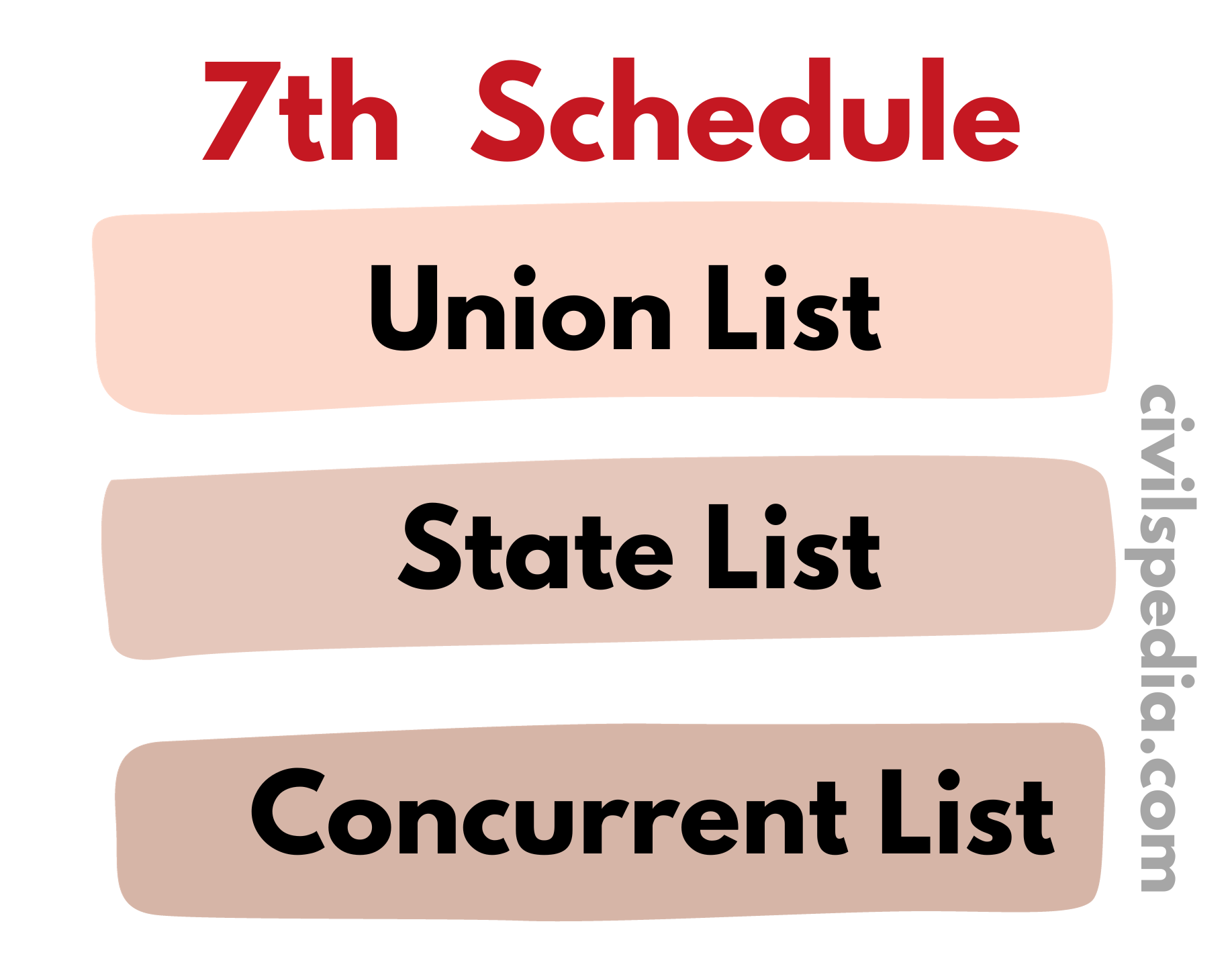

Subject Matter

The

Seventh Schedule of the Indian Constitution outlines this threefold

distribution, specifying legislative subjects allocated to the Centre and the

States.

List I (Union List)

Parliament has exclusive legislative authority over 100 subjects (originally 97) listed in this category.

These subjects pertain to matters of national importance that require uniformity nationwide.

Examples include Defence, Atomic Energy, Railways, etc.

List II (State List)

State Legislatures possess the exclusive right to legislate on 61 subjects (originally 66).

These subjects are of regional and local importance.

Examples include Police, Public Health, Agriculture etc.

List III (Concurrent List)

The authority to enact laws on 52 subjects (Originally 47) is vested in both the Parliament and State Legislatures

Uniformity in such subjects is desirable but not essential. Hence, Union law provides a broad framework, and state laws can introduce variations.

Examples include Education, Marriage, Bankruptcy, and Insolvency.

In the conflict between central and State laws, the Rule of Federal Supremacy applies, i.e. central law prevails. But the exception is that if state law was reserved for the President’s approval & has received it, then it prevails.

Sarkaria recommendation – Acts on subjects in this list should be made after active consultation with the State government except in cases of extreme urgency.

Residuary Subjects

In the USA, Subjects on which the Federal Government can legislate are enumerated in the Constitution & on the rest of the subjects, only states can legislate.

Indian system is taken from Canadian system

The Government of India Act,1935, has the same system with one change on Residuary Subjects, the Governor

Points worth noting

In the USA, Subjects on which the Federal Government can legislate are enumerated in the Constitution & on the rest of the subjects, only states can legislate.

Indian system is taken from the Canadian system.

The Government of India Act of 1935 has the same system with one change on Residuary Subjects: the Governor General can legislate.

When can Parliament Legislate on State Subjects?

Under special

conditions, the Parliament can legislate on subjects included in the State List

under some specific circumstances, which are as follows:

When Rajya Sabha passes a resolution that is in the national interest, Parliament should legislate on State Subjects.

Parliament can legislate on state subjects if the Rajya Sabha passes a resolution, supported by at least two-thirds of the members present and voting, stating that it is in the national interest to do so.

At the same time, the State can also legislate upon the same subject, but in case of any inconsistency, the laws of the Centre prevail.

This resolution remains in effect for one year at a time, and any laws enacted by Parliament under this provision have a maximum life of six months after the resolution has expired.

During National Emergency

Parliament is vested with the authority to legislate on state subjects during a National Emergency.

However, it’s essential to note that laws enacted during a National Emergency become inoperative within six months after the emergency ceases to be operational.

When the State makes a request

Parliament can legislate on a state subject if two or more states make a request for the same. The law enacted will be operational in those specific states. Other states may later choose to come under the purview of such legislation.

Notable examples include the Wildlife (Protection) Act of 1972 and the Water (Prevention & Control of Pollution) Act, which were initiated based on requests from multiple states.

To implement International Agreements and Treaties

Parliament is empowered to legislate on any matter to implement international treaties or agreements.

For instance, the United Nations (Privilege and Immunities) Act and the Anti-Hijacking Act of 1960 were enacted by Parliament to fulfil international obligations.

During President’s Rule

Laws made during the period of

the President’s Rule in a state remain operational even after the

President’s Rule ceases to be in effect.

This provision ensures

continuity and stability in governance during transitions.

Centre’s Control over State Legislature

The

Constitution allows this in the following ways.

The governor can reserve certain types of Bills passed by the State Legislature for Presidential Approval. The President has an absolute veto in that situation.

Certain types of bills can be introduced in State legislature only after the previous sanction of the President, although they are in List II of the 7th Schedule (restrictions on Trade & commerce)

Money and Finance Bills require the President’s approval during a Financial Emergency.

The concurrent list’s items are subject to the Doctrine of Federal Supremacy.

This article deals with ‘Competitive Federalism – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Introduction

Competitive

Federalism refers to the concept in which states compete among themselves and

also with the Centre for benefits. This idea gained

significance in India after the 1990s economic reforms in a free-market economy

when states were trying to woo private investment in their territory.

Different states try to make their own policies in a

competing spirit to

Attract more investment,

Provide more jobs to its

residents.

Increase the standard of life

of people living in its territory.

Competitive

Federalism follows the bottom-up approach as

it brings change from the states.

Competitive Federalism in India

In India, the government replaced the Planning Commission by establishing NITI Aayog, with one of the mandates to develop Competitive Federalism in India.

Indian states are making legal reforms for ease of doing business in their state and attract private companies. E.g., Labour Reforms

Gujarat: Making it more difficult for utility workers to go on strike

Karnataka: Allows establishments to be open longer and allows women to work at night.

Rajasthan: Allow companies employing up to 300 staffers to lay off workers or close down without getting the government’s prior approval

Different states are organizing their investment summits to woo investors to invest in their states. E.g.,

Gujarat’s – Vibrant Gujarat

Punjab’s – Progressive Punjab

DIPP is releasing the Ease of Doing Business Report of States

The

impact of competition for attracting investments to the states can be

understood at two levels.

On the one hand, states are under pressure to provide good governance and manage their finances prudently.

On the other hand, they are aware of the negative impact of many of these reform measures on their electoral popularity.

This article deals with ‘Cooperative Federalism – Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Introduction

The concept of

federalism is where the governments

at various levels, i.e., central, state, and local levels, work in synergy with

each other for the larger public interest, bypassing the differences

between them.

Some Obstacles to Cooperative Federalism in India

Proclamation of Emergency under Article 356: Post-1977, the arbitrary use of Article 356 to impose President’s Rule in states has been a persistent issue.

Union Dominance in Legislative Matters: The Union’s dominance in legislating over the concurrent list and its interference in the state list are also in special cases, such as while ratifying international agreements.

Governor Appointments without State Consultation: States have no say in the appointment of the Governor.

Centrally Sponsored Schemes: The imposition of centrally sponsored schemes under the ‘One-Size-Fits-All’ approach has been a source of tension. States often find themselves obligated to implement schemes without considering regional variations, leading to inefficiencies.

Fiscal Responsibility and Budgetary Management (FRBM) Act: Forcing states to follow the dictates of the Fiscal Responsibility and Budgetary Management (FRBM) Act before the basic public services of ordinary citizens in States are met.

Deployment of Paramilitary Forces without State Consent: Instances of deploying paramilitary forces in states without their consent, such as the use of central forces in Jammu and Kashmir

Enquiries against Chief Ministers for Personal Reasons: The initiation of inquiries against Chief Ministers for personal or political reasons has been a source of tension.

Non-Devolution of Powers to Local Governments: The reluctance of states to devolve powers to local governments, particularly in matters under Schedule XI & XII, remains a hurdle.

How can we achieve Cooperative Federalism?

Consensus Building: Encouraging dialogue and collaboration among states and the central government. For Example, The Goods and Services Tax (GST) was implemented after extensive deliberations and consensus-building among states.

Reactivation of the Inter-State Council: Strengthening the constitutional body will facilitate cooperative decision-making between the Centre and the States.

Protection of State Interests: Ensuring that on issues such as international treaties, World Trade Organisation obligations, or environmental concerns, the interests of affected states are safeguarded.

Greater devolution of power to states: Ideally, the Union should have only those powers which the state can’t handle and require national unity in the form of matters like defence, communication, foreign policy, etc.

Formation of NITI Aayog after scrapping Planning Commission.NITI Aayog has increased the participation of states in its functioning & decision-making.

States’ Involvement in Governor Appointments: Allowing states to have a say in the appointment and removal of Governors to enhance mutual respect

Reform of Schedule XI & XII: Abolish Schedule XI & XII & instead work towards a new local list outlining activities and sub-activities under Local Bodies within Schedule 7 itself.

Side Note: Reasons for the Rise of Cooperative Federalism post-LPG

End of single-party Rule at Centre & emergence of Coalition Politics: The era post-1990 witnessed a shift from a dominant single-party system to a more diversified and collaborative political landscape with multiple parties forming coalitions to govern

Judicial activism, exemplified by landmark cases such as the S R Bommai case, has been instrumental in preventing the Union government from misusing constitutional provisions. The judiciary, acting as the guardian of the Constitution, has consistently intervened to safeguard federal principles.

Active Media: The active role of media in the post-LPG era has contributed significantly to Cooperative Federalism. Informal and vigilant media have played a crucial role in bringing attention to instances where constitutional provisions are at risk of being manipulated for political gains.

This article deals with ‘Federal System– Indian Polity.’ This is part of our series on ‘Polity’ which is important pillar of GS-2 syllabus . For more articles , you can click here.

Introduction

The idea of federalism as an organizing principle between different levels of a state is quite old. Greek city-states had it. Lichchhavi kingdom of northern India in the 6th century BCE is a celebrated example of a republican system. European Union is a recent example of the idea of federalism being implemented at a trans-national level.

The term “federation” is derived from the Latin word “foedus,” meaning treaty or agreement.

A federation can be formed in two ways.

Integration, i.e. Coming Together Federation: When two or more weak states come together to form a strong union, e.g., USA.

Disintegration, i.e. Holding Together Federation: When a Big unitary state is converted to a federation by granting autonomy to provinces, e.g., Canada and India.

Federal Polity is a system of governance in which sovereignty is constitutionally shared between the centre & states.

Federal system is adopted so that

The federal system is

adopted so that

States & their diversity can flourish with autonomy.

For multicultural societies, federalism is an attractive option. It enables minorities to become majorities in sub-national units

Political Motives

The Federal System provides security from external & internal threats.

Additional central assistance, when required, can be provided by the centre in the Federal System.

Economic Motives

The Federal System provides access to the larger national market

Transfer of resources from other states in case of an underdeveloped state.

India has a Federal system, but the term federation is mentioned nowhere in the constitution; instead, Article 1 describes India as a Union of states

Federalism and Stability of State

Centralized administration often refuses to decentralize, thinking it will undermine its integrity. But the opposite is true. Decentralization leads to stability, and those who refuse to decentralize often crumble under their weight.

Difference between Federal and Unitary Government

Federal System

Unitary System

Federal Polity has

a ‘dual government.’

Unitary Polity has

a ‘single government.’

It has a written constitution (must)

It may have written

(France) or unwritten (Britain) constitution.

There is a division

of powers between the centre and the states

There is no

division of power, as all the powers are vested in the centre

There is a

supremacy of the constitution

Constitution may be

supreme (Japan) or may not be (Britain)

Federal Polity has

a rigid constitution

Unitary Polity may

have a rigid or flexible constitution.

Federal Polity has

an independent judiciary

Unitary Polity may

or may not have an independent judiciary.

Federal Polity has

bicameral legislature

Unitary Polity may

have two houses (Britain) or one house (China)

Federal System in India

India is holding together federation different from the USA, which is coming together.

The holding together model was adopted for the sake of the unity of the country & national integration – The constituent assembly prescribed the federalist model so that the country could face the challenges of Centrifugal forces effectively.

Features of the Indian System of Federation

Dual Polity: India follows the concept of

a dual polity, with the Union at the Centre and the States at the

Periphery.

Division of

Powers: There is

a well-defined division of powers between the Union and the States,

elucidated in the 7th Schedule of the Constitution.

Supremacy of

the Constitution: The Indian Constitution establishes the supremacy of

the Constitution itself. All laws must conform to its provisions, and any law

inconsistent with the constitution is declared void.

Rigid

Constitution: The constitution

is rigid in its structure, and the method of amendment is also rigid. Provisions

concerned with federal character can be amended by joint action of state

and centre.

Independent

Judiciary: The judiciary in

India is independent and not under the influence of the Union

government.

Bicameralism: The Indian Parliament follows

a bicameral system, where the Rajya Sabha represents the states of the

Indian Federation, and the Lok Sabha represents the Indian people as a

whole.

Asymmetric

Federalism: India

has Asymmetric Federalism in the sense that the rights and

responsibilities of all the states are not the same. The special nature

and needs of certain regions are defined constitutionally via various

sub-clauses of Article 371

Architect of the Indian Constitution, Baba Saheb Ambedkar, believed that for a culturally, ethnically and linguistically diverse and heterogeneous country like India, federalism was the ‘chief mark’, although with a strong unitary bias. This understanding, which was shared by Pt. Jawaharlal Nehru, Sardar Patel and other national leaders, stood at sharp variance with Gandhi’s idea of federalism, who was a votary of decentralization and devolution of power to the lowest unit of Panchayat.

All federal systems, including the American system, are placed in a tight mould of federalism. No matter the circumstances, it cannot

change its form and shape. It can never be unitary. On the other hand,

the Indian Constitution can be both unitary

and federal according to the requirements of time and circumstances. In

normal times, it is framed to work as a federal system. But in times of

distress(e.g. National Emergency), it is designed to make it work as a unitary

system.

Unitary features of the Indian Constitution

Strong Centre: The Indian Constitution leans towards a strong Centre, where the powers are tilted in favour of the Union.

Parliament’s Authority to Change State Boundaries: Parliament holds the unique power to alter state boundaries and names and even create new states.

Single Constitution for Union and States: Unlike other federations, India has a single constitution that governs the Union and the states. It ensures a unified legal framework throughout the country.

Flexible Process of Constitutional Amendment: The process of Constitutional Amendment is less rigid than found in other federations.

Inequality in State Representation in Rajya Sabha: The Rajya Sabha, the upper house of Parliament, does not guarantee equal representation for states.

Unitary Transition During Emergencies: In times of Emergency, the federal structure temporarily transforms into a unitary one. This shift occurs without the need for a formal Constitutional Amendment.

Single Citizenship: There is only single citizenship, i.e. citizenship of India, and no separate citizenship of states.

Unified Judiciary: There is a single judiciary with the Supreme Court at the top that enforces central and state laws.

All India Services: The creation of All India Services, such as the IAS, IPS, and IFS, is a unitary feature.

Integrated Audit Machinery. CAG audits accounts of both Central and State Governments but is appointed by the President only, and states have no say in his appointment or removal.

Office of Governor: The head of state, i.e., the Governor, is nominated by the President and is an agent of the centre in states.

Integrated Election Machinery: India maintains a single integrated election machinery for conducting both central and state elections.

President’s Absolute Veto: The President has an Absolute Veto over the State Bill if the Governor send any bill to the President for consideration.

Is India a federal state or a Unitary state?

India’s

constitutional framework raises the intriguing question: Is India a federal or

unitary state? The answer lies in the nuanced understanding of the features

embedded in the Indian Constitution.

Although there are large unfederal features that are essentially incorporated for the unity and integrity of the country, it is equally important to recognize that all the fundamental federal features are present in the Constitution. The presence of strong unitary elements has led some scholars to categorize India as a “Quasi-federal” state.

Although Article 1 states that India is a Union of states, this doesn’t mean India isn’t a federation. No particular significance is to be attached to the word union because the word union is used in the Preamble of the USA, too, and citing this, BR Ambedkar said the description of India as a Union, although it is a Federation, does no violence to its usage.

At the time of Independence, traumatized by the partition and violence, the Constituent Assembly wanted to ensure the unity and integrity of the new nation. Hence, the framework departed significantly from all existing models of federalism.

When India adopted this system, In the absence of any track record of India in federalism and the tendency to compare all federal states with the US model, jurists found it difficult to certify that the system was indeed federal. It was therefore declared ‘Quasi-Federal’. This description is no longer valid today because the federal principle has taken root and further developed on Indian soil.

After

the 73rd & 74th Amendments & formation of the Panchayati Raj, a new era

was started in the chapter of Indian Federalism.