e-Commerce

This article deals with ‘e-Commerce – UPSC.’ This is part of our series on ‘Economics’ which is an important pillar of the GS-3 syllabus. For more articles, you can click here.

Introduction

Selling and buying goods using ICT is known as e-Commerce.

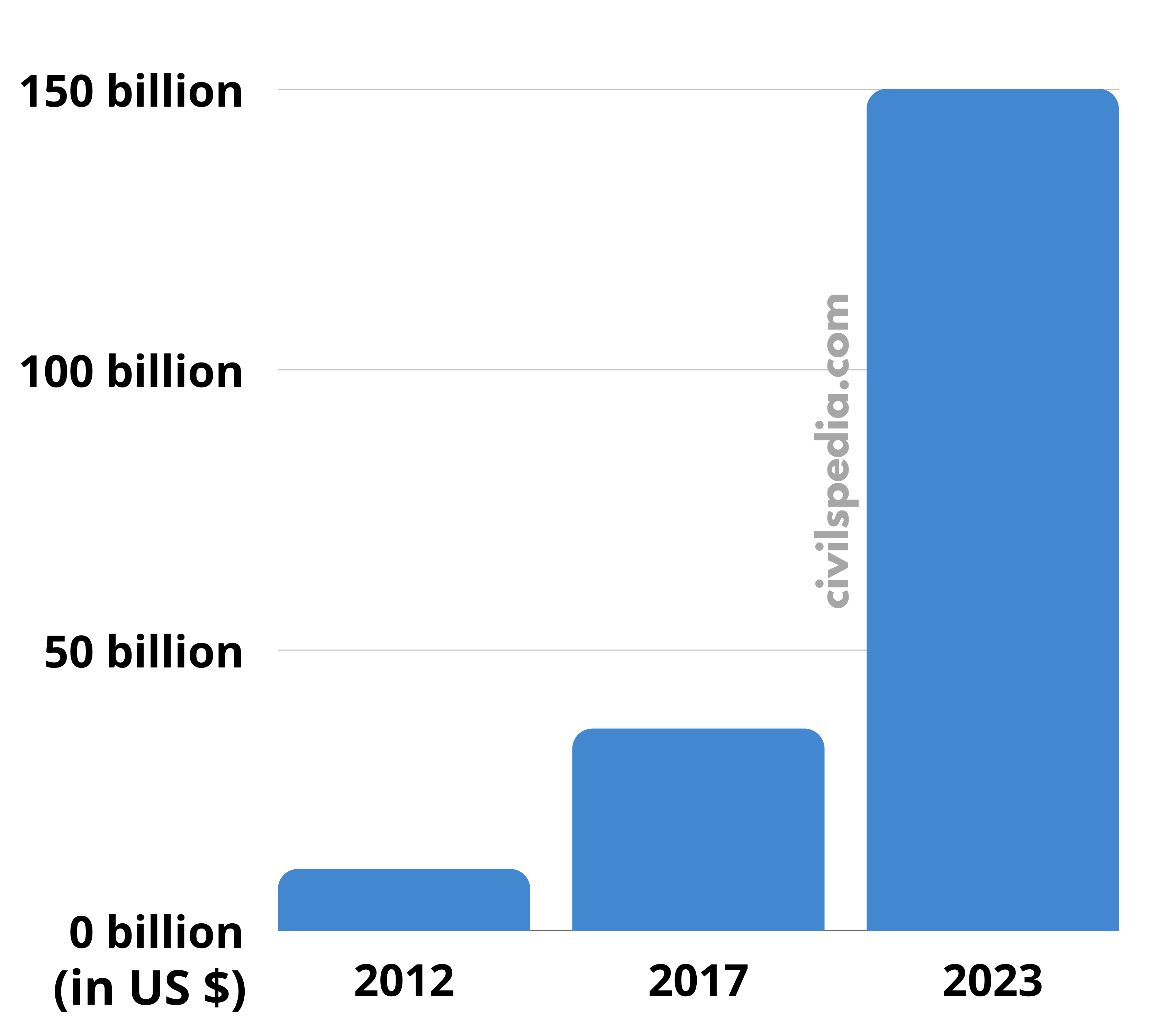

E-Commerce Sector is growing at an incredible pace

The e-Commerce sector has generated a multiplier effect

- Huge creation of jobs

- Reduction of market prices for consumers

- Huge investment in logistics and infrastructure

- Help Artisans exploit new markets. E.g. Karigar ke Dwar (Flipkart)

- Help in promoting tribal art. E.g., Amazon and Trifed signed a contract to sell Indian Tribal Products globally under the brand ‘TRIBES INDIA

Two Models of e-Commerce

There are two models of e-Commerce

1. Market-Based Model

- Market-based Model is followed by Amazon & Flipkart, in which the company provides the IT platform to facilitate the transaction between buyer and seller and takes their fees for providing the platform.

- FDI Norms: FDI is allowed

2. Inventory-Based Model

- In this Model, the seller manufactures and sells its product online—for example, the online store of Samsung, where Samsung sells its phones and other accessories.

- FDI Norms: FDI is not allowed

Other way to define

| B2B | Business to Business |

| B2C | Business to Customer |

e-Commerce Policy

Need for e-Commerce Policy

- Taking Market Based License but then acting as an Inventory based company. E.g., WS Retail, the biggest seller on Flipkart, is owned by Flipkart, and Cloudtail and Appario, which are the biggest sellers on Amazon, are owned by Amazon. Apart from that, Amazon sells its in-house products like Kindle in its marketplace.

- A large amount of customer data is under the control of e-commerce companies which can be misused.

- Importance of sector due to its revenue and job-creating potential. Hence, it should be properly regulated as any mishap can result in a catastrophe.

- Monopolistic market: e-Commerce giants such as Amazon are trying to set up a Monopolistic market by making the brick and mortar stores go out of the market through their policies such as making exclusive deals with mobile companies to sell their phones on their platform only and by giving large discounts.

- Silo-based regulation: e-Commerce in India is regulated by the IT Act, Consumer Protection Act etc. The government needs to consolidate it via a comprehensive act.

Draft e-Commerce Policy

- FDI: Clearly demarcate a marketplace model & an inventory-based model and encourage FDI in the ‘marketplace’ model alone. (Earlier issue: Companies like Amazon show that they follow Marketplace Model but sell their inhouse products (like Amazon Kindle etc.)

- Data: Policy acknowledges data as a ‘national asset’/’societal common’ and seeks to establish a legal & technological framework to restrict the cross-border flow of data generated in India (Earlier issue – Companies take Indian data outside and mine it to target advertisements or sell data about their preferences).

- Taxation Issues: The concept of ‘significant economic presence‘ should be adopted for the purpose of taxation. (Earlier issue – Companies like Amazon don’t pay tax, arguing that they are based in Luxemburg).

- Infrastructure Development: ‘Infrastructure status’ will be given to digital infrastructure like data centres, server farms for data storage etc.

- Small enterprises and start-ups attempting to enter the digital sector can be given ‘infant-industry’ status.

Q-Commerce

- Supply chain disruptions triggered by the pandemic led to a new sub-vertical of the online grocery segment is — Quick Commerce, or q-commerce — where the promise of deliveries within 10-30 minutes of ordering is the unique selling proposition. The focus of most of these ventures is on setting up micro-warehouses located closer to the point of delivery and restricting the stocks at these ‘dark stores’ to a focussed set of under 2,000 high-demand items, as against the traditional formula of well-stocked large-format warehouses located on the outskirts of towns and cities.

- Examples: Instamart, Zepto, Grofers etc.